Despite Interest Rate Concerns, Muni Volatility May Offer an Entry Point

As we approach the midway point of 2013, the capital markets have many concerns: the potential end of quantitative easing (QE3), the slow rate of economic growth, the stubbornly high unemployment rate and the sorry state of affairs in both federal and state government finances. I won’t speculate on the eventual outcome of these issues, especially where politics is concerned. But I do think it’s valuable to look past the market’s fear and search for areas where smart investors can take clear-eyed action and benefit in uncertain conditions.

Based on what we’re seeing in the closed-end fund market, municipal bonds may be an area to consider. Steep discounts could present buying opportunities for investors whose risk tolerance and time horizon can withstand the present market volatility and economic questions.

What goes down, must come up … but when?

One of the top areas of uncertainty is the future of interest rates and the potential for them to rise once QE3 eventually ends. The United States has seen, on balance, a downward trend in rates and a very positive environment for fixed income investors since the second half of 1981. However, even if rates go no lower beyond 2013, it does not necessarily follow that they will rise substantially higher anytime soon. When interest rates rise, if interest rates rise, how fast they rise, and how high they go — none of this is predictable with certainty.

Depending on a number of factors, a good case can be made that if rates do track higher, it may happen in a slow, methodical method, giving investors multiple entry points along the way. If short-term rates remain near zero, as they have for several years, there may be a substantial opportunity cost for investors who wait on the sidelines versus investing today. Investors who make prudent choices with today’s rates get a head start on their income accumulation.

What we can learn from municipal closed-end funds

The unique nature of closed-end funds makes them a reflection of investor sentiment. The net asset value (NAV) performance on a closed-end fund reflects the price movement of the fund’s underlying investments. But the market-price performance of closed-end funds reflects supply/demand factors for the individual shares traded on the exchanges, which is evidenced by whether the shares trade at premiums or discounts to NAV.

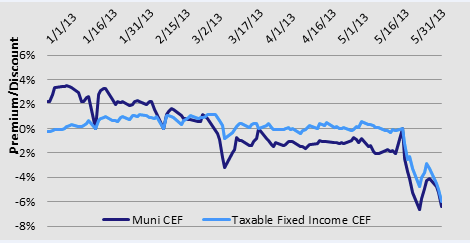

Recently, closed-end funds that invest in municipal bonds have experienced notable volatility as their market price performance has fallen significantly below their NAV performance. The chart below illustrates the premium/discount levels on closed-end muni funds versus closed-end taxable funds from Jan. 1, 2013 to June 12, 2013. The muni funds began 2013 at roughly a 2% premium to their NAVs, while the taxable funds were around par value. Munis had a very sharp selloff in March, creating discounts around 3%, while the taxable funds held near par. Munis recovered nicely to par in early April into May, but have had a sharp selloff from mid-May through mid-June, creating discounts to NAV of approximately 6%. The taxable funds have sold off sharply during the last several weeks, creating their largest discounts of the year.

Source: Bloomberg; as of June 12, 2013

What’s behind the strong volatility in closed-end muni funds?

It may be an overreaction to the overall bond market correction, which was fueled by macro concerns and exacerbated by selling pressure — in the week ended June 5, fixed income investors liquidated over $9 billion in assets from bond mutual funds and exchange-traded funds, which is second-biggest redemption week since 1992, according to Lipper.

In some cases, muni closed-end funds are trading at prices and discounts not seen since mid-2011, whereas just a few months ago, they were trading at premiums to their NAVs. This may present a more attractive entry point to consider; bigger discounts and higher current interest rates are a byproduct of lower market prices.

Conclusion

There is much speculation in the marketplace regarding the economy, interest rates, and the Federal Reserve’s next move, among other factors. This speculation has manifested itself in weaker bond prices overall, and much weaker prices among closed-end funds as their market prices have fallen below their NAVs. Investors and their financial advisors may wish to weigh these factors and decide if this an attractive entry point, or is there further weakness to be expected? Fixed income instruments will continue to play an important part of well-diversified portfolios, and many times the decision to take advantage of market opportunities created by above-average selling pressure look good down the road as the markets recover.

Important information

All fixed-income securities are subject to two types of risk: credit risk and interest rate risk. Credit risk refers to the possibility that the issuer of a security will be unable to make interest payments and/or repay the principal on its debt. Interest rate risk refers to fluctuations in the value of a fixed-income security resulting from changes in the general level of interest rates.

Economic and regulatory factors may affect a municipal security’s value, interest payments, repayment of principal. An issuer’s failure to comply with tax requirements may make income paid thereon taxable, thus reducing the security’s value. In addition, there could be changes in applicable tax laws or tax treatments that reduce or eliminate the current federal income tax exemption on municipal securities or otherwise adversely affect the current federal or state tax status of municipal securities.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

Invesco Distributors, Inc.

© Invesco