Alternative Energy Brief: EU Solar Tariffs “a big mistake.”

EU Tariffs on Solar

The European Union (EU) have introduced a temporary 11.8% tariff on imports of Chinese solar panels with the threat of an increase to 47% if some compromise is not reached by August. The path to get here has been tortuous. German solar module manufacturers complained that Chinese module manufacturers were receiving illegal subsidies and dumping panels into Europe. The EU has agreed and proposed high tariffs of 47% on imports of Chinese solar modules. Interestingly, 18 of the 27 EU countries opposed this high tariff level, including Germany, which has led to the compromise of the

11.8% rate as a negotiating position.

The Chinese have, in retaliation, threatened to impose tariffs on imports of wine from the EU. This would directly hit the countries who are believed to have been supportive of the tariffs—France, Spain and Italy. Amusingly, the EU commissioner leading the push for tariffs, Mr Van der Gucht, owns a vineyard in Italy.

Our view is that the tariffs are a big mistake, first, because the accusations of illegal subsidies and tariffs do not stand up to cursory review. International solar companies all receive some form of subsidies, as witnessed by the US grant program, which gave over $500 million to Solyndra. In China, the main forms of subsidies are loans from Chinese state banks. These are at market rates which are typically in the 6% to 10% range, far in excess of the cost of subsidy finance available in the US and Europe. On dumping, the Chinese are selling modules in their home market at lower prices than they sell them for in Europe, and it is a highly competitive commoditised market where 10 or more major Chinese module competitors compete aggressively for every contract. That is the reason why prices have fallen, not as a result of a dumping strategy to gain a monopoly position.

The second reason why we believe that tariffs are a mistake are because we think they will not have the desired effect. If Chinese modules are subject to high tariffs, module prices in Europe should go up, which could increase electricity costs and lower installation volumes, potentially damaging local installations firms where the bulk of employment in the industry lies. Manufacturing could shift from China to low cost manufacturing countries without tariffs, and these are typically not in Europe. There may not even be any protection for the European manufacturing industry, and the EU solar installation industry could suffer.

What will happen next? It is hard to see a happy outcome in the near term. There is little that the Chinese government can do to impact the prices Chinese companies sell at in Europe, and it is not offering any subsidies to manufacturers that it can stop offering. The often touted suggestion that minimum prices are introduced is not a sensible solution—this will be good for profits at Chinese manufacturers but would harm the EU solar installation industry. We think that access to the growing Chinese market is the best that the EU can strive for. If the tariffs do go up to 47%, this will be damaging in the short term for the European solar industry, but I believe the tariffs would be over- turned in December by a vote of the European countries.

On a positive note, the US and EU are engaging further with China on how to move forward for this industry. These tariffs are ultimately a tax on domestic energy consumers, and, in our opinion, the sooner we can move on from proposals for trade tariffs the better.

Module prices rising

Over the last quarter, module prices have increased from the lows for Chinese modules of 64c to 78c (source: Bloomberg New Energy Finance). This has been as a result of strong demand, inventory from the first quarter being worked through and many second and third tier manufacturers ceasing production. While we expect prices to decline over the long run, the current pricing level allows for better profitability at module manufacturers. We believe that polysilicon prices are unlikely to fall dramatically from current levels and are therefore not going to support continuing production if module prices fall. Overall, we believe this could lead to better earnings numbers in the second half of 2013.

Japanese solar market poised for growth

Cumulative capacity approved for Feed-in Tariffs in Japan increased by over 7.5 gigawatts (GW) in just the first quarter of 2013. Expectations are for 6GW to 9GW of installations in 2013 in Japan.

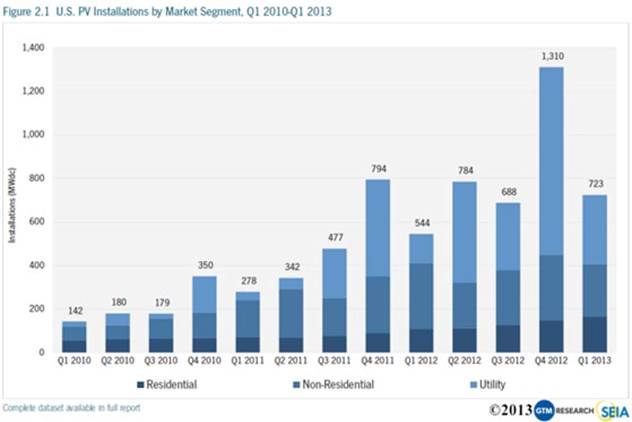

US solar market has continued to grow

As shown in the above chart, US installations are growing substantially; even the seasonally weak first quarter showed installations of 723 milliwatts (MW). The same report forecast 4.4 GW of installations for 2013—our expectation is that the actual level could be higher than that as new business models such as that used by Solarcity become more established and utility programs ramp up as a result of much lower installation costs.

Opinions expressed are subject to change, are not guaranteed and should not be considered investment advice.

Distributed by Quasar Distributors, LLC

© Guinness Atkinson Asset Management