Gold’s 2013 fall has been the lone development in the two-year commodities decline that seems to have captured much attention. The CRB Raw Industrials—a spot index of 13 commodities exhibiting a much tighter linkage to the global economy than gold—peaked in mid-April 2011, coinciding with the bull market relative strength highs in the both S&P 500 Energy and Materials sectors (Chart 1) and the “absolute” price highs in the MSCI stock market indexes of commodity exporters Brazil, Canada and Russia. If one failed to bail out near the 2008 commodity peak, the spring of 2011 offered a second chance to unload physical commodities, commodity stocks and even commodity “countries.”

Chart 1

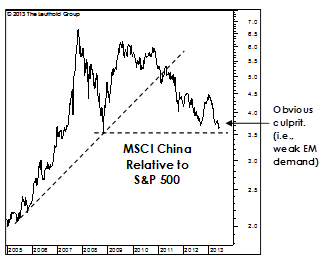

China’s loss of industrial momentum (while difficult for both us and Chinese officials to quantify) is no doubt a key culprit behind the two-year slump in many key commodities. But we don’t believe that weak industrial commodities prices are primarily a “China” problem—or even, more broadly, a demand problem. Neither we nor Chinese policymakers have a good handle on what its economy might do in the second half. But the problem is bigger than any short-run shortfall in demand. Supply—specifically, the newfound abundance of it in many commodity-oriented industries—could subvert any price rebound that might have normally resulted from an acceleration in Chinese manufacturing and construction.

Chart 3 shows global Energy and Materials sectors ramped up capacity aggressively in the final phase of last decade’s commodity boom. As if that “hangover” level of capacity overhang weren’t enough to contend with, the rate of Materials sector expansion (based on the capex-to-depreciation ratio) actually exceeded its pre-bust peak early on in the current recovery. (Energy sector spending has recovered as well, though not to 2007-2008 levels.)

Chart 3

In short, commodity producers seem to believe that last decade’s commodity boom is set to repeat. This belief itself (manifested in high capital spending) probably ensures that it won’t.

Relative Pricing Power : Commodity stocks (broadly defined to include both Energy and Materials) have historically tended to outperform when the rate of PPI inflation exceeds CPI inflation (i.e., when the spread shown in the bottom panel of Chart 4 is negative). Today’s positive CPI-PPI spread tends to favor both the profitability and relative stock market action of consumer-oriented stocks (both Consumer Staples and Discretionary).

Commodity Prices Versus Commodity Stocks : We’ve previously examined the linkage between Materials stocks and industrial commodity prices, hoping to identify a reliable lead-lag relationship between the two. Unfortunately , there’s no consistent tendency for one to lead the other at important inflection points. In 2011, astute investors might have correctly viewed Materials stocks inability to “confirm” the CRB Raw Industrials’ new inflation-adjusted high as a long-term bearish sign for the sector. In our opinion, it’s not too late to adopt this bearish view.

© Leuthold Weeden Capital Management