Did you know that in the first half of the last century, Myanmar had twice the GDP per capita of China? What a difference a few decades and government policies make, as China is ten-fold the size of Myanmar today, according to UBS Research.

The change in wealth between the two nations is a prime example of how government policies can have a tremendous effect on a country’s growth.

Now, after the West temporarily lifted its sanctions against investment in Myanmar last year, global investors have been rushing in to gain access to this fertile land. Multinational companies such as Coca-Cola and Unilever are eager to get their products in the hands of its 55 million residents.

Over the next decade, these two firms will be spending $1 billion, reports the Wall Street Journal.

This is an exciting development for global companies looking to expand their reach, but investors don’t necessarily have to buy multinational businesses to access this untapped growth.

Many companies located in Southeast Asia have plans in place to expand into Myanmar, according to our China Region Fund (USCOX) portfolio manager Michael Ding. Businesses in Thailand have a geographic advantage and companies in Indonesia benefit from the growing economy. Michael says this theme is embedded in the fund, as about 10 percent of the portfolio has an indirect route to Myanmar’s growth.

This is an exciting area of the world these days, as the geopolitical and economic organization called the Association of Southeast Asian Nations (ASEAN) prepares to become one market by 2015. The association was formed in 1967, comprising original members Indonesia, Malaysia, the Philippines, Singapore, Thailand and Brunei (otherwise known as ASEAN-6), with Cambodia, Laos, Myanmar and Vietnam becoming later additions (i.e., CLMV).

click to enlarge

The ASEAN area offers a treasure trove of strengths for investors, including solid demographic trends, an aspirational middle class, strong fiscal and monetary policies, and government support for greater integration, free trade and political stability among the area’s countries.

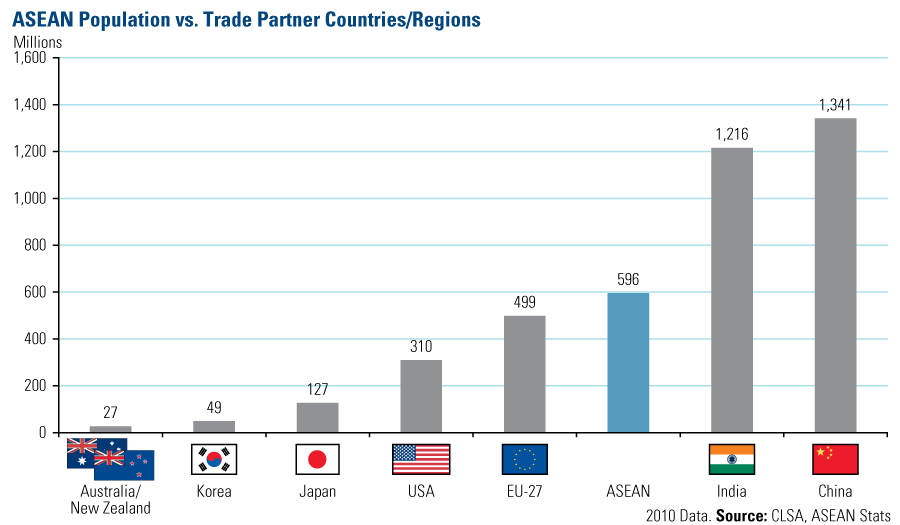

As a group, ASEAN has the third-largest population in the world, after China and India. China and India each have a population of about 1.3 billion people; the ASEAN countries collectively have nearly 600 million. This is about 100 million more people than the 27 countries in the European Union.

click to enlarge

Indonesia makes up 40 percent of this number, with a population of 250 million. The Philippines is the second-largest ASEAN country, with 105 million and Vietnam is the third largest, with 92 million.

Together, Indonesia, the Philippines and Vietnam comprise two-thirds of the ASEAN population and GDP, according to Bank of America Merrill Lynch (BofA-ML).

ASEAN’s residents are young, too—37 percent are, on average, under 20. The mean age is 30 years, which is significantly lower than Japan’s 44 years.

And a young population translates to a growing labor force. Looking at people aged 15 to 64, the countries that comprise the ASEAN will grow 1.4 percent annually over the next 10 years, “increasing by 56 million people to 444 million,” says CLSA. By contrast, Japan’s workforce is expected to decline 1 percent each year.

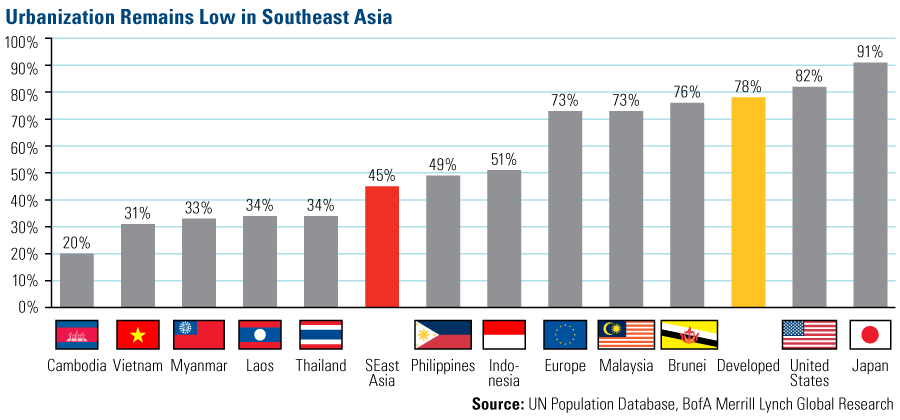

click to enlarge

Urbanization levels are currently low compared to developed areas of the world, which offers potential for infrastructure buildout and increasing domestic consumption. Only 45 percent of people in Southeast Asia live in an urban area, compared to 78 percent for developed markets. Only 20 percent of Cambodian residents live in an urban area; the urbanization rate in Vietnam, Myanmar, Thailand and Laos is around 30 percent, with the rate of urbanization rising quicker in many of these ASEAN countries compared to developed countries.

click to enlarge

But perhaps ASEAN’s most important strength is the steps the group is taking to encourage trade and improve infrastructure, including roads, railways, airports and ports, to support cross-border cooperation. One of the steps included removing tariff barriers. According to BofA-ML, “ASEAN-6 has achieved zero tariffs for 99 percent of goods and CLMV 0-5 percent tariffs for 98 percent of goods.”

This integration is beginning to have an affect on intra-regional trade and investment, with the share of intra-ASEAN trade rising to about one-quarter of total trade in 2010, “up from 22.4 percent in 2002,” says BofA-ML.

One of the many companies that is poised to benefit from increased domestic wealth and greater trade is Airports of Thailand (AOT). The company handles about 85 percent of Thailand’s air traffic, making it a “near-monopoly” and the “main beneficiary of higher demand for air travel,” says CLSA. With the implementation of regional economic integration, we expect there to be greater trade, a greater flow of people and goods, “supporting more traffic growth into and out of Thailand.”

© US Global Investors