Executive Summary

- Though markets were whipsawed by the announcement, the Fed’s plan to step aside and allow normalization is a good thing.

- The primary risk to hedge is now economic growth and the strong equity returns it tends to produce — not financial Armageddon.

- While risks in Europe and China persist, U.S. fundamentals look relatively strong.

- It’s not too late for investors to move away from defensive positioning and back toward a standard allocation.

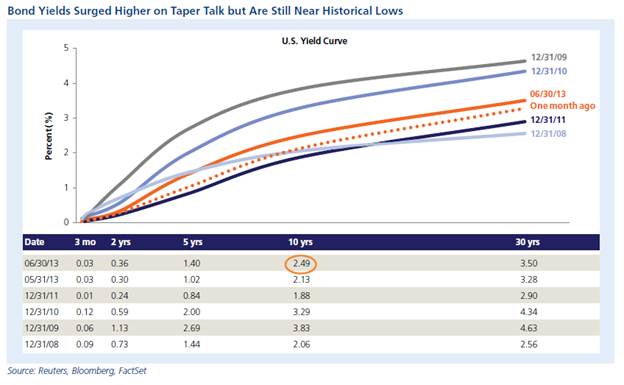

“Normal” is the economy’s goal. Getting back there is likely to be ugly; in fact, it already has been, especially for the fixed income market. But a return to normal is essential in order to gain clarity on our problems and to implement the policy responses that will guide us back to trend-level growth with plentiful and meaningful jobs, a higher standard of living and ultimately increased wealth. In June, the Fed announced its intention to at some point step aside and allow this normalization. The Fed made the right decision at the right time; given the “diminished risks” that are evident, to delay is to allow for unintended consequences, asset bubbles and other excesses. We have been there before, and it is worse than the pain of the cure.

The market was surprised — as were we — by the Fed’s announcement of a prospective 2014 date for the end of the its “unconventional policy” of quantitative easing. Fixed income securities of all stripes were hammered, gold dropped like a rock, and the U.S. dollar strengthened on the news. The revelation also hit emerging market equity, bond and currency markets particularly hard, throwing investment flows into reverse. In a classic case of “gaming diversification”, it wasn’t so much rising yields that caught many investors unprepared — that was expected to happen eventually — but the speed at which they turned.

Equity Is a Hedge for Bonds and a Market “Melt-Up”

Think about it. We have had an overnight regime change in terms of the primary risk to hedge. Potential financial Armageddon had been the biggest concern for the past five years, and bonds have been the supreme asset class to hedge this risk. But what investors failed to understand is that not only do equities serve as a hedge against bonds in a rising-rate environment, they are also a hedge to a market “melt-up”, participating in the economic growth that tends to produce strong returns. Cash may be a good hedge against interest rate risk, but as a stagnant asset it’s useless in hedging growth — and a big mistake for investors. For example, those who waited to be fully allocated to equities got hit with a double whammy in 2013, lacking a sufficient hedge both to interest rate risk and to a growing economy with diminished risks. Yes, equities initially dropped on the FOMC’s news, but they have been recovering quickly; the same can’t be said for bonds.

In fact, our equity model portfolio outperformed our fixed income model by 200 basis points in the second quarter and by more than 1,000 basis points in the first half of 2013, a sure first over the five years since the financial crisis. A more cogent description is that “safe” bond investors lost 3.8% YTD, while “risky” equity investors gained 6.3%. The overall model portfolio delivered an unimpressive yet positive 2.3% year to date. Now, that is a hedge — just not to the risk that many investors had been expecting.

Global Risks in Europe and China Persist

Though the U.S. is getting back to normal — certainly important for global growth since it is the largest economy in the world and keeper of the global reserve currency — it is still not enough. Here are some concerns:

- Europe is close to its seventh consecutive quarter of contraction, with unemployment of 12.1%.

- Bond yields in June surged for Italy, Spain, Portugal and Greece.

- China’s interbank lending rate skyrocketed, as the central bank triggered a cash crunch by refusing to inject funds into the system.

- China’s runaway growth in lending on wasteful and unproductive projects is leading to 2008-style credit crunch, impeding future growth and spending.

- China’s Shanghai equity market plummeted 14% in June and set off contagion in emerging markets.

Market Fundamentals Holding On

The fundamentals are about to undergo a test. Will a near-1% increase in mortgage rates stop the housing market’s rebound? Though the shock of sharply higher rates may result in a temporary slowdown, we think growth will resume once buyers digest the fact that rates are still near historical lows. The ABCDs of fundamentals, meanwhile, appear to be holding their own.

Advancing earnings growth. With the first quarter of 2013 now complete, year-over-year earnings growth, at 3.5%, exceeded expectations. The market will now re-focus and perhaps re-energize based on second quarter earnings, which begin in earnest this month. Expectations are again low; second quarter growth is forecast at only 0.8%.

Broadening manufacturing. June saw manufacturing activity rebound sharply after hitting a four-year low in May. The ISM index of factory activity rose to a better-than-expected 50.9% in June, with strong growth in the new orders component of the index.

Consumer as the game changer. The consumer machine may have slowed in the first quarter, as evidenced by the fact GDP growth was ratcheted down to 1.8% thanks mostly to a downward revision to consumer spending data. Second quarter data have pointed to somewhat of a rebound, however. Retail sales reached an all-time high of $421 billion in May, while consumer confidence as measured by the University of Michigan remained near six-year highs at the end of June. The housing market has continued to surge, with the S&P/Case-Shiller index of home prices posting the largest month-to-month increase in its history as well as a 12% year-over-year increase.

Developing markets. The BRIC countries — Brazil, Russia, India and China — slammed into a wall this year, as the MSCI BRIC Index was down more than 12% in the first half and investors have been heading for the exits. The global economy appears to be in the midst of a shift; while the BRICs may have become complacent in their rapid growth, there are plenty of other economies — especially in Latin America and Southeast Asia — that are clamoring to become the next emerging markets. Remember: The developing and emerging economies account for 80% of the world’s population but only 35% of its economy. The growth story is far from over.

Moving from Gaming Diversification to Effective Diversification

Investors overexposed to safety in the first half of 2013 should have learned a valuable lesson about the folly of gaming diversification; yet, a hope persists that bond yields will drop. Expecting such a move would be a mistake. Markets tend to provide investors with a “shot across the bow” to wake them up, which is what happened in June; if no action is taken, the shot become more like bazooka fire. The risk for investors is no longer Armageddon, it’s underexposure to equities. It is not too late for investors to position themselves appropriately for their goals by rebalancing back to a standard allocation, such as a 60% equity/40% bond ratio.

It has been an arduous, unusual and unconventional five-year journey for the markets. Normal has never been so welcome. This year markets have had a stealth rally toward risk, in particular upside risk — a risk investors should be excited to hedge. For the first time in many years, equities are likely to become popular again, and that is normal.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 6863