Investors have been conditioned by more than eighty years of experience to expect 5% annualized yields from a traditional bond portfolio. After a sustained downward trend in yields, it has become clear that this assumption may no longer be valid. Yields on 10-year U.S. Treasury notes have dipped below 2%, and inflation-adjusted yields have been negative for several years.1

Healthy yields are evaporating precisely when they are needed the most. With record numbers of retirees leaving the workforce in coming years, the need for reliable streams of investment income has never been greater. Compounding the problem are elevated levels of risk associated with traditional fixed-income strategies, including Treasury bonds typically perceived as a “safe” investment.

Fortunately, today’s global investment landscape offers an expanding range of income-generating options. This paper identifies some less traditional sources of income, highlights key benefits and risks, and discusses how they might best be integrated into existing portfolios. These are difficult times for those investors seeking income from their investment portfolio. While interest rates are slightly above lows reached in 2012, they are still well below historical averages. And since August of 2011,yields on 10-year Treasury notes have been so low they have lagged inflation.2

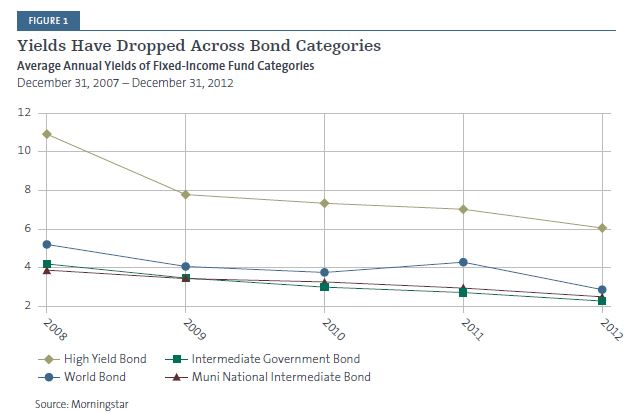

Moreover, yields have been falling across the asset class spectrum. Average annual yields have genera lly declined steadily for all categories of fixed-income mutual funds (Figure 1). For example, average yields for high-yield bond funds tumbled from almost 10.9% at the end of 2008 to 6.1% in 2012.

The question for income investors is, What now? If yields remain low, their financial plans and retirement income could be in jeopardy. While no one can predict when or if the Federal Reserve will raise interest rates, most analysts believe interest rates are likely to stay low for quite some time. Even the Congressional Budget Office is not forecasting a return to the long-term average until 2016, when it expects interest rates to rise steadily alongside a strengthening economy.3

Even if rates on government debt do tick higher, it is entirely possible that they will not keep up with inflation, whether the official kind calculated by a basket of goods, or the more visceral kind felt as sticker shock at the gas pump or supermarket.

If, on the other hand, the Federal Reserve decides to begin raising rates, investors would face a different kind of risk. The long bull market in bonds has produced solid total returns, with appreciation in bond values helping to offset declining yields. But if and when interest rates rise, bond prices are likely to drop, which could translate into serious losses to existing fixed- income portfolios.

The upshot is that traditional bond investments long deemed “safe” may not be so safe anymore. Market risk now looms larger than at any time in recent memory, and higher tax rates only compound the problem.

In light of these challenges, financial advisors are increasingly seeking to diversify their clients’ bond market exposure. They are also casting a wider

net for investment strategies with the potential to generate more income than traditional sources. Investors are increasingly exploring global opportunities, and some are integrating assets (such as commercial real estate) and strategies (such as long/short approaches) they might not even have considered only a short time ago. Three specific approaches to generating more income are explored here in more detail:

• Multisector bond strategies that seek to capitalize on differences in relative value

• Dividend strategies employing a more refined and global approach

• Emerging market (EM) corporate bonds, which has recently emerged as a viable asset class

Multisector Bond Strategies: Seeking to Profit From Relative Value

Rather than turning away from bonds in the face of elevated risk levels, some investors are scrutinizing the risks of various bond market sectors and strategies against their income and return potential in order to benefit from the disparities in the relative value of differing bond strategies.

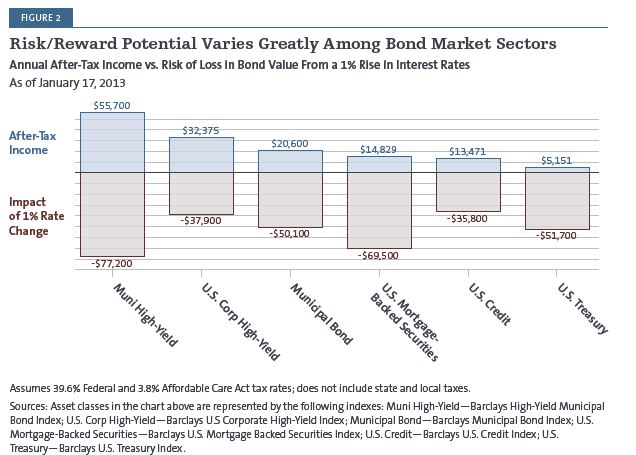

As an example, Figure 2 compares the potential for risk-adjusted after-tax income across different types of bonds, based on historical yields and current tax rates, with the asset value that would be at risk if interest rates were to rise 1%. As of January 2013, Treasurys had the lowest income- to-risk ratio, meaning their ability to produce income per unit of risk was the lowest among all

types of bonds examined. In fact, Treasurys posed dramatically lower ratios than those of high-yield corporate bonds or high-yield municipal bonds. This type of relative value analysis can be used to identify which opportunities may hold the greatest potential for total return.

Another diversification opportunity, in contrast to traditional bond portfolios which almost uniformly take a long-only approach, are nontraditional strategies which may use short selling to offset risks on the long side of the portfolio. Managers may also take advantage of diverging relative values by shorting expensive securities while holding long positions in less expensive asset classes.

Dividend Stocks: A More Refined and Global Approach

The search for yield has also generated a growing wave of interest in dividend-paying stocks, which offer attractive relative yields not only in the U.S. and Europe, but also in emerging markets.4

Research shows that dividend-paying stocks outperform nondividend-paying stocks on a total return basis over a full market cycle.5 A deeper dive into performance patterns brings two important findings to light:

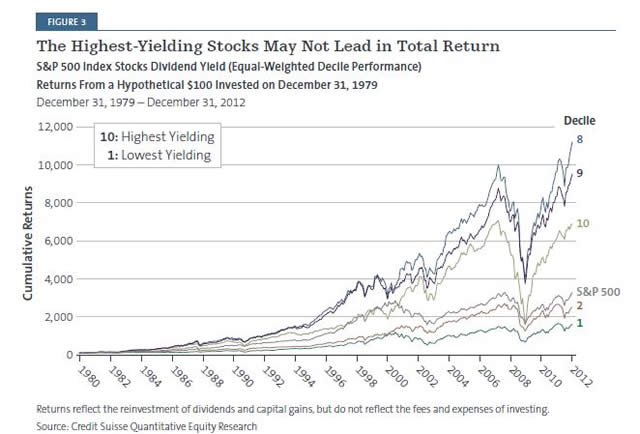

• Stocks with the highest dividend yields do not generate the best total return, counterintuitive as that may seem. When dividend stocks are grouped into percentiles based on yield, it is those in the mid-to-upper decile (not the ninth

or tenth) that produce the best long-term return (Figure 3). Studies show a similar result across all geographic regions, with firms sporting the highest payout ratios rarely producing the best results.6 Clearly, selecting dividend stocks based on yield alone may not be a winning strategy.

• Dividend payout ratio (the proportion of earnings paid in the form of cash dividends) is an important determinant of total return versus yield alone. Research shows that a combination of low payout ratios and high (but not highest) dividend yields generally reflects a market’s sweet spot.7

This second finding makes sense when one considers the highest-yielding stocks are typically those of companies that also have the highest payout ratios. Distributing a high proportion of their income as dividends may leave companies with little or nothing to reinvest in the business. If unable to finance their growth internally, they must rely on the capital markets through new equity or bond issues.

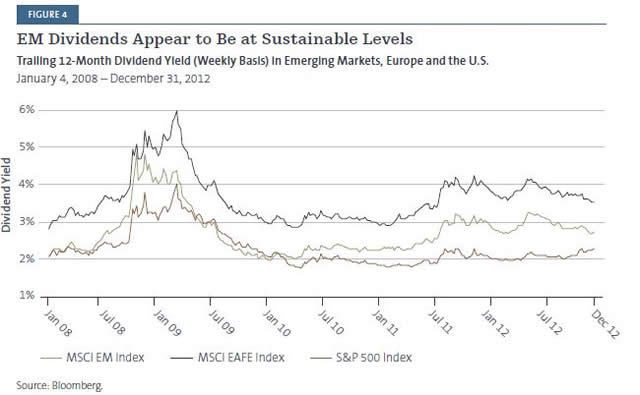

When these findings are applied internationally, emerging market equities stand out as a potential source of opportunity for dividend investors. As a group, EM equities feature a relatively low payout ratio, exhibiting sustainable dividend levels on par with those found in the United States.8 Currently, emerging market dividend yields appear to be at sustainable levels, in stark contrast to Europe, where relatively high yields and payouts point to the likelihood that dividends will be cut in the near future (Figure 4).

At the same time, EM stocks today are attractively valued, with price-to-earnings ratios that compare favorably to those in the U.S. and Europe. EM companies also boast trailing 12-month profit margins of more than 17%, easily eclipsing the 13.5% margins found in the U.S. and Europe.

In sum, EM equities offer the potential of solid growth prospects and healthy profits as well as attractive valuations and sustainable dividends. We believe this makes them a compelling value proposition for investors seeking income as well as growth potential. Investors should keep in mind the same metrics used to identify attractive dividend-payers overseas can be used in the U.S. and other developed markets as well.

Why Not Dividend ETFs?

Research on dividend yields and payout ratios can have important real-world implications for investors considering passive dividend exchange-traded funds (ETFs). With selection criteria that often rely heavily on yield picking, yield weighting or even the absolute size of the dividend, these instruments can prove risky to unwary investors.

The problem is that dividend yields can peak immediately before being reduced or eliminated. For example, many investors were lured by the 10% yields that European telecommunications companies were paying in 2011, but suffered in two ways over the following year, as yields dropped to single digits, and stock prices fell by 20-30%.9 Not only are the highest yields less likely to produce the best long-term returns, they may also signal unsustainable dividends and stock prices.

Emerging Market Corporate Bonds: The New Frontier

While many investors are increasingly comfortable investing in EM equities, they are often less familiar with the opportunities presented by corporate bond markets in the same countries. Their growing popularity is reflected in the rapid adoption of emerging market bond mutual funds and ETFs, whose numbers have increased more than five-fold over the past decade and collectively represent more than $100 billion of assets.10

Research has shown that a global equity strategy weighted on fundamentals performs better than one weighted by market capitalization.11 The reason? A fundamentals-based approach lets investors avoid misallocating resources to markets perceived as “hot,” overpriced or overvalued. Global bond markets can be viewed through the same lens. Investors in corporate and sovereign bonds tend to allocate the largest portion of their portfolio to developed markets. Yet, not only do developed nations tend to be the most indebted countries, with the most indebted companies, their economies are generally growing at a relatively slow pace, possibly hampering their ability to repay debts.

The fundamentals of EM debt markets are worth a closer look by any investor who wishes to optimize a portfolio for risk, yield and total return. Corporate use of leverage in emerging markets is half of what it is in the United States.12 External debt balances are lower, bond yields are higher and economic growth is famously robust.13

We see at least five reasons investors may want to look beyond equities and consider participating in the $1 trillion emerging market corporate bond market:14

1. Lower degree of interest-rate sensitivity relative to U.S. corporate bonds15

2. “Investment-grade” credit rating given to 52%

of bonds in the category16

3. Little local law or currency risk for corporate bonds denominated in U.S. dollars and issued under U.S. law

4. More yield per unit of duration on developed market bonds17

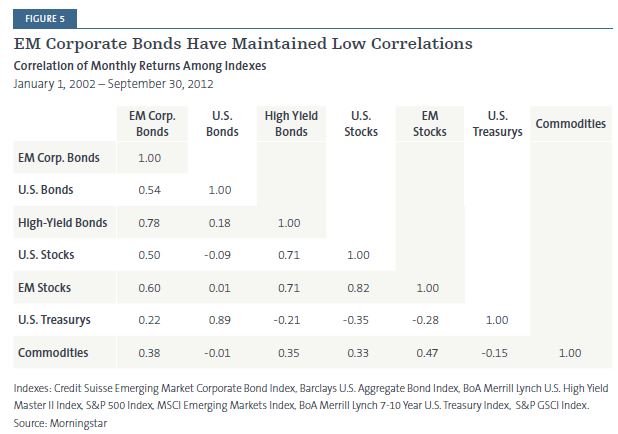

5. Low correlation to U.S. Treasurys in both rising and falling interest-rate environments18

Evaluating Options and Recognizing Risks

While new asset classes and investment strategies may improve a portfolio’s yield and total return potential, they are also subject to risks that should be taken seriously. Four types of risk are particularly noteworthy:

Interest Rates

Interest-rate risk is a prime concern for bond investors, since bond prices generally fall as interest rates rise. Skilled investment managers often seek to mitigate that risk by using interest- rate swaps and diversifying portfolios. Diversification could mean simply investing in bonds of differing maturities, or it could involve farther-reaching diversification across geographic regions, market sectors or types of securities.

Dividend-paying stocks are less likely than bonds to suffer from interest-rate risk, as they are only indirectly affected by rate changes. Since they also stand to benefit from the more rapid economic growth and higher prices typically associated with rising rates, dividend stocks can help buffer portfolios against interest-rate risk while offering attractive income potential.

Credit Quality

Credit quality has been a particular concern for bond investors in the U.S. and other developed markets since 2008, when ratings agencies began downgrading a growing number of issuers— sovereign nations and corporations as well as municipalities. Investors may be willing to accept more credit risk in a low-yield environment, but resignation is not the only choice.

With their rapid growth, robust profit margins, expanding industries and friendly government policies, corporate issuers in emerging markets continue to be upgraded, even as their competitors in the U.S. and Europe see their credit ratings slide. Almost 40% of EM corporate bond issuers are now rated A or higher, and 18% of the market is rated AA or higher.19 Additional credit analysis and astute security selection have the potential to further reduce credit risk.

Leverage

How big a role leverage played in the global financial crisis is still being debated. However, most academicians and other researchers agree that overleveraging certainly contributed to the systemic market risk that caused leverage to skyrocket when prices on risk assets plunged as liquidity evaporated. Investors and their advisors will want to keep this scenario in mind as they attempt to ascertain their true net exposure to these risks. High-yield ETFs, for example, are too new to have been tested by a market with scarce liquidity. While leverage can be a powerful and effective tool—particularly when borrowing costs are as low as they are now—it can quickly become a problem. The point is that careful monitoring and effective risk models are critical.

Correlation

Correlation risk is still fresh in the memories of all who were actively involved in the markets five years ago. Events from that time underscored how important it is to diversify portfolios, and how severely investors may be punished by inadequate diversification. Increasing global exposure is an obvious way to address correlation risks. Although the financial crisis was widely

seen as a global phenomenon, some markets, including some bond asset classes, escaped relatively unscathed, or showed positive returns. Investors may also consider adopting a more tactical and flexible approach that manages market exposure through the judicious use of long/short strategies.

Expanding the Portfolio Tool Kit

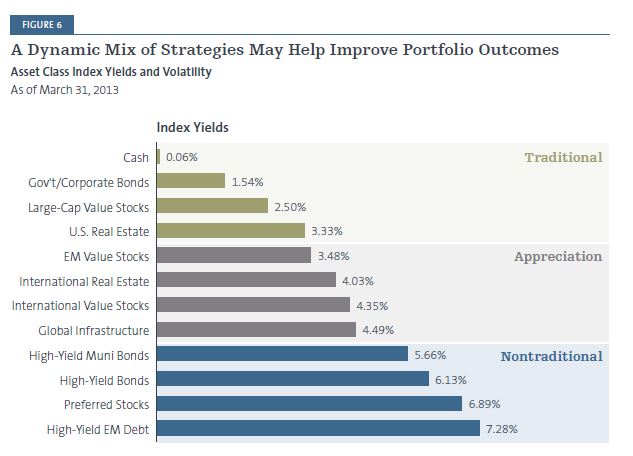

Finding reliable sources of investment income is a challenge in this low-yield environment. Based on historical analysis of asset class performance, opening a portfolio up to a broader range of asset classes and strategies can potentially increase yields while also dampening volatility ( Figure 6).

By diversifying across a blend of income- producing asset classes, investors can seek to balance their varying advantages and risks within a portfolio. Consider that:

• Traditional sources of income, like government bonds, may only provide modest yields in the current environment, but have lower overall volatility.

• Other income-producing asset classes, like real estate investment trusts (REITs), may exhibit

greater volatility but offer higher yields.

• Asset classes known primarily for their appreciation potential may in fact be attractive sources of income. Those based on hard assets, such as international real estate and infrastructure stocks, may have the added advantage of being inflation-sensitive.

• Nontraditional income sources, such as EM corporate debt, currently combine attractive yields with modest volatility and less correlated returns, as shown in Figure 6.

Avoiding the Costs of Inertia

Today, investors have unprecedented access to asset classes and strategies spanning the globe. Given the options available—and the risks associated with traditional approaches to income investing—we believe this is an opportune time for investors to revisit their portfolio allocations.

We believe that an advanced income strategy should incorporate diverse asset classes and be flexible enough to adapt to shifting market conditions. In our view, as long as risk factors for each market and strategy are adequately assessed and addressed, investors would be wise to widen their search for income.

1. Ibbotson Associates, as of 12/31/12

2. Ibid.

3. Congressional Budget Office, The Budget and Economic Outlook: Fiscal Years 2013 to 2023, February 2013

4. Ned Davis Research and Morningstar, January 1972 – March 2012

5. Ibid.

6. Credit Suisse Quantitative Research, July 2012

7. Ibid.

8. Bloomberg, as of 12/31/12

9. Archibald Preuschat, “Investors Hang Up on Europe’s Telecom Stocks,” The Wall Street Journal, January 28, 2013

10. Strategic Insight, as of 03/31/13

11. Robert D. Arnott, Jason Hsu, Phil Moore, Fundamental Indexation, 2005

12. David Wilton, “Emerging Market Private Equity: The Opportunity, The Risks & Ideas to Manage Them,” International Finance Corporation, January 2012

13. International Monetary Fund, World Economic

Outlook Database, October 2012

14. JP Morgan, as of 11/21/12

15. Bloomberg, as of 04/10/13

16. Credit Suisse EM Corporate Debt and Bank of America Merrill Lynch EM Corporate Plus Bond Indices, as of 12/31/12

17. Credit Suisse and Bank of America Merrill Lynch, as of 12/31/12. Yield per unit of duration is calculated by dividing yield to maturity by modified duration. Calculations were performed using data published by Credit Suisse and Bank of America Merrill Lynch. For more information on ratings and analytics related to the indexes, refer to the websites of Credit Suisse and Bank of America Merrill Lynch.

18. Bloomberg, as of 04/10/13

19. Credit Suisse EM Corporate Debt and Bank of America Merrill Lynch EM Corporate Plus Bond Indices, as of 12/31/12

Definition of Terms

A/AA are Standard & Poor’s long-term credit ratings that reflect a bond issuer’s financial strength, or its ability to meet its financial commitments in a timely fashion. AA is given when an issuer’s capacity to meet its long-term debt obligations is extremely strong, while A indicates a strong repayment capacity.

Correlation is a statistical measure of how two securities move in relation to each other.

Dividend yield is a financial ratio that shows how much a company pays out in dividends each year relative to its share price.

Duration is a measure of the sensitivity of the price (the value of principal) of a fixed-income investment to a change in interest rates.

Investment grade refers to the quality of credit, and indicates that a company or bond has a relatively low risk of default.

MSCI EAFE Index is a stock market index that is designed to measure the equity market performance of developed markets outside of the U.S. and Canada.

MSCI Emerging Markets Index is a free float- adjusted market capitalization index that is designed to measure equity market performance in the global emerging markets.

Price-to-earnings (P/E) ratio of a stock is a measure of the price paid for a share relative to the annual income or profit earned by the firm per share.

S&P 500 Index is an unmanaged index of 500 common stocks chosen to reflect the industries in the U.S. economy.

Short selling is the practice of selling a financial instrument that the seller does not own at the time of the sale. Short selling is done with intent of later purchasing the financial instrument at a lower price.

Valuation is the process of determining the value of an asset or company based on earnings and the market value of assets.

One cannot invest directly in an index.

You should consider the investment objectives, risks, charges and expenses of the Forward Funds carefully before investing. A prospectus with this and other information may be obtained by calling (800) 999-6809 or by downloading one from www.forwardinvesting.com. It should be read carefully before investing.

RISKS

There are risks involved with investing, including loss of principal. Past performance does not guarantee future results, share prices will fluctuate and you may have a gain or loss when you redeem shares.

Borrowing for investment purposes creates leverage, which can increase the risk and volatility of a fund.

Foreign securities, especially emerging or frontier markets, will involve additional risks including exchange rate fluctuations, social and political instability, less liquidity, greater volatility and less regulation.Short selling involves additional investment risks and transaction costs, and creates leverage, which can increase the risk and volatility of a fund.

Alternative strategies typically are subject to increased risk and loss of principal. Consequently, investments such as mutual funds which focus on alternative strategies are not suitable for all investors.

Diversification does not assure profit or protect against risk.

There is no guarantee the companies in our portfolio will continue to pay dividends.

© Forward Management