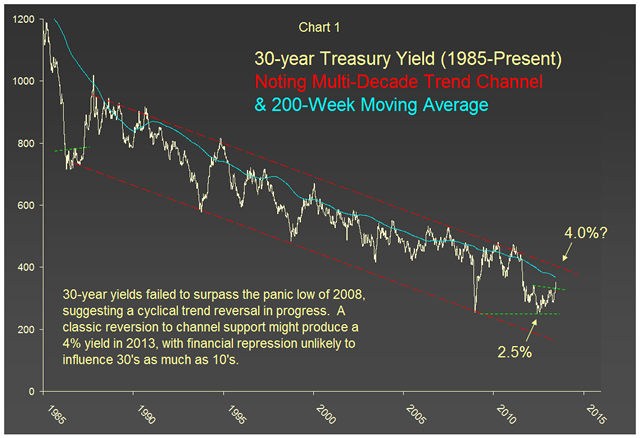

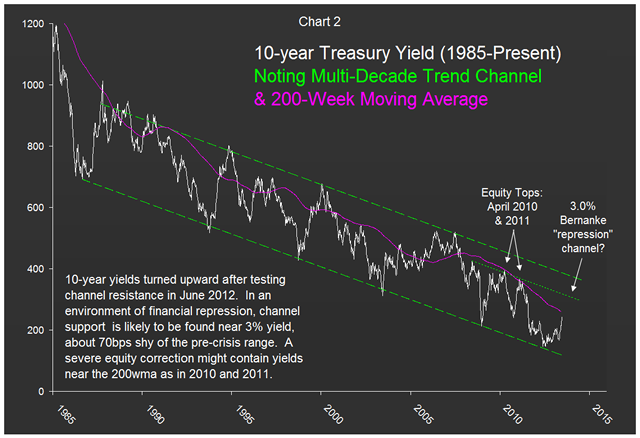

The evolving bond-market reversion, which I have explored here and here, is on track to produce yields of 4.0% on 30-year Treasury bonds and 3.0% on 10-year Treasury notes. (See charts 1 & 2 below.) This would constitute a normal process which has occurred time after time in recent decades, even in the post-ZIRP environment.

So, what could go wrong with the full-cyclical-reversion scenario? Lots of things, of course. In particular, a severe equity-market correction might limit the yield on 10-year notes to the vicinity of the 200-week moving average as noted in Chart 2. This caveat is worth mentioning as we approach the 200-week average in an environment of equity weakness.

© Charter Trust Company