Stocks got a boost last week from Fed Chairman Bernanke who decided (as predicted here) he needed to reset market expectations about the economy and Fed policy.

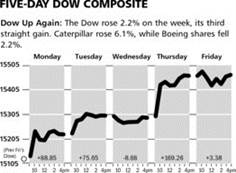

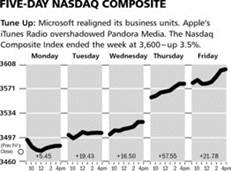

As one can see by the above charts, the Dow Jones Industrial Average rallied over 2% last week while the NASDAQ Composite moved higher by nearly 3.5%.

The Markets & Economy

In case there is any doubt, the power behind the stock market rally is the stated intention of the world’s Central Banks that they will print money until the cows come home. Within the last few weeks the monetary authorities of Europe, Great Britain and Japan have been quite clear that “accommodation is the name of the game”.

Here at home, the USA has been out of sync with its C entral Bank brothers by trying to convince the markets that the economy is sufficiently recovered that a forthcoming change will be made in the so-called quantitative easing policy. Just this hint last month sent bonds plunging and caused a correction in stocks.

The only problem is that it is based upon a premise that is not true. The USA economy is actually turning in a very dismal second quarter of growth. GDP estimates have now fallen to below a one-percent growth rate.

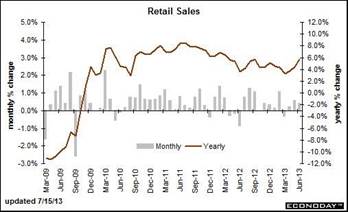

Why hasn’t the improvement in the jobs market over the past year translated into higher economic activity as measured by GDP growth rates? The answer is that it has all basically been a mirage. Just look at this morning’s June report for retail sales. It was awful.

While the overall number showed an increase, if one adjusts for higher gasoline prices and automobile sales, the number was negative. How can this be, given that the government says there are a couple million more people working this year than last?

The numbers do not lie. While one can makeup jobs out of thin air via assumptions about participation rates etc…the numbers on retail sales and GDP actually can be measured with relative accuracy.

Accordingly, the Fed showed up last month with its warning about “tapering” at just the wrong time. The economy was slowing, not growing and the jump in interest rates and oil prices have now lowered expectations for the second half of the year. Hence the need for Bernanke to give the stock and bond markets a goose - and last week he did just that.

In essence, nothing is changing. The economy muddles along with bad fiscal policies emanating from Washington DC, being offset by this crazy loose monetary policy. The result is a stalemate. The economy limps along while the stock market does very well as it is the best asset class for investors out there. In particular US stocks look good given the relative stability of the dollar versus the mess called the Euro.

What to Expect This Week

Earnings will be flooding the scene. Financials seem to be ok, but look for problems elsewhere. Recent warnings by Federal Express and Accenture bode ill for many important names due to report. This may give us a chance to initiate positions on weakness given how stock prices react.

Additionally, the Fed Chairman will once again speak on Wednesday. No doubt he is interested in making sure that investors know that he really means it when he says future policy moves are data dependent. Since he knows the data is weakening, look for bond prices to improve and to serve as further support for stock prices.

The weekly update from the Economic Cycle Research Institute shows little change but a worsening trend, if ever so slight. Given the economic malaise which most people are still not thinking about correctly, bond prices could be due for a nice rally as we head into the fall.

![]()

SYMBOL: BA

Boeing was in the news again last week due to a fire Friday on a grounded 787 Dreamliner at London’s Heathrow airport. The investigation into this fire is being led by Britain’s Air Accident Investigations Branch. Industry sources expect an initial report will be released by the end of this week. While the Company has remained in the news the last couple of weeks, the shares still are one of the best performing stocks in the Dow Jones this year.

While there is no definitive report on the recent fire, investigators have found no evidence that the incident was caused by the airplane’s batteries. The overheating of two batteries on Dreamliners back in January caused a temporary grounding of the 787, but we don’t expect a similar result from this fire. There haven’t been any cancellations for the 787s and airlines need this plane more than ever. The strong backlog continues to fuel the share price higher, and we expect the share price to reach $125 by the end of this year.

![]() and

and ![]()

SYMBOLS: EPD and R

Two of our core holdings announced dividend and distribution increases last week, which is a sign of confidence to all stakeholders.

First of all, Ryder declared its regular quarterly cash dividend of $0.34 per share. The dividend represents a $0.03 increase from the $0.31 dividend the Company had been paying out since last year at this time. This is Ryder’s 148th consecutive quarterly dividend payment.

Also, Enterprise Products increased its quarterly cash distribution to $0.68 per common unit. This distribution reflects a 7.1 percent increase in the distribution from a year ago. This is the 36th consecutive quarter that the Board of Directors has increased its quarterly cash payout.

Both of these companies have been solid performers for our clients over the past several years, and we expect more positive news from management when both companies announce their second-quarter earnings results. We are always encouraged when companies continue to raise their payouts to shareholders and expect to remain long-term shareholders of both of these companies.

© McIntyre, Freedman & Flynn