Beneath the Noise, a Resilient Demand Trend and Clear Fed Plan

- Available data point to real GDP growth of less than 1% in the second quarter, yet we are looking through the dip: core demand data have been firmer (watch June retail sales on Monday), and a Q2 inventory correction will likely be followed by current quarter re-stocking.

- The sharp upward adjustment in mortgage rates will not derail the housing recovery. The upward trend in new construction is tightly tethered to household formation; and while house price growth may slow, home sales should continue their gradual ascent: affordability remains high even at current rate levels, and expected future rates and prices, as well as rising employment and income security, exert positive influence on demand.

- The FOMC has provided substantial clarity, in our view, regarding the monetary policy path that it intends to follow if the economy evolves in line with its expectations. To anticipate a different course of monetary policy over the next 2½ years, one must hold a different economic outlook (we do not). In contrast, we find little appeal in arguing for a different policy course based on the assertion that the FOMC will end up responding to a given set of economic outcomes in a manner at odds with its stated reaction function.

Q2 growth: look beyond the headline

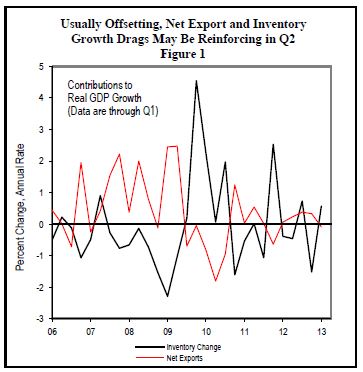

Estimates of Q2 real GDP growth have fallen by roughly one percentage point over the last two weeks, to less than 1% (annual rate), owing roughly equally to downside surprises in May net exports (goods & services balance $4.8 billion wider) and wholesale inventories (-0.5%). Given these sources, anticipated weakness in the release of Q2 growth (due July 31) will not be indicative of underlying trends in the economy. We expect 2.7% growth in Q3.

- Outright inventory liquidation is unsustainable, so a current quarter growth contribution from wholesale inventories (and from aggregate re-stocking, including manufacturers and retailers) likely.

- It is unusual for inventories and net exports to make contributions to growth in the same direction within a given quarter, as appears to have occurred in Q2: since some inventories are imported and others are due for export, a slower pace of inventory building (or outright de-stocking) is generally associated with a narrower trade gap.1 It is possible that the trade gap narrowed sharply in June, shifting net exports to a positive contributor to growth, erasing the apparent anomaly.2 Alternatively, the unusual occurrence could repeat in Q3, but with the sign reversed as inventories and net exports both add to growth.

- Available data indicate core domestic demand (consumption, housing, business fixed investment) holding up better, tracking near 2½%. Indeed, both the inventory draw and import surge could reflect stronger demand than has yet been reported. We look to June retail sales (due Jul. 15) and durable goods data (Jul. 25) for evidence with which to test of this hypothesis.

Source: Bureau of Economic Analysis, Haver Analytics

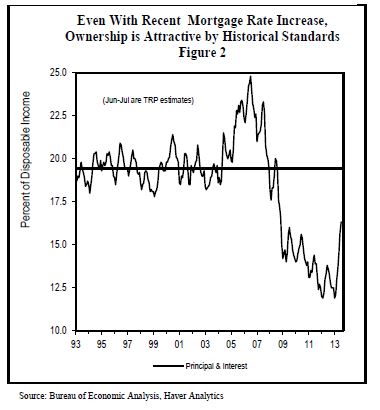

Limited risks to housing from higher rates

The 120 basis point April-May rise in mortgage rates has prompted concern for the viability of the housing recovery. Our highest-confidence view on this subject is that the rise in borrowing rates will not disrupt the recovery in construction of new housing units. From the broadest perspective the current pace of housing starts is too low relative to the rate of household formation. An anticipated June rise in housing starts (Jul. 17) July consolidation of June’s sharp rise in builder sentiment (Jul. 16), would support this view. In addition, it stands to reason that higher mortgage rates will cool the recently heated pace of home price inflation, in part by tarnishing the economics of investor purchases.

Nonetheless, we are skeptical that the current level of rates will undermine the gradual recovery in home sales (although a short-term setback is certainly possible – the Mortgage Bankers Association index of mortgage applications for home purchase has fallen 6.1% over the past two weeks to a four-month low). Even at current interest rates, mortgage carrying costs are low by historical standards: principal and interest on a mortgage financing 80% of the median-priced home has risen from an all-time low 11.9% of median family income in January to an estimated 16.3% in July, but this level is still well below the pre-bubble (1993-2004) average of 19.4% (Figure 2), corresponding to an affordability index of 128.9%.3 Particularly with affordability still attractive by historical standards, the negative impact of the recent increase in rates is likely to be outweighed by the positive influences of expected future rates and prices, as well as by employment and income

security.

The Fed’s message has been clear, deal with it

Here’s the Fed’s plan, (broadly) same as it ever was:

- Begin the wind-down of asset purchases later this year if incoming data are broadly consistent with the FOMC’s forecast. (We expect the first tapering step no later than the Sep. 17-8 meeting.)

- Cease asset purchases around mid-2014 (assuming that the unemployment rate has declined to “the vicinity” of 7% “with solid economic growth supporting further job gains”4).

- Begin discussing rate hikes when the unemployment rate reaches 6.5%5; FOMC projections imply a 6.5% average unemployment rate in the first quarter of 2015.

- Begin to raise policy rates in 2015, and proceed to “remove accommodation” – raise rates – gradually thereafter.6

Now hear this!

In the FOMC policy statements, removal of policy accommodation has always referred to raising policy interest rates, not to any aspect of balance sheet policy. There is no contradiction between winding down asset purchases and concluding “that highly accommodative monetary policy for the foreseeable future.” 7

The FOMC has provided substantial clarity, in our view, regarding the monetary policy path that it intends to follow if the economy evolves in line with the Committee’s expectations. To anticipate a different course of monetary policy over the next 2½ years, one must hold a different economic outlook (we do not). In contrast, we find little appeal in arguing for a different policy course based on the assertion that the FOMC will end up responding to a given set of economic outcomes in a manner at odds with its stated reaction function.

1 This relationship – quarterly contributions to growth from inventories and net exports of opposite signs – held 70% of the time over the past 10 years.

2 June business inventory and international trade data will not be released until after the July 31 initial estimate of Q2 GDP. The Commerce Department will incorporate its own estimates of these and other missing data in that first estimate of Q2 GDP.

- 3 At this level of affordability, median income is 128.9% of the level required to qualifying for 80% financing of a median-priced home.

4 Ben S. Bernanke, “Press Conference,” June 19, 2013. Transcript from Roll Call, Inc., via Bloomberg.

5 Subject to the FOMC’s 1-2 year inflation forecast not exceeding

2.5% and inflation expectations being contained.

7 Eighteen of 19 FOMC participants expect the Fed funds target rate to have been increased at least once – by 25 basis points to 0.5% - by the

end of 2015. Forecasts for the 2015 Q4 average funds rate range from 0-.25% to 3.0%, with a median of 1.0% and mean of 1.34%.

7 Ben S. Bernanke, “Question and Answer Session at a Conference

Sponsored by the National Bureau of Economic Research, Cambridge, MA, July 10, 2013. Transcript from Roll Call, Inc., via Bloomberg.

Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. The material is not intended to be a solicitation for any product or service not available to U.S. investors, including the T. Rowe Price Funds SICAV, and may be distributed only to institutional investors.

Issued in Japan by T. Rowe Price International Ltd, Tokyo Branch (“TRPILTB”) (KLFB Registration No. 445 (Financial Instruments Service Provider), JSIAA Membership No. 011-01162), located at NBF Hibiya Building 20F, 1-7, Uchisaiwai-cho 1-chome, Chiyoda-ku, Tokyo 100-0011. This material is intended for use by professional investors only and may not be disseminated without the prior approval of TRPILTB.

Issued in Canada by T. Rowe Price (Canada), Inc. T. Rowe Price (Canada), Inc. enters into written delegation agreements with affiliates to provide investment management services. T. Rowe Price (Canada), Inc. is not registered to provide investment management business in all Canadian provinces. Our investment management services are only available to select clients in those provinces where we are able to provide such services. This material is intended for use by accredited investors only.

Issued in Australia by T. Rowe Price International Ltd (“TRPIL”) (ABN 84 104 852 191), Level 50, Governor Phillip Tower, 1 Farrer Place, Suite 50B, Sydney, NSW 2000, Australia. TRPIL is exempt from the requirement to hold an Australian Financial Services license (“AFSL”) in respect of the financial services it provides in Australia. TRPIL is authorised and regulated by the UK Financial Services Authority (the “FSA”) under UK laws, which differ from Australian laws. This material is not intended for use by Retail Clients, as defined by the FSA, or as defined in the Corporations Act (Australia), as appropriate.

Issued in New Zealand by T. Rowe Price International Ltd (“TRPIL”). TRPIL is authorised and regulated by the UK Financial Services Authority under UK laws, which differ from New Zealand laws. This material is intended only for use by persons who are not members of the public, by virtue of section 3(2)(a)(ii) of the Securities Act 1978 and is not intended for public distribution nor as a solicitation for investments from members of the public. This material may not be redistributed without prior written consent from TRPIL.

Issued in the Dubai International Financial Centre by T. Rowe Price International Ltd ("TRPIL"), 60 Queen Victoria Street, London EC4N 4TZ, which is authorised and regulated by the UK Financial Services Authority (the "FSA"). This material is communicated on behalf of TRPIL by the TRPIL Representative Office which is regulated by the Dubai Financial Services Authority ("DFSA") as a Representative Office. This material is not intended for use by Retail Clients, as defined by the FSA and DFSA. Retail Clients should not act upon information contained within this material.

Issued in Hong Kong by T. Rowe Price Hong Kong Limited (“TRPHK”), 21/F, Jardine House,1 Connaught Place, Central, Hong Kong, a Hong Kong limited company regulated by the Securities & Futures Commission. This material is intended for use by professional investors only and may not be redistributed without the prior approval of TRPHK.

Issued outside of the USA, Japan, Canada, Australia, New Zealand, DIFC and Hong Kong by T. Rowe Price International Ltd, 60 Queen Victoria Street, London EC4N 4TZ, which is authorised and regulated by the UK Financial Services Authority (the “FSA”). This material is not intended for use by Retail Clients, as defined by the FSA.

This material is provided for informational purposes only and is not intended to be a solicitation for any T. Rowe Price products or services. Recipients are advised that T. Rowe Price shall not offer any products or services without an appropriate license or exemption from such license in the relevant jurisdictions. This material may not be redistributed without prior written consent from T. Rowe Price. The contents of this material have not been reviewed by any regulatory authority in any jurisdiction where this presentation is being made or by any other regulatory authority. This material does not constitute investment advice and should not be exclusively relied upon. Investors will need to consider their own circumstances before making an investment decision.

T. Rowe Price, Invest With Confidence and the Bighorn Sheep logo is a registered trademark of T. Rowe Price Group, Inc. in the United States, European Union, Australia, Canada, Japan, and other countries. This material was produced in the United Kingdom.

The views contained herein are as of June 14, 2013, and may have changed since that time.

Copyright © 2013 by T. Rowe Price Associates, Inc. All rights reserved.