Prepare for the 1-2 Punch of Declining Earnings and Multiple Contraction

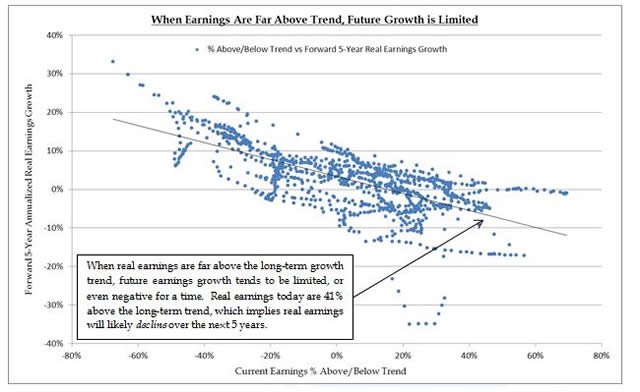

The market today is counting on continued earnings growth driven in large part by ongoing quantitative easing without inflationary consequences. In arecent strategy letter, we show that the market’s expectation for future earnings growth is overly optimistic based on the fact that earnings are currently more than 40% above the long-term trend and mean-reversion and history suggests that real earnings are likely to decline over the next 5 years.

Furthermore, we show how these anticipated low levels of earnings growth over the next 5 years are typically accompanied by much lower valuations.

This 1-2 punch of declining real earnings and declining valuations are likely to lead to real inflation adjusted losses to owners of stocks while benefiting owners of real assets.

- Stock Market Valuations Rise and Fall with Real Earnings Growth (or Lack Thereof)

- When the Long Term Arrives in the Short Term: Treasury Yields

- There are Only a Few Good (Real) Investment Options During a Large Monetary Expansion

© Sitka Pacific Capital Management