I don’t know about your part of the country but I think this summer has been the wettest in some time around Detroit. We have had soooo much rain. Our Great Lakes began the year well below their long-term average depth. After months of rain, all of the Great Lakes are now above their levels from last year, and nearby Lake Ontario has gained ten inches in height in just the last month. Ontario is 11″ higher than one year ago and 5″ ABOVE the century average. Yet its previous below average condition had existed for years and had been worsening – quite a change!

Of course, the way we’ve made up the deficit has been the result of many spring and summer storms. However, while they both bring lots of water, they differ markedly.

In the spring, the gentle rains come with a chill in the air and a constant layer of cloud cover. But in the summer, the storms roll in suddenly, and the hours preceding them are hot and sticky. The humid air rises quickly; hitting the cold upper atmosphere with a clash and storms seems to almost explode from the summer skies.

And when they strike, they are violent. Lightning flashes are common… and close. The skies are constantly rumbling, punctuated with explosions that rattle the house, sending our two dogs scurrying for cover or on to our laps.

Summer stock market conditions are not much different. We’ve seen it happen almost every year. Stocks fall in May and rally in July, only to turn suddenly lower as the summer wears on.

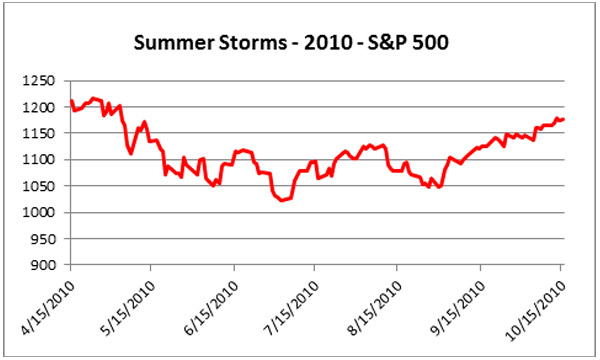

Source: Bespoke Investment Group

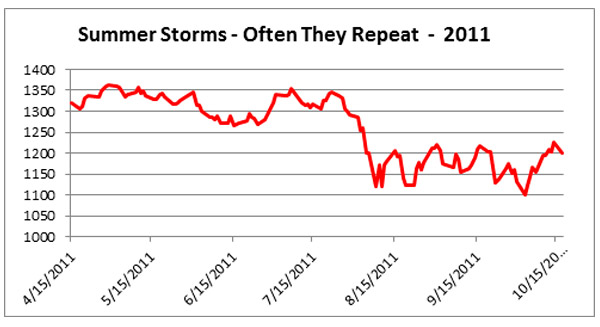

Source: Bespoke Investment Group

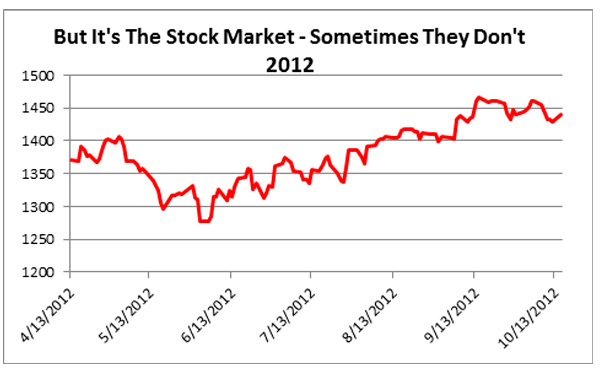

Source: Bespoke Investment Group

This year is not likely to be much different. We have already hit a short-term top in our political/ seasonality index, causing us to move to money market in that strategy last Thursday (7/18). With 4 out of the last 5, and 11 out of the last 12 trading days up in the market, I wouldn’t be surprised to see many of our mean revision-type strategies, like S&P Tactical Patterns, focus more on profiting from down moves than rallies.

Up until now I’ve been solidly in the bulls’ camp. When the market topped in May, I felt that the decline would be a minor one, and it was, with the S&P falling just 5.76% from 5/21 to 6/24. And at that bottom, I was saying in my 6/24/2013 commentary that:

Remember, the biggest mistake made in the markets this year by professional and non-professional investors alike, has been not being fully invested in stocks during the current market rally. So far on the run up it has always paid to be cautious in pushing the sell button. This time may be different, but to determine that precisely we have the various actively managed strategies. As each of them pushes the sell button, we will move, but you cannot anticipate the alarm going off.

I remain a long-term bull on the market, after all, it’s hard for an old trend follower to not be excited about a market that is hitting new highs daily and has moved well above its intermediate-term moving averages. Still, I do get concerned when markets seem to overdo it on the upside.

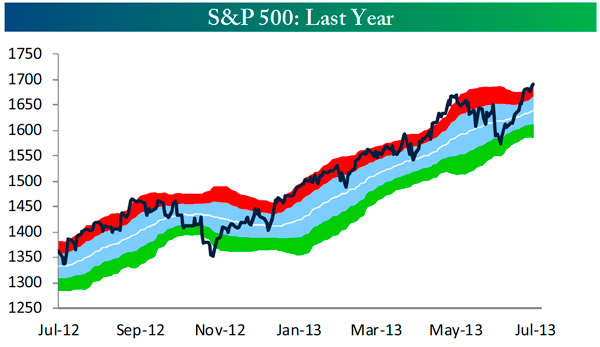

Here’s a chart from Bespoke Investment Group’s Friday newsletter;

Source: Bespoke Investment Group

The red channel denotes that the market has gone into overbought territory. That means that stocks may have risen too far, too fast (or in technical language – more than two standard deviations away from their 50-day average).

When the S&P 500 Index moves above the red channel in the chart, the Index often has a setback, and the longer we are above the upper channel, the worse the downturn tends to be. Obviously we are now above the channel.

Still, despite the damage done by summer storms (I must have passed a half dozen downed trees on the way into the office and we had tens of thousands without power after Friday’s cloudburst), I do believe the likely downturn will be brief and minor in the scheme of things.

Bespoke on Friday quoted the Federal Reserve Board regarding a favorite indicator of mine, the yield curve:

The yield curve – specifically, the spread between the interest rates on the ten-year Treasury not and the three-month Treasury bill – is a valuable forecasting tool. It is simple to use and significantly outperforms other financial and macroeconomics indicators in predicting recessions two to six quarters ahead.

– Federal Reserve Bank of New York, June 1996

Bespoke went on to show that not only is the indicator good for predicting recessions, but it also does well at pointing out times when the odds of a price advance or decline is higher. They conclude with a 50-year study suggesting that the present level of a positive, rising yield curve is good news for stock prices over the next six months.

Bespoke’s analysis suggests that the current positioning of the yield curve has yielded returns over the next three and six months that have been positive 60% of the time and of an order of magnitude 19% to 77% better than average. Our own analysis suggests superior numbers – better than 60% odds and returns 65% to 185% over market averages for like periods.

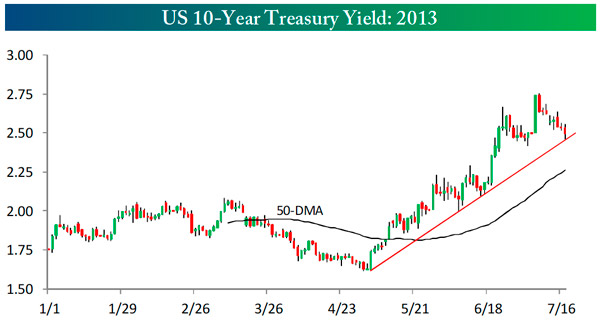

So far in earnings reporting season, while revenues have been mediocre, earnings themselves have been beating expectations at a higher rate than past quarters. And while economic reports are just in the neutral range, interest rates have fallen significantly since they topped out in June. However even here we may be in for a reversal, as the charts show we have hit an upward sloping trend line that has been stopping rate declines lately.

Source: Bespoke Investment Group

There are some storm warnings out and clouds are gathering on the horizon. We always have to be on the lookout for a sudden summer storm. If they turn into something more, well that’s what dynamic risk management is all about.

All the best,

Jerry

© Flexible Plan Investments