OUTLOOK

Investors have faced a torrent of central bank actions and communications during the last month, and markets continue to differentiate among economies and companies — a welcome maturation from the markets’ prior regime of “risk on/risk off.” We believe the Federal Reserve has moved from an easing bias to one of tightening — but at an elongated pace that will remain data dependent. Joining in this parsimony are some key emerging-market central banks, including the People’s Bank of China, which is working to control credit risk in the Chinese economy. A more expansive approach is emanating from Europe and its equivocal partner, the United Kingdom. Both the European Central Bank (ECB) and the Bank of England (BoE) have communicated a willingness

for monetary policy to support economic growth. Aggressive action by the Bank of Japan is stimulating the Japanese economy, along with expectations of further benefits from Prime Minister Abe’s new growth policies. Japan’s Upper House elections later this month look set to strengthen Abe’s hand in furthering his economic reform agenda.

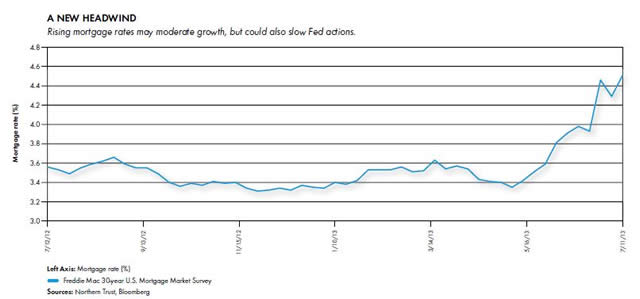

Current growth in the United States is unimpressive, as the effects of fiscal drag, weak export markets and lower inventories mean second-quarter growth could be below 2%. We continue to expect slow, but durable, growth in the United States, supported by the continuing recovery in housing. As the accompanying chart indicates, however, mortgage rates have risen quickly in the wake of the changing monetary policy outlook, and this may slow the pace of housing growth. Emerging-market growth also slowed as the quarter progressed, and is now facing the additional headwind of somewhat tighter monetary policy. European growth is slowly rebounding and looks set to be aided by central bank policy.

Financial markets have been digesting the changing policy outlook and seem to be gaining some confidence about the likely path forward. Equity markets have performed reasonably well over the last month, continuing the pattern

of U.S. strength and lagging emerging markets. Negative returns have been realized across broad bond market indexes, but yield-oriented plays like global real estate have bounced back this past month. We expect this volatility to continue in the bond market, as investors assess incoming data on labor markets and inflation to handicap further monetary policy action.

U.S. EQUITY

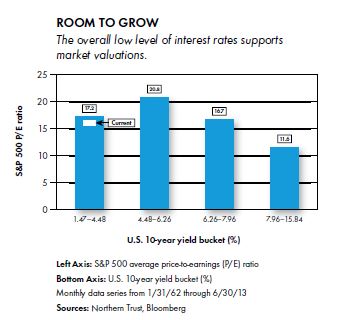

- Rising interest rates have spurred concerns about the impact on valuations.

- Our research suggests that further P/E multiple expansion is justifiable.

As interest rates have begun to rise, reflecting the expectation of a reduction in the pace of Fed purchases of U.S. Treasury and mortgage-backed securities, concerns about the impact of higher rates on price-to-earnings (P/E) multiples have moved to the fore. We believe real interest rates and P/E multiples should be positively correlated — assuming growth and interest rates are moving together — while inflation, instead of improving growth prospects, typically is negative for multiples. Our research suggests that multiples and rates are positively correlated until real interest rates exceed approximately 4%, well above today’s level of under 2%. As a result — and with inflation data remaining relatively benign — we believe further P/E expansion is justifiable at this point in the cycle.

EUROPE & ASIA -PACIFIC EQUITY

- Upcoming elections boost economic prospects for Europe and Japan.

- Accommodative monetary policy should also help growth.

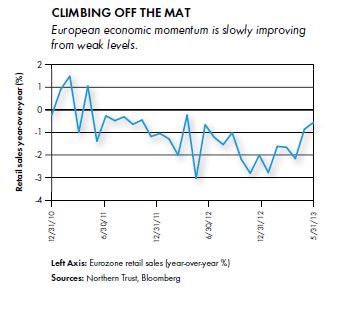

The consensus view is that Europe is stuck in the economic doldrums. Thus, we believe any positive spark could provide a surprise to the markets. This could come from German Chancellor Merkel retaining power after the fall election, allowing for progress on a host of eurozone-specific issues and for further monetary accommodation. Japan’s parliamentary elections in late July likely will further concentrate Prime Minister Abe’s power, enabling him to enact targeted policies to revive Japan’s economy. Accompanying fiscal and monetary measures, Abe plans to improve productivity in the private sector, open up Japan’s markets, and encourage investment by reforming tax systems and free-trade agreements. In contrast to the United States and emerging markets, we anticipate easy monetary policy in Europe and Japan to continue during the next year.

EMERGING-MARKET EQUITY

- Credit and inflation concerns are leading to tighter emerging-market monetary policy.

- Tighter monetary policy hinders an already softer growth outlook.

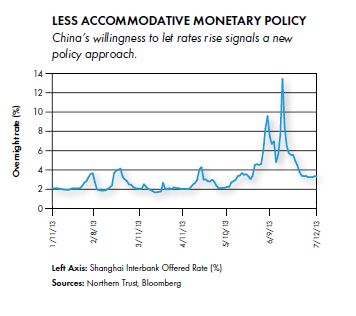

Financial markets have been focused on the rate of slowing in the Chinese economy, but are now also grappling with the unexpected prospect of tighter monetary policy across the emerging markets. While reported economic data doesn’t indicate an economy facing a hard landing, Chinese economic officials surprised the markets with a signal of tighter monetary policy during the last month in their efforts to slow credit growth. This added to investor concerns over the negative impact of higher U.S. interest rates on emerging-market assets. In addition, we’ve seen inflationary concerns lead to higher policy rates in recent weeks in Brazil, Indonesia and India, broadening the concerns over tighter monetary policy.

U.S. FIXED INCOME

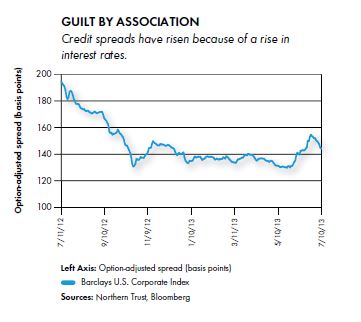

- Corporate credit spreads jumped after talk of Fed tapering took hold.

- With fundamentals remaining strong, we anticipate spreads to narrow going forward.

Fear of higher interest rates caused investors to withdraw funds from fixed income in June, and corporate credit spreads widened as a result. This is partially attributable to the continued sparse liquidity in the fixed-income markets, where broker-dealer risk appetites remain highly constrained. The widening in spreads occurred despite corporate balance sheets remaining in excellent condition. The uncertain political, regulatory and economic environment continues to cause corporations to be reluctant to invest in their businesses. This is occurring despite historically low interest rates that allow companies to forecast a low cost of capital when evaluating new projects. We retain a positive outlook on corporate credit, as continued moderate economic growth in the United States should help strong credit fundamentals.

U.S. HIGH YIELD

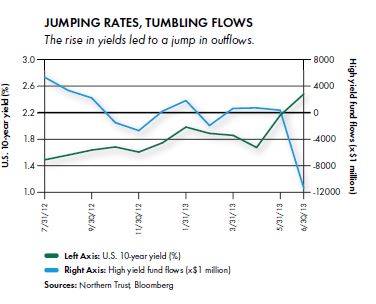

- Interest rate uncertainty has resulted in reallocations between asset classes.

- The revaluation of the high yield market was driven primarily by cash flows out of the market.

Uncertainty about the Fed’s monetary policy outlook has resulted in the reallocation of assets away from fixed-income markets. When the market consensus was for indefinite Fed support, there was little impact of interest rates on fund flows. However, as rates rose in early May because of the Fed’s comments about changing the amount of asset purchases, fund flows became significantly negative. In an illiquid market, these flows were the primary driver of the revaluation of the market, as nothing has changed in the fundamental picture. Credit quality hasn’t deteriorated, and the outlook for the default rate hasn’t increased. With a current yield of around 6.5%, we continue to find U.S. high yield attractive.

REAL ASSETS

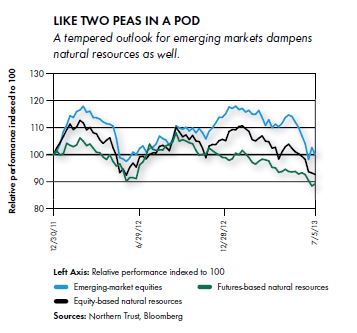

- Emerging-market weakness creates a headwind for industrial metals.

- Other sectors of the natural resources complex are driven by unique factors.

As China’s infrastructure exploded during the last decade, emerging-market and natural-resource equities moved together (exhibiting a correlation of 0.86).

However, recent government pronouncements have indicated concern over the quality of past investments and a reticence to engage in significant stimulus spending, especially as concerns over credit expansion have grown. Industrial metals prices likely will languish in this environment, while agricultural

prices may moderate during the next year after weather-related price spikes. Meanwhile, energy prices are being driven by unrest in the Middle East. We think the lowered emerging-market growth outlook will serve to constrain natural resource price appreciation during the next year.

CONCLUSION

We made changes to several inputs to our investment outlook this month, keying off the outlook for monetary policy. While we moved both the United States and emerging markets from an easing bias to a tightening bias, we have seen further evidence that the major developed markets outside the United States (Europe, the United Kingdom and Japan) remain fully committed to easy monetary policy. So while we downgraded our growth outlook for emerging markets based on slowing momentum and tighter policy, we upgraded our outlook for the European Union (EU) and Japan. We also boosted our assessment of the political leadership for the EU and Japan, with a view that the postelectoral leadership will be able to be more aggressive in tackling their respective regional challenges.

With our downgraded growth and monetary policy outlook in the emerging markets, we favor developed ex-U.S. equities over both emerging market and natural resources. With economic expectations for the EU still muted, we see the potential for modest improvement to be well received by the markets, especially in the wake of easy monetary policy. With these changes, we believe risk assets are more attractive than investment-grade bonds. We anticipate reasonable performance from credit-related fixed income, as credit quality remains high, and continue to favor an overweight to U.S. high yield bonds.

Our risk cases have evolved, as concern about a change in the outlook for low interest rates has come into view during the last two months. First, we see risk in the Fed’s ability to deftly manage the normalization of its balance sheet and management of investor expectations over interest rates during the next year. The road during the last two months hasn’t been smooth, and we face the likely nomination and confirmation of Chairman Bernanke’s successor during the next six months. Our other primary concern centers around political stability in Germany and Japan, where we see the potential for solidified leadership engendering solid policy progress, which underpins our more favorable view toward the European and Japanese markets. Should Chancellor Merkel or Prime Minister Abe not secure the political gains we expect, our expectations for political progress stand to be disappointed.

Jim McDonaldChief Investment Strategist

Basis Points (bps) is a unit of measure in quoting yields, changes in yields or differences between yields; 100 basis points is equal to 1%.

Option-adjusted spread measures the yield spread between similar securities(typically bonds) with different options, such as prepayment or call options, which are very interest rate sensitive.

Price-to-Earnings Ratio is the current share price of a stock divided by its earnings per share.

The Barclays U.S. Corporate Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate, taxable corporate bond market. It includes USD-denominated securities publicly issued by U.S. and non-U.S. industrial, utility,and financial issuers that meet specified maturity, liquidity, and quality requirements.

S&P 500® Index is an unmanaged index consisting of 500 stocks and is a widely recognized common measure of the performance of the overall U.S. stock market.

It is not possible to invest directly in an index.

IRS CIRCULAR 230 NOTICE: To the extent that this message or any attachment concerns tax matters, it is not intended to be used and cannot be used by a taxpayer for the purpose of avoiding penalties that may be imposed by law. For more information about this notice, see http://www.northerntrust.com/circular230.

Past performance is no guarantee of future results. Returns of the indexes also do not typically reflect the deduction of investment management fees, trading costs or other expenses. It is not possible to invest directly in an index. Indexes are the property of their respective owners, all rights reserved.

This newsletter is provided for informational purposes only and does not constitute an offer or solicitation to purchase or sell any security or commodity. Any opinions expressed herein are subject to change at any time without notice. Information has been obtained from sources believed to be reliable, but its accuracy and interpretation are not guaranteed. © 2013.

Asset Management at Northern Trust comprises Northern Trust Investments, Inc., Northern Trust Global Investments Ltd., Northern Trust Global Investments Japan, K.K., The Northern Trust Company of Connecticut and its subsidiaries, including NT Global Advisors, Inc., and investment personnel of The Northern Trust Company.

Please carefully read the prospectus and summary prospectus and consider the investment objectives, risks, charges andexpenses of Northern Funds before investing. Call 800-595-9111 to obtain a prospectus and summary prospectus, which containthis and other information about the funds.

© 2013 Northern Funds | Northern Funds are distributed by Northern Funds Distributors, LLC, not affiliated with Northern Trust.

NT WPR PERS (7/13)

© Northern Trust