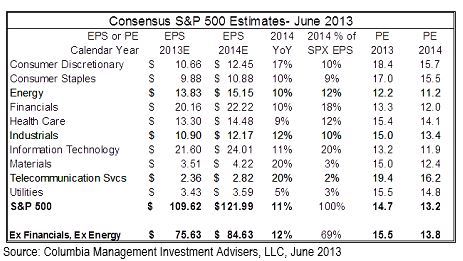

With the ebbing of the quantitative easing taper debate, can we go back to our regularly scheduled programming of earnings driving the stocks? If so, where do we stand? There are certainly some areas where we think estimates are a little high and some where they are too low. But in order to get a better picture of earnings expectations and what is priced in, we need to look at both the earnings and the PE (price-to-earnings) ratio the market has placed on those earnings. The table below illustrates the current state of earnings estimates and some of the key themes investors need to focus on:

Source: Columbia Management Investment Advisers, LLC, June 2013

Technology: Now proportionally represented in the “Shifty Fifty.”

It is interesting to sort the S&P 500 for the 50 biggest detractors to the market PE — the companies that are both large in size and low in PE. The usual suspects on this list are large financial and energy companies. But these days, tech companies constitute eight of these 50, slightly higher than a proportional representation. Because low PE ratios generally signal skepticism about the sustainability of earnings, “Shifty Fifty” seems like an apt term. But why the skepticism? Corporate tech spending has stayed tighter for longer as CFOs and CEOs seem more willing to push back on their IT departments. And with more computing taking place in the cloud and not on our desktop computers, the need to get a faster computer every two years has waned. Global PC and desktop unit sales growth stalled at minus 13.9% in Q1 2013, following a decline of 3.7% in 2012. Tablets took share and caused much of the decline, but basic demand is still a bit soft. Federal IT spending cuts, estimated at 7%, triggered revenue shortfalls in this area in the Q1 2013 reporting season. In terms of the actual earnings, we saw disappointments across the board in Q1, and have continued to see disappointments for the companies reporting quarters that closed in May. While worries over long-term growth persist, risks to the remainder of 2013 seem manageable.

Cyclicals: Some “faith-based” estimates and multiples. Some of our best stock ideas are in cyclicals. But within industrials and some areas of consumer discretionary, we do see a higher incidence of earnings that look a little high, or PE ratios that tell us general growth expectations are too high. For industrials, the year started with management teams giving guidance that relied on a pick-up in activity in the 2nd half of 2013. Their faith was not backed by orders, backlogs or other solid indicators. Some companies have lowered guidance as the orders have not accelerated. But consensus still shows 9.7% operating profit growth in the second half for industrial firms vs. 2.7% in the first half of 2013. The stocks are coming to terms with this in varying degrees, but it may be optimistic to think the remaining adjustment will be painless.

The consumer discretionary sector has high PE ratios. Some of this is likely attributable to investor attraction to simple business models, modest growth and a healthy allocation of capital to dividends and buybacks. Witness the relative performance of media stocks where investors seemed to have favorably re-evaluated the major franchises in this space. But 17% earnings growth from 2013 into 2014? That’s a bit beyond the normal Wall Street analyst optimism that we try to account for. So when one looks at industrials, consumer discretionary or even semiconductors, the combination of estimates and PE ratios indicate both optimism and demand for cyclical recovery stories. I do think things are getting better, but bargains seem hard to come by among the cyclical merchandise.

Other key sectors — General trends and themes continue.

There isn’t much controversy in consumer staples. The recent weakness in the sector is probably more about an “air pocket” in demand for reliable, total yield stocks in the face of rising rates. With the financial sector trading at 1.1x book value and 2013 reflecting an Return On Equity (ROE) of about 9%, the earnings ramp still has room to move up, but the steepness is not what it was two years ago. Rate normalization is a good thing for financials, but could cause some short term issues in areas like mortgage refinancing or general originations. Global pharmaceuticals could see some weakness due to softness in demand. But the healthcare sector, especially managed care, is waiting to see how the next leg of the Affordable Care Act affects enrollment, utilization and pricing.

Summing up — The path to year-end.

Bottoms-up consensus estimates for the S&P 500 stand at just below $110. Based on our internal estimates, I would expect the actual number to come in at about $108, and for estimates to follow the saw-tooth pattern we’ve seen over the last several quarters. That is, estimates come down 2%-3% during the quarter, but then “beat” by somewhat less than the amount the estimates had faded. Share count reduction will probably help earnings growth by about 1.2%-1.5%. Barring macroeconomic troubles and banking on some decrease in year-over-year fiscal drag caused by higher taxes and lower federal spending, $115 is a good placeholder for 2014.

Disclosure

The views expressed are as of 7/8/13, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2013 Columbia Management Investment Advisers, LLC. All rights reserved. 692071