Sharing some commentary from our friends at TrimTabs, which summarizes a few changes in the investment landscape that may give you an indication of what to expect following May’s “sell in May and go away” trading adage. TrimTabs research focuses on fund flows and float shrink. They believe the market is heavily influenced by what people and institutions are doing with their dollars. You can read more about the research behind float shrink at AdvisorShares.com.

The S&P 500 Index rose 2.10% in May 2013, its seventh consecutive monthly gain. While “sell in May and go away” has not worked well so far this year, what should investors expect for June? We do not try to do short-term market timing at TrimTabs, but historical data helps put the situation into perspective. Since 1950, the S&P 500 Index has risen in seven consecutive months 14 times, or roughly once every 4.5 years. Eight-month rallies occurred eight times (the last ended in January 2007). On the other hand, declines in consecutive months are far rarer. Since 1950, the S&P 500 Index fell for seven straight months only once.

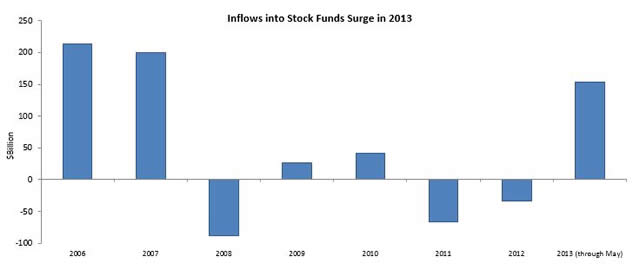

Although the S&P 500 Index is up 14.34% so far this year (as of 5/31/13), investors have reasons to remain positive on stocks. Inflows into equity mutual funds and ETFs reached $154.4 billion in the past five months, the strongest buying since 2007. Corporate balance sheets are in much better shape than they were in 2007, as companies are sitting on record amounts of cash. In addition, inflation remains minimal. Consumer price inflation in the U.S., Europe, and Japan trended lower in recent months.

Source: TrimTabs Investment Research

Past performance is not indicative of future results.

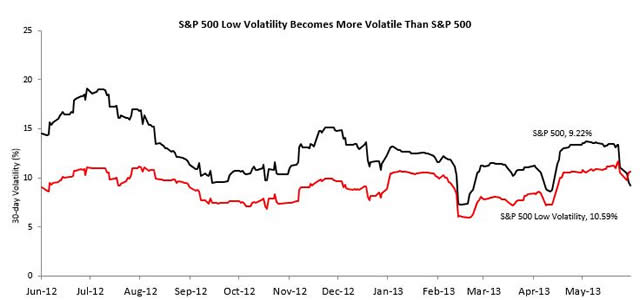

Equity investors should pay attention to a few changes to the investment landscape. First, the volatility of low volatility stock strategies is now higher than for the benchmark (the 30-day volatility of the S&P 500 Low Volatility Index was 10.59% in May versus 9.22% for the S&P 500 Index). Low volatility strategies attracted huge inflows in the past few years. In a correction, investors who piled into these strategies may be unpleasantly surprised. These strategies typically assume volatility is stable, but in reality, a low volatility strategy’s volatility relative to that of a benchmark is almost certain to change.

Source: Bloomberg

Past performance is not indicative of future results.

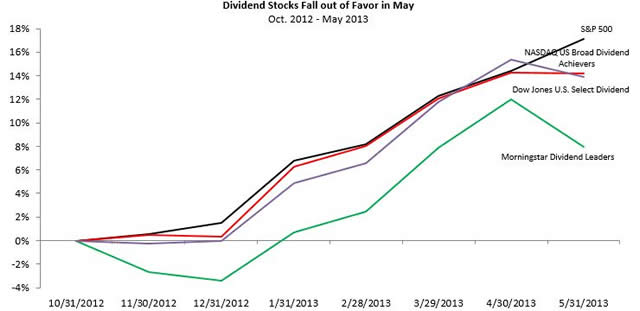

Second, dividend-paying stocks have fallen out of favor. Several major dividend stock indices sold off hard in May. Investors have been fleeing stocks with higher yields as bond yields back up.

Source: Bloomberg

Past performance is not indicative of future results.

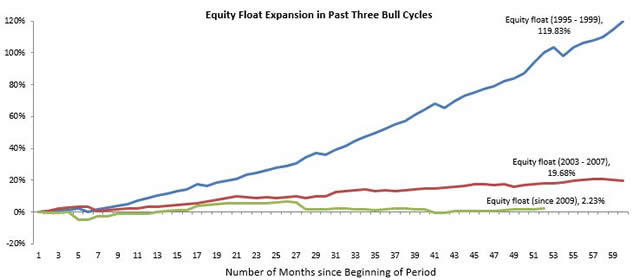

Third, the tradable equity float (measured using the float of the Russell 3000 Index) expanded 0.54% year-on-year in May, up from 0.17% year-over-year in April. The equity float is increasing for the first time in two years. All else being equal, if the same amount of money chases fewer shares, the share price increases. New share issuance ultimately dilutes the value of existing shares, and companies and insiders are taking advantage of current stock prices level to sell. Since 2009, the float has expanded only 2.23%, down from 19.68% from 2003 to 2007. Limited float growth is vital to the current bull market. Investors should turn more cautious if float expansion accelerates.

Source: TrimTabs Investment Research

Past performance is not indicative of future results.

Dividend yields have lost much of their allure as a predictor of equity returns because companies have changed their payout practices. For example, S&P 500 companies distribute only 40% of their total payout as dividends. The rest is paid out through share buybacks.

Since corporate America is sitting on a record amount of cash, a “total payout” approach makes more sense than a dividend-only focus. There are many high dividend strategies investors can pair with the fund to build the core of a “total payout” portfolio. Mostly importantly, we select stocks based on float reduction, not just stock buybacks.

Definitions

The S&P 500 Index is a free-float capitalization-weighted index based on the common stock prices of 500 American companies. It is one of the most commonly followed equity indices and many consider it the best representation of the market and a bellwether for the U.S. economy.

Volatility is a statistical measure of the dispersion of returns for a given security or market index. Volatility can either be measured by using the standard deviation or variance between returns from that same security or market index. Commonly, the higher the volatility, the riskier the security.

The S&P 500 Low Volatility Index measures the performance of the 100 least volatile stocks in the S&P 500. The index is designed to serve as a benchmark for low volatility or low variance strategies in the U.S. stock market.

Constituents are weighted relative to the inverse of their corresponding volatility, with the least volatile stocks receiving the highest weights.

Float is the total number of shares publicly available for trading. The float is calculated by subtracting restricted shares from shares outstanding.

Tradable Equity Float (Public Float) is the number of shares publicly owned and available for trading. Floating shares are included in the calculation of a company's outstanding shares, along with restricted stock. Restricted stock is only available to company insiders, like employees and executives. It is not freely traded among the public and is subject to special Securities and Exchange Commission restrictions. Unlike floating stock which is freely tradable.

A Buyback is the repurchase of outstanding shares (repurchase) by a company in order to reduce the number of shares on the market. Companies will buy back shares either to increase the value of shares still available (reducing supply), or to eliminate any threats by shareholders who may be looking for a controlling stake.

The performance of High Dividend Equity Strategies is calculated as the average of ten high dividend indices which has at least one ETF with a minimum of $100 million AUM tracking it.

The Russell 3000 Index measures the performance of the largest 3000 U.S. companies representing approximately 98% of the investable U.S. equity market.

This communication is a publication of TrimTabs Asset Management. It should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. Information presented does not involve the rendering of personalized investment advice. Content should not be construed as an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein. Performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing performance returns. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Past performance may not be indicative of future results. Therefore, no investor should assume that the future performance of any specific investment or investment strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions, may materially alter the performance of an investor's portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for an investor's portfolio.

© AdvisorShares