All markets came under pressure last week (and this morning) over the dual concerns of a slowing global economy coupled with the Federal Reserve’s suggestion that things are improving and thus “tapering” might start by the end of the year.

The two notions are, of course, contradictory, but combined sent bond, stock and commodity markets reeling. It has also had the effect of raising the dollar’s value. In short all of the market signs show concern over deflation - something which theFed’squantitative easing was meant to combat.

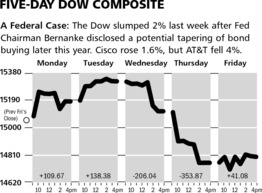

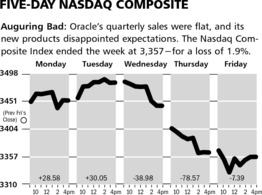

The result last week as shown in the above charts was for the Dow Jones Industrial Average to decline by 1.8%, while the NASDAQ Composite fell by nearly two percent.

The Markets & Economy

As I said a few weeks ago, the Fed could hint at a forthcoming policy, but risked credibility (as witnessed by the market’s reaction) if it were to do so. The reason I said this is clear. Notwithstanding the question of whether or not QE was good and/or effective economic policy, the Fed undertook it to accomplish its dual mandate.

That mandate is to achieve full employmentand to operate at a low inflation rate which is defined as 2% or slightly above. Currently, the unemployment rate has ticked up to 7.6% and in my view is on its way higher by year end. At the same time inflation has fallen below the 2% threshold and given market reactions is likely to fall further this summer.

The Fed itself acknowledged this inconsistency but just thought the summer would be better and thus set the stage for tapering to begin. Remember the Fed has made the same rosy forecast three summers in a row and been incorrect each time. You would think they would learn.

Just this morning the President of the New York Federal Reserve Bank stated the Fed was not sufficiently accommodative with its monetary policy. This represents, already, the beginning of the “walk back” of the damage done by last week’s presentation.

Look for bond yields of all types to remain under pressure from margin and other forced selling, but ultimately bond prices will recover as the notion gains traction that the Fed’s statement last week was borderline nonsense. The US economy will be lucky to see 2% growth for all of 2013, and next year looks bleak as well with the looming regulations and taxes associated with Obamacare.

Remember, in this crazy upside down world, last week’s overly rosy view of the economy was bad news for the markets. As this is shown to be incorrect, the more pessimistic view will turn out to be good for stocks. How long and to what extent the market prices correct is the unknown question at this point.

What to Expect This Week

The tremors from last week’s Fed meeting as well as increasing worries about the Chinese banking system (another oldie but goodie) have markets on edge. With the dollar rising and interest rates having backed up so quickly, I look for the US bond market to be your first market to stabilize.

The so-called growth scare last week will be replaced by concern over the economy. That will help defensive names but continue to weigh on cyclical and commodity markets, although they are pretty oversold.

Behind the scenes the central banks will do what they can to restore confidence. After all they have printed trillions of dollars and other currencies over the past few years and without a bona-fide inflation threat, they will do more with impunity. That will give us our summer rally, but not today.

The weekly view from the Economic Cycle Research Institute (shown next page) remains inconclusive. While it dipped last week, the overall trend is still positive and not indicating anything dramatic one way or the other.

Finally, the markets went up some six months in a row. The action in June was bound to happen, but is not occurring over some radical change in outlook which has not been good all along. Thus don’t get confused by headlines from the many happy talkers of months ago suddenly expressing concern. The items in the news this week have been present throughout the rally of the past four years.

Out next update will be in two weeks given the slowing activity as we head into the July 4th holiday. The employment report for June will come out on the 5th of July and represents the next big thing. This week’s news will simply reflect the macro items discussed above.

![]()

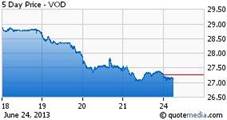

SYMBOL: VOD

Vodafone shares were flat t his morning as the Company announced a deal to buy the German cable operator Kabel Deutschland for 7.7 Billion euros. Vodafone has been in these discussions for many months.

The Company will add these new cable customers to its cellphone and broadband businesses. The so-called bundle will come to Germany. The deal is not a surprise and neither is the price being paid.

What has yet to be worked out is whether or not this will impact or affect Vodafone’s 45% stake in Verizon Wireless, worth some $120 billion dollars. We shall see but not for awhile as the acquisition will take several months to close, and that assumes no other bidders emerge for the shares.

![]()

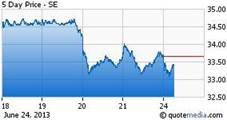

SYMBOL: SE

This is a follow-up note on shares of Spectra Energy which jumped higher, as we mentioned last Monday. It also turns out that an activist fund manager has communicated with the Board of the Company about strategy and steps which, if taken, could produce a much higher share price. This pressure may explain the timing of the actions announced two weeks ago, and may also raise the chances that further steps will be announced.

The hedge fund has indicated that it will pursue a proxy contest if their demands are not met, and estimated that shares in Spectra Energy were worth well into the high 40’s. Thus management has an obligation to consider the plan put to them. We shall see how it unfolds.

© McIntyre, Freedman & Flynn