Bond Investing Now Requires Assessing and Balancing Risk Exposure – Not Just Return Potential

Unprecedented monetary measures taken by central banks have pushed bond yields to record lows across the globe. The two factors that drive bond returns – capital appreciation and interest income – are both under pressure. The capital appreciation that results from declining interest rates is limited given that rates are already low and bound by zero. Furthermore, interest income is paltry, sometimes less than the inflation rate, because demand for bonds continues at a fever pitch. Add to this the looming threat of rising interest rates, and bond investors face a difficult crossroad.

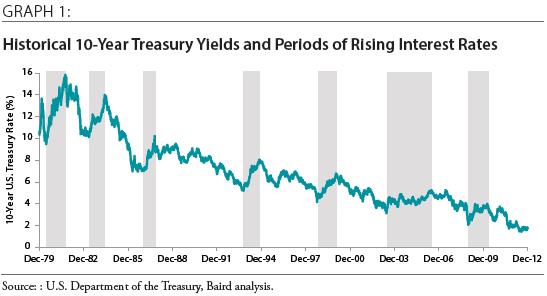

As depicted in Graph 1 below, the bond market has been in a 30-year bull market over which time it delivered investors a strong 8.6% annualized return (as measured by the Barclays Aggregate Bond Index). The 10-year Treasury yield that topped 15% in the early 1980s now offers around a 2% yield in 2013. With yields this low, the bond market returns of the past are no longer feasible, and volatility is likely to increase if interest rates rise.

Attempting to forecast when and to what extent interest rates rise is a tricky proposition. Rates can stay low for prolonged periods or spike up quickly. That said, it is not too early to begin to adjust your bond portfolio to better face these challenges. Luckily, the bond market is diverse and offers many options, which are highlighted in this paper.

Why Interest Rates Matter

From an issuer’s perspective, a bond is simply a loan that will be repaid down the road (i.e., at maturity) along with periodic coupon payments. This is a common form of financing for governments and corporations alike.

So much focus is on interest rates because it affects the prevailing price of a bond. If the current interest rate is greater than the coupon payment of a bond, its market price is lowered. It is worth less to a potential buyer because a new bond offers a higher coupon payment than the existing one.

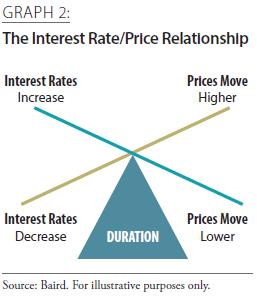

Thus, the direction of interest rates and bond prices are inversely related – when one increases, the other decreases (Graph 2). This relationship is magnified by a bond’s duration, or sensitivity to interest rate changes.

The prospect of rising interest rates is concerning to many investors because the value of bond portfolios will generally fall. However, the ability to reinvest coupon payments at now higher rates can at least partially offset those price declines. It is therefore important to focus on total return: price plus income changes.

It is unknown whether an environment of rising interest rates will result in negative total return for bonds or just muted returns. Every economic cycle is different and drawing broad conclusions based on past data is dangerous. A transparent Federal Reserve that aspires to calm the markets is a positive; the historically low yields that provide little buffer to price declines is a clear negative.

Nevertheless, an investor’s ability to navigate these ever-changing waters depends on their portfolio’s careful construction.

Bonds Still Play an Important Role

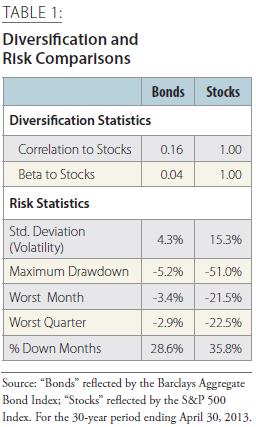

Omitting any major asset class such as bonds from a properly diversified portfolio can have unintended negative consequences. We believe that bonds still play a critical role in clients’ portfolios for the reasons stated below and quantified in Table 1.

• First, bonds have historically offered better downside protection and lower volatility than stocks have historically offered. A bond’s face value paid at maturity sets a terminal value that doesn’t exist with stocks. Unless there is a default, a bond can be held to maturity and the investor knows how much money to expect.

• Second, bonds have exhibited consistently low correlation to stocks over the past 30 years. Even if the expected total return of the bond market is not attractive, there is still value in owning bonds in terms of diversification potential. Properly balancing a portfolio’s stock/bond mix is the central determinant that impacts overall volatility.

• Third, bonds provide a stable stream of income. Many income-producing alternatives to bonds exist but few offer the same downside and diversification benefits. For example, many dividend-paying stocks offer competitive yields in addition to growth potential but are accompanied by much greater swings in price.

Bottom line, bonds are generally a suitable investment for most investors over most time periods. The decision that needs to be made isn’t whether to include or exclude bonds from a portfolio, it is how much to allocate and how to position that allocation.

The Portfolio Construction Dilemma

One effective way to reduce the impact of rising interest rates on your bond portfolio is to materially shorten the duration. However, as anyone with money in a savings account knows, short-term instruments pay next to nothing in yield. In fact, inflation-adjusted returns for many short-term instruments are negative.

Recall that capital appreciation is constrained because rates cannot fall much further. This means that the burden for total return falls on the interest payments (or yield). Higher yields are then necessary to maintain a positive inflation-adjusted return potential. Yet, yield is offered as compensation for assuming additional credit or interest rate risks; therefore, investors are increasingly being swayed towards less-traditional bond types.

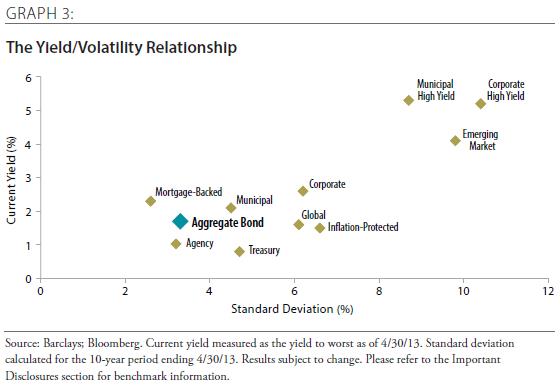

Graph 3 illustrates the relationship between yield and standard deviation (a measure of the volatility of returns). As of April 30, the Barclays U.S. Aggregate Bond Index has a current yield of 1.7% with a 3.3% standard deviation of returns. If someone wanted to achieve the 10-year historical average yield of 4% in this low yield environment they would have to consider Emerging Market Debt (4.1% yield), which carries three times the volatility!

Herein lies the major dilemma facing clients right now: the future of bond investing requires assessing and balancing risk exposures, not return potentials. The 30-year interest rate tailwind will no longer be at your back. If you are unwilling to accept higher risk than you have in the past, then return expectations need to be revised downward. This is the tough, but honest, truth of the environment that we face today.

Opportunities Still Exist

Opportunities still exist for those willing to take a proactive approach to addressing their bond portfolio.

Unlike the global stock market where correlations have risen to the point that most major categories move in close tandem with one another, bond markets are more segmented and react differently to various factors. This means that there are more levers that a bond manager can pull to adapt to changing conditions.

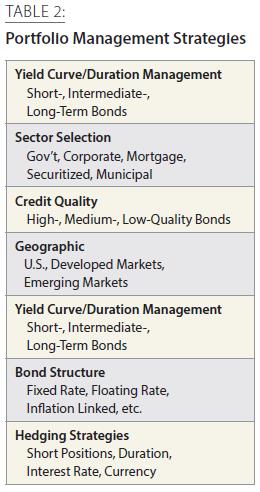

Table 2 lists a number of strategies or decisions that can be implemented in a bond portfolio. Each is subject to its own set of opportunities and risks. Yield curve management, duration control, sector selection and security research are among a few tools that professional money managers can use.

Oftentimes investors are more attuned to how their stocks are positioned and behaving, and take the bonds for granted given strong historical returns and lack of volatility. Going forward, we believe there is a growing need to develop a long-term strategy for your bond allocation. This may require repositioning a portion of your portfolio and will definitely require a reframing of expectations. One thing seems certain: The bond market of the next 30 years will face more challenges than the last 30 years.

Parting Words

• Don’t assume yield is free. In this environment of historically low yields, many bonds may appear less risky on a yield spread measure when compared to a long-term average. However, the thirst for yield has pushed bond prices higher, creating the appearance of a smaller risk premium than is often warranted. With higher yields generally comes higher risk; gain sufficient understanding of the risks in certain bond types before investing.

• Do consult a professional. Although it is unlikely for anyone to be right 100% of the time, professional money managers follow the markets daily and have the critical experience that can make them better equipped to manage risk and properly diversify a bond portfolio. Please consult your Financial Advisor for perspectives on how your bond portfolio is positioned given your return expectations and risk tolerance.

• Don’t overreact or attempt to time the market. Studies of behavioral finance have shown that many investors who follow their emotions tend to sell out of investments near a bottom, or buy into them after they’ve already hit a top. Short-term market corrections are likely and probable over long time periods. Maintain a long-term view and be mindful of the portfolio objectives before making changes.

• Do exercise patience and prudence. Investment time horizons can span years, or even decades. Keeping this in mind and following careful processes with regular evaluation is instrumental in achieving long-term objectives.

Aaron Reynolds, CFA, CFP®, is the Associate Director of Asset Manager Research at Baird. Reynolds is a co-portfolio manager of Baird’s ALIGN Strategic and UMA portfolios. He also oversees the due diligence of mutual funds and separate accounts, and frequently writes about topical market subjects. He has a BA in Economics from the University of Wisconsin-Madison and an MBA from the University of Chicago Booth School of Business.

If you have questions or need more information, please contact your Financial Advisor.

Important Disclosure

Indices are unmanaged and are used to measure and report performance of various sectors of the market. Past performance is not a guarantee of future results and diversification does not ensure a profit or protect against loss. Direct investment in indices is not available.

Benchmark Definitions

Barclays Aggregate Bond Index (“Aggregate Bond”): Comprised of approximately 6,000 publicly traded bonds, including U.S. Government, mortgage-backed, corporate, and Yankee bonds with an average maturity of approximately 10 years.

Barclays Muni Bond Index (“Municipal”): Bonds must have a minimum credit rating of at least Baa, an outstanding par value of at least $3 million, part of a transaction of at least $50 million, issued after December 31, 1990 and have a year or longer remaining maturity.

Barclays Muni High Yield Bond Index (“Municipal High Yield”): A subset of the Barclays Muni Bond Index that have a credit rating of less than Baa, an outstanding par value of at least $3 million, part of a transaction of at least $50 million, issued after December 31, 1990 and have a year or longer remaining maturity.

Barclays U.S. Treasury Index (“Treasury”): Public obligations of the U.S. Treasury with a remaining maturity of one year or more.

Barclays Agency Bond Index (“Agencies”): A sub-set of the Aggregate Bond Index that includes U.S. agency issued bonds, including the Federal National Mortgage Association (Fannie Mae).

Barclays U.S. Credit Index (“Corporate”): Includes publicly issued U.S. corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered.

Barclays MBS Index (“Mortgage-Backed”): U.S. agency mortgage-backed bonds, including Government National Mortgage Association (GNMA), Federal National Mortgage Association (FNMA) and Freddie Mac (FHLMC) securities.

Barclays U.S. Corporate High Yield (“Corporate High Yield”): Covers the universe of fixed rate, non-investment grade debt. Eurobonds and debt issues from countries designated as emerging markets (sovereign rating of Baa1/BBB+/BBB+ and below using the middle of Moody’s, S&P, and Fitch) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-EMG countries are included. Original issue zeroes, step-up coupon structures, 144-As and pay-in-kind bonds (PIKs, as of October 1, 2009) are also included.

Barclays Global Aggregate (“Global”): Provides a broad-based measure of the global investment-grade fixed income markets. The three major components of this index are the U.S. Aggregate, the Pan-European Aggregate, and the Asian-Pacific Aggregate Indices. The index also includes Eurodollar and Euro-Yen corporate bonds, Canadian government, agency and corporate securities, and USD investment grade 144A securities.

Barclays EM USD Aggregate (“Emerging Markets”): Includes USD denominated debt from sovereign, quasi-sovereign, and corporate EM issuers. Country eligibility and classification as an Emerging Market is rules-based and reviewed on an annual basis using World Bank income group and International Monetary Fund (IMF) country classifications.

Barclays US Gov’t Inflation Linked (“Inflation Linked”): Measures the performance of the US Treasury Inflation Protected Securities (“TIPS”) market. The index includes TIPS with one or more years remaining maturity with total outstanding issue size of $500m or more.

Market Risk: The risk that the bond market as a whole would decline, bringing the value of individual securities down with it regardless of their fundamental characteristics.

Costs and Fees: The risk that the costs and fees associated with an investment are excessive and detract too much from an investor’s return.

Liquidity Risk: The risk that investors may have difficulty finding a buyer when they want to sell and may be forced to sell at a significant discount to market value.

Credit Risk: The risk that the borrower will be unable to make interest or principal payments when they are due and therefore default.

Beta: A measure of a portfolio’s sensitivity to the performance of its benchmark. A beta greater than 1 suggests higher volatility and vice versa.

Standard Deviation: A statistical measure of performance dispersion. The higher the measure, the more volatile the historical return pattern.

Maximum Drawdown: Over a specific period, the greatest peak to trough decline.

Correlation: A statistical measure of how securities move in relation to each other.

MC-38674. First use: 5/13

© 2013 Robert W. Baird & Co. Incorporated. rwbaird.com 800-RW-BAIRD