ING Fixed Income Perspectives June 2013

Bond Market Outlook

Global Interest Rates: Fears of Fed tapering are overblown; we expect global funding conditions to remain easy.

Global Currencies: We continue to favor the U.S. dollar and are bearish on the euro and the yen; we are cautious on EM local currencies, as volatility is likely to persist.

Corporates: Spreads are appealing at current levels, with higher-quality industrials offering the most attractive risk/reward.

High Yield: Prices have pulled back of late, though we have not seen any material degradation in credit fundamentals.

Mortgages: Prepayment fears have eased, and the housing recovery and liquidity dynamic are supportive; tapering and higher interest rates will cause volatility.

Emerging Markets: EMD will continue to be impacted by benign global growth expectations and higher developed market rates, encouraging near-term caution.

Macro Overview

- Apparently, April showers bring not May flowers but rather May flows — out of U.S. Treasuries and a wide variety of global assets with positive income characteristics. The Bank of Japan provided the global economy with a burst of liquidity with its early-April announcement of an ambitious monetary stimulus plan, driving bond yields lower and fixed income prices higher. By early May, however, investors began to question the efficacy of “Abenomics” given its to-date lack of real pro-growth policies and fiscal reforms, inspiring a sharp selloff in global duration and bond markets that was exacerbated by mounting unease about the eventual end to the Federal Reserve’s bond-buying program.

- The simultaneous cheapening of both safe-haven assets and riskier investments reflected a re-pricing of global fixed income across the risk spectrum despite no real changes to global liquidity conditions or the economic paradigm upon which ample central bank accommodation is built. As Bernanke reminded us in mid-June, the philosophy that drives $85 billion of agency MBS purchases per month is unlikely to be revised anytime soon; all else equal, the data — from economic growth and inflation to unemployment and wages — point to a consistent level of U.S. accommodation, with a liquidity boost from other central banks like Japan.

- Just as the introduction of quantitative easing acted as a volatility suppressant in global debt markets, the threat of its removal has acted as an accelerant; the ten-year U.S. Treasury, for instance, sold off 60 bps on the belief that Fed tapering could occur. However, we believe markets have misjudged not only the timing of an eventual unwind but also its potential impact; given global deflationary pressures, we would expect fixed income assets to richen, not cheapen, and for equities to wilt with vigor were central banks to slam the brakes on QE rather than slowly ease off the accelerator.

- As markets spend the near term debating the duration and efficacy of global monetary policy, our bias is to proceed with caution while taking advantage of the mispricings that have driven down prices on many fundamentally attractive asset classes, particularly spread sectors like U.S. high yield.

Sector Overviews

Global Interest Rates

- Weak global growth and benign inflation are likely to continue in the second and third quarters of 2013. We expect global funding conditions to remain easy, with the ECB and emerging market central banks adding to the liquidity. Fears of Fed tapering are overblown, and the Fed also remains committed to keeping short-term rates down; in other words, the Fed is more likely to be late than early in removing monetary accommodation. The May selloff, which accelerated through June, sent valuations into fair or slightly cheap territory for the first time in two years; they seem likely to retrace in the near term.

- We have a bullish long-term view on Japan’s political commitment to a supportive fiscal stance and structural reform — the two remaining arrows in Abe’s quiver next to monetary stimulus — but remain bearish on Japan and most other developed government bonds (e.g., France, Italy and Spain) relative to higher-yielding emerging markets that are exposed to U.S. growth, like Brazil and Mexico.

Global Currencies

- We maintain that the U.S. is the most credible growth and recovery story in the developed world. This will support the U.S. dollar, though upside will be limited thanks to weaker global growth expectations, falling commodity prices and a re-affirmation by the Fed that monetary stimulus will remain firmly entrenched given high unemployment and inconsistent growth.

- We continue to favor higher-yielding currencies that will benefit from U.S. dollar strength, like the Brazilian real and Mexican peso, as well as lower-beta currencies like the Chinese renminbi and Malaysian ringgit given yield and diversification benefits. We remain broadly bearish on developed market currencies like the euro, pound sterling and Japanese yen.

Investment Grade Corporates

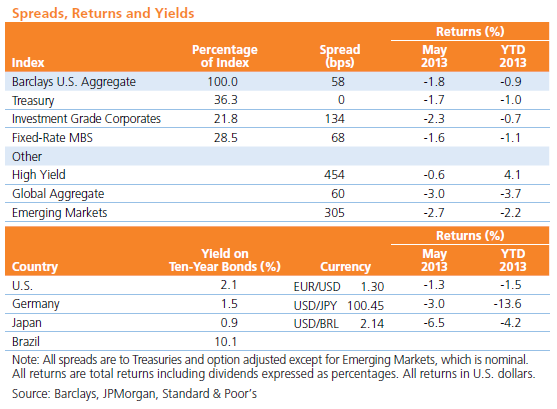

- Beginning the year at around 140 bps, corporate spreads set a new post-crisis low of 130 bps in mid-May. However, they have since widened beyond early-2013 levels, driven by concerns of Fed tapering and the increase in macro volatility. Financials and utilities have led in terms of excess returns this year. The recent back-up in spreads has been relatively uniform across the major industry categories, but longer-dated securities have suffered the most given the rate move and credit curve steepening. We find corporate spreads appealing at these levels, with higher-quality industrials perhaps offering the most attractive risk/reward.

High Yield Bonds

- High yield corporates saw a more material re-pricing. The yield to worst on the Barclays High Yield Index backed up over 1%, with option-adjusted spreads versus Treasuries widening as well. Liquidity-driven selling to satisfy extremely large retail outflows (outflows were a record $4.63 billion for the week ended June 5) has continued to pressure the asset class. We are still seeing significant day-to-day and intra-day volatility, which will likely continue until outflows subside. The fundamental picture remains intact, with no signs of material degradation in credit fundamentals.

Mortgages

- Agency RMBS cheapened as Treasury rates tracked higher, pushing the primary mortgage rate to the highest level in more than a year. This has helped alleviate prepayment fears and together with substantially cheapened valuations led to improved market sentiment and investor appetite. Near term, agency RMBS performance will continue to be dominated by the direction of interest rates, volatility and market concerns over stimulus tapering.

- Non-agency RMBS, supported by the recovering housing market and strong technicals, capped an aggressive run stretching back to early 2011. While fundamentals have remained supportive, the technical picture has deteriorated significantly, as investors sold non-agency gains to cover agency losses. As a result, the current market sees very little liquidity, and yields have given back some of the early-year run.

- Like non-agencies, CMBS have also been impressive since early 2011, supported by the recovering commercial real estate market and strong technicals. Its technical picture, too, has decayed, albeit not as significantly as non-agency RMBS.

- ABS, while well-supported fundamentally, labored under a less favorable technical environment for most of 2013, generatingonly modest year-to-date gains and underperforming most risk markets. ABS spreads have proved resilient since April, however, attracting safe-haven flows as risk appetites receded across other markets.

Emerging Markets

- The sharp selloff since mid-May was largely driven by concerns about an earlier-than-expected start to Fed tapering, though other factors — including Turkish political uncertainty, Japanese market volatility and fears of tightened liquidity conditions in China — have also come into play. Emerging corporates are trading at the wide end of their post-crisis range versus domestic markets, which is likely warranted due to weaker global growth relative to the U.S. as well as commodity weakness. The selloff in emerging sovereigns and local-currency markets does present some opportunities, but volatility likely will continue near term.

ING U.S. Investment Management’s fixed income strategies cover a broad range of maturities, sectors and instruments, giving investors wide latitude to create a new portfolio structure or complement an existing one. We offer investment strategies across the yield curve and credit spectrum, as well as in specialized disciplines that focus on individual market sectors. We build portfolios one bond at a time, with a critical review of each security by experienced fixed income managers. As of December 31, 2012, ING U.S. Investment Management managed $127 billion in fixed income strategies in the United States.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 6795