A striking feature of this year's global stock market rally is that international markets have significantly trailed U.S. stocks. Nevertheless, Neuberger Berman's Asset Allocation Committee (AAC) recently made the contrarian call of upgrading its view for international developed markets, particularly Europe. In this Strategic Spotlight, we provide an update on the European economy and lay out some reasons for optimism despite the dour growth outlook.

Ongoing Challenges

Following the European Central Bank's (ECB) pledge last year to do "whatever it takes" to keep the eurozone together, the market's heightened concerns about the economic bloc's demise have gradually subsided. Still, high funding costs, austerity measures and downbeat sentiment have taken a toll on growth. Europe remained in contraction mode in the second quarter, with peripheral countries like Greece mired in depression-like conditions. Austerity measures and regulatory reforms stipulated in bailout negotiations have not fully realized their potential to drastically reduce government deficits and expedite a return to growth within troubled countries. The resulting malaise has contributed to near constant political turmoil in affected countries.

Gradual Healing

However, there are signs of improvement. In particular, non-euro economies such as the UK and some Nordic countries have been relatively resilient. The UK, already well into the multiyear implementation of spending cuts, has seen signs of recovery in GDP, consumer sentiment and housing data as the Bank of England maintains easy monetary conditions. In Germany and other larger "core" countries within the eurozone, growth has resumed albeit at only 0.1% in the second quarter. Across the region, manufacturing survey numbers are pointing to improving business sentiment, which generally leads to stronger economic activity in short order.

Hidden beneath the poor headline news and political turmoil, "peripheral" countries are also showing subtle signs of a positive rebalancing in their economies, with declining current account balances and improving productivity levels. While much still needs to be done, reforms in labor markets and other areas have marginally improved competiveness.

Slow Recovery Ahead

Overall, we believe that Europe could return to growth in the fourth quarter of 2013. Stronger countries like Germany are likely to lead the charge, while peripheral countries could lag as private and public sector deleveraging continues. As shown in the U.S. after the 2008–2009 recession, recovery in the banking sector will be important as easing credit conditions could facilitate consumption and investment activity. With inflation remaining low at around 1.5%, we expect the ECB to keep rates low for the near to medium term, which should also benefit asset prices.

Compelling Valuations

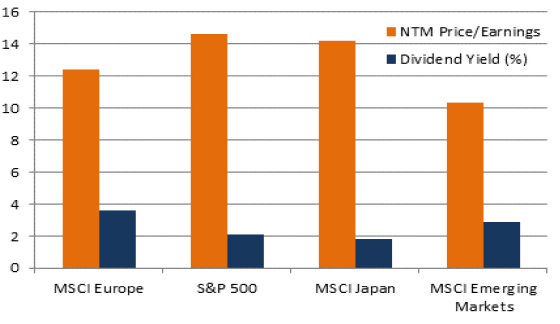

With this backdrop of slow improvement, we believe that underperformance of the region's equities have contributed to a value opportunity. European stocks are trading at a substantial discount relative to safe haven assets such as German bunds, their own historical valuations and U.S. equities. The MSCI Europe Index's forward price/earnings ratio is around 12.4 compared with the current S&P 500 valuation of 14.6. Earnings revisions are on the upswing and dividend yields are attractive at 3.6% when compared to fixed income and other equity markets. (On a P/E basis, emerging markets remain cheaper.) It is also worth noting that Europe's corporate earnings are expected to grow 9% and 12% in 2013 and 2014, respectively—a reversal from contractions in the previous two years.

EUROPEAN VALUATIONS ARE APPEALING

FactSet, as of June 30, 2013.

Time to Retest the Waters

Despite Europe's recent troubles, one should remember that the region represents a $16 trillion economy—about the size of that of the U.S. In our view, the worst of the debt crisis is over and investors who have stayed away from the region may want to consider reentry as part of a long-term strategic allocation. Being selective about opportunities is always important, but Europe undeniably remains home to many multinationals that are levered to global growth and have strong track records of returning value to investors.

As the debt crisis abates, investors might be well served to abide by an often-cited quotation: "Don't let a crisis go to waste."

© Neuberger Berman