There can be little doubt that US equity markets have become more dependent than ever, at least in the short-term, on the every utterance of Fed Chairman Ben Bernanke and his fellow FOMC members.

Chairman Bernanke’s press conference remarks on June 19th led to the worst four-day market declines of the year. After Bernanke laid out a conditional timeframe for tapering the Fed’s bond purchases, the S&P quickly entered a 6.2% correction and the SPY traded by far its heaviest volume of the year on a mass scramble for the exits.

Markets started a steady recovery shortly thereafter, as jawboning by many Fed members (the greatest number of Fed speakers over a week in recent memory) “walked back” the Chairman’s comments.

Flash forward to last week, and Mr. Bernanke was at it again during a Q&A session after a speech in Boston, saying, “Highly accommodative monetary policy for the foreseeable future is what’s needed for the US economy.” Though this was after the market close, S&P futures soared when the remarks hit the wires, adding about 1% in short order, and the Dow followed by gaining 169 points on Thursday.

The Wall Street Journal’s Moneybeat has called this “A new record for Fed flip-flopping.” They added, “While it’s a common exercise for analysts to parse Fed’s messages, the subtleties have reached an extreme lately as interest rates began to move wildly amid expectations for the Fed to taper its bond-buying program.”

Barron’s on Saturday compared the Chairman to a well-intentioned but discipline-challenged parent of a young child, saying, “Ben Bernanke proves that the toughest thing to say can be: No.” (Recall that “Taper Tantrum” was the term du jour in describing June’s market volatility.)

And Bloomberg’s Surveillance radio show was astounded at how fast Chairman Bernanke could go from “bungler” to “genius” in the market’s estimation.

About the only thing clear is that Mr. Bernanke was not saying anything entirely new last week. But he was taking great pains to differentiate between the timing of a “tapering” of the Fed’s $85 billion per month bond purchases and the ultimate raising of interest rates, with the latter by all accounts estimated as not before 2015. In fact Mr. Bernanke reemphasized that, “There will not be an automatic increase in interest rates when unemployment hits 6.5 percent.”

On Friday, Philadelphia Fed President Charles Plosser expressed his frustration at the Fed’s lack of transparency and confusing messages, saying, “The FOMC has offered a variety of changing targets or signals about future behavior. Although the aim was to clarify our policy intentions, I believe the repeated changes have likely caused more confusion than illumination.”

And so market participants will continue to play the “Bernanke Guessing Game,” at least for another year or so it appears.

Which brings us to another point:

An investor should not be about guessing, predictions, or trying to divine the next economic data point or comment coming from the Fed. Rather, it should be about a disciplined, well-diversified approach to portfolio management, with a heavy dose of risk management thrown in. While this approach may not always record the greatest gains in surging markets, it can produce higher risk-adjusted returns over time and much better performance in times of market stress.

The “guessing game” engaged in by many can certainly be a difficult one, even for seasoned professionals. The most recent survey of the National Association of Active Investment Managers’ (NAAIM) member base showed this past Saturday that most were maintaining a “low neutral” cautious outlook on equities, with “bullishness” well below the average for the 2nd quarter of 2013.

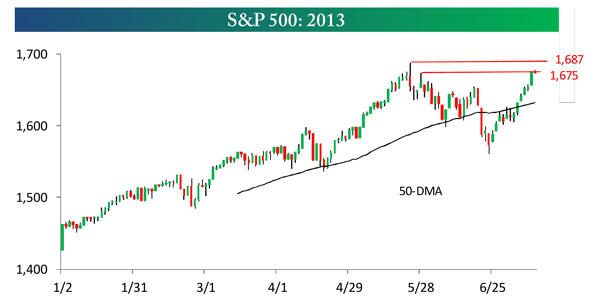

And this despite a week which saw major equity indices registering hefty gains, with the SPX up about 3% and just below all-time intraday highs, as the chart below indicates. Since those June lows, the S&P has put in advances on eleven of thirteen trading days and now sits at a fresh all-time closing high.

Source: Bespoke Investment Group

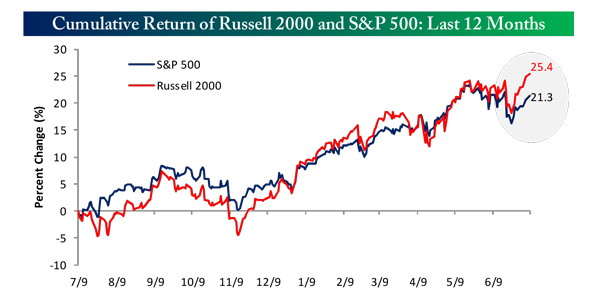

Bespoke Research points out that the current leg up in the markets has been led by the Russell 2000, which had a week full of consecutive all-time closing highs and maintains its out-performance versus the S&P for the past twelve months.

Source: Bespoke Investment Group

What made the market’s performance all the more impressive last week was the move higher in the face of less than stellar economic news. Those cautious managers we referred to earlier had every reason for their skepticism, as only one economic report out of nine beat expectations, with a drop in Consumer Sentiment and higher jobless claims two of the more notable negative data points. Most analysts expect weakness in 2nd quarter GDP, below a 2% annualized rate. The IMF also made headlines last week, lowering both its global and US growth outlook for 2013 and 2014, pegging the US at a “modest” 1.7% rate this year.

Adding to this, the outlook for China growth appears to continue to be moderate and, here at home, the lift in some mortgage rates has revealed the first cracks in the rebound of the housing market. And despite some impressive earnings this past week from JPMorgan (JPM) and Wells Fargo (WFC), economic bellwether UPS threw out some serious warning signals blaming “a weak economy” for a lower outlook.

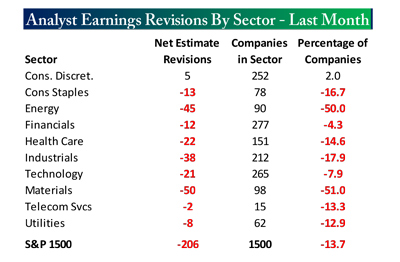

As earnings season is about to kick into high gear, Bespoke also presented a sector review of earnings estimates revisions, finding that analysts have downgraded outlooks for 583 companies in the S&P 1500, while raising estimates for 377. Among the sectors, only Consumer Discretionary maintains a positive net revision ratio.

Source: Bespoke Investment Group

Bespoke concluded its analysis, “Looking at the bright side, at least expectations are low.”

While there are plenty of reasons for caution in the markets, despite the new record highs, Moody’s Analytics was out with a more upbeat analysis titled, “U.S. Macro Outlook: Hanging Tough.” The analysis cited better-than-expected consumer strength in the areas of housing, auto sales and retailing, and a diminishment of European economic threats to US growth prospects.

This report concluded, “The U.S. economy appears to be moving forward gracefully despite raging fiscal headwinds. The tax increases and government spending cuts, which will lower GDP by an estimated 1.5 percentage points this year, have done less damage than expected. Threats to a stronger U.S. recovery, while substantial, are less severe than they were a year ago. Employment in particular has outperformed expectations.”

It will be a big upcoming week on several fronts, with the markets pondering China’s latest economic data, released Sunday evening, 44 members of the S&P 500 reporting earnings and sixteen economic reports to be released. And let’s not forget possible market-moving remarks from Chairman Bernanke, as he will spend two days “on the Hill” Wednesday and Thursday in front of House and Senate committees.

But no guessing here. Let’s sit back and see what happens and respond appropriately. Have a good week.

© Flexible Plan Investments