Asia Brief: China's Energy Demand

China has the world’s largest unconventional gas reserves, but these so far remain untapped despite its growing demand for energy. China is now trying to follow the example of the US, and the government has set aggressive targets for unconventional gas production. As the demand for transportation fuels grow over the next decade, this gas could be a major contributor to meeting that need. However, there are major technical and institutional challenges to be overcome before these targets can be met, and China lacks the dynamic private companies which were instrumental in innovating to grow production in the US.

China’s voracious demand for energy has driven its hydrocarbon majors to search the globe for suitable assets to satisfy the needs of its growing industrial economy. However, some of the most prospective sites may be at home in China. As the US has discovered, the techniques of fracking and horizontal drilling can substantially increase the available supply of natural gas, and the Chinese authorities are watching and learning from the US experience.

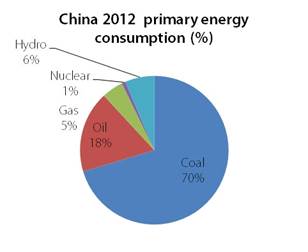

As it stands, natural gas is not a major part of the Chinese energy mix (see figure 1), accounting for 4.7% of its primary energy consumption in 2012. This places it slightly below hydropower, which accounts for 6.4%. Coal is by far the biggest energy contributor for China, accounting for 70% of its needs.

Figure 1: China’s energy consumption

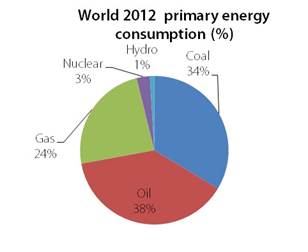

This makes China unusual compared to other nations in the world, which tend to have a much better balanced consumption pattern with a greater emphasis on oil and gas (see figure 2). This is partly a function of availability, given China has large onshore coal reserves and a suitable landscape for hydro power, particularly in the South of the country. It also reflects the fact that stationary power and industrial users have driven the demand for energy over the last 20 years.

Figure 2: World energy consumption

China cannot rely on coal and hydro power alone to fuel its growth, and fresh demand for transportation, as opposed to electricity production, is likely to take up more of China’s growth of energy usage in the coming decade. This lends itself more readily to oil and gas.

China’s world-class unconventional gas reserves

China has globally significant proven reserves of technically recoverable unconventional gas in the form of both coal bed methane and shale gas (1115 trillion cubic feet (tcf)), according to the US Energy Information Administration (EIA) and the Chinese Ministry of Land and Resources. This means China is estimated to possess the largest unconventional gas reserves in the world. By way of comparison, the EIA estimates that the US has 567 tcf of technically recoverable resources of shale gas. The gas reserves are also much bigger than China’s conventional gas reserves which are estimated at only 124 tcf.

The reserves are in basins across the country but the most interesting are in the West and center of the country. The Tarim basin in the far west and the central Sichuan basin are of most interest for shale gas, while the central Qinshui and Ordos basins are most prospective for coal bed methane.

China’s challenge is to extract and use these endowments in an economical and responsible way, and the government is still grappling with the best way to do so. From an environmental point of view, unconventional gas can be of benefit by reducing carbon and particulate emissions at the point of use, and this can help China reduce further environmental damage.

Government targets for natural gas

The government recognizes the huge potential of unconventional gas and has ambitious targets for production in the two five year plans running from now until 2020. If the government’s targets are met, China will produce between 8 and 12 billion cubic feet (bcf) of shale gas per day by 2020, which is similar to the country’s current conventional gas production and would put it close to the shale gas production in the US today. For coal bed methane, the targets are similarly ambitious, and production should be just under 2 bcf per day by 2020.

To attain these levels, the government has concluded two rounds of bidding for shale gas blocks, and awarded licenses to major domestic players based on their willingness to invest the money to drill the wells needed to explore these areas. There should also be another round of bidding over the next 12 months, and this could include foreign companies. Coal bed methane exploration is being carried out in a slightly different manner, with around 70% of the existing reserves already carved up between two players, Petrochina and China United Coal Bed Methane.

Encouraging gas consumption

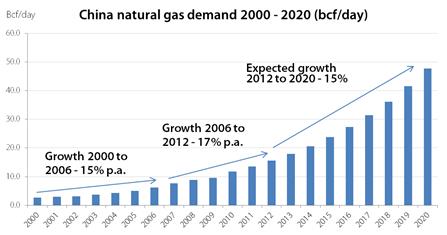

As well as allotting the blocks and encouraging firms to drill, the government also needs to address the demand side for gas and take steps to support higher prices to allow the needed investment to take place. Figure 3 and table 1 indicate reasonable forecasts of growth in demand for gas in China, but this also reflects other sources than unconventional gas production.

This puts China at an advantage compared to its regional peers, all of whom went through a similar process as China when their investment-led growth phases cooled and consumption became more significant as a driver of Gross Domestic Product (GDP) growth. Unlike Japan, South Korea and Taiwan (see chart below), Chinese oil demand relative to primary energy consumption has barely crept above 20%, while these other nations peaked at 70-80% before falling back to around 50% following the end of their investment phases of growth. For Japan, South Korea and Taiwan, with few energy resources of their own, imported oil was the quickest and easiest method of ramping up energy consumption domestically, but it left them exposed to imported inflation if international oil prices rose. With large coal deposits of its own, China has been in an advantageous position, and this could allow it to rapidly expand vehicle usage without a debilitating effect on its balance of payments status and inflation.

Considering table 1, the Chinese government recognizes that its energy usage has become unbalanced, with too great a reliance on coal as a source of fuel. The consequences of heavy coal usage are becoming apparent across industrial China, with emissions causing real concern in the larger cities. It is also difficult for China to shift too much of the burden to oil, given around half of the nation’s oil is imported and this exposes China to the vagaries of international prices. It is also difficult to scale up hydro power to meet a big growth in power needs, and it may even fall as a proportion of overall energy supply by 2020. Gas offers a cleaner-burning fuel which can be scaled up to meet China’s needs for both transportation and power generation. Given this, onshore unconventional gas is ripe for development to meet the nation’s needs.

Figure 3: China natural gas demand

Source: Guinness Atkinson, Bloomberg

On the import side, Liquid Natural Gas (LNG) is already being imported from the Middle East and Australia, and more could be brought across the Pacific from the US and Canada to help meet China’s needs. Given the uncertain state of the gas industry in the US, many producers would be glad to capture the new demand growth and higher prices available in Asia. However, volume exports from North America require political support, and it may be unpalatable to allow this windfall to help drive the economic development of a national rival.

The other main source of growth in gas supply is a network of gas pipelines bringing gas from the existing fields of central Asia to China. This will bring gas from Turkmenistan, Uzbekistan, Russia and Kazakhstan to China, and the core section of the pipeline has been in operation since 2009. It is estimated that 0.87 bcf of gas a day flowed through the pipeline in 2012, and the China National Petroleum Corporation, which operates the project, estimates that this could reach 5.8 bcf per day in future. There is also the possibility that other nations, such as Kyrgyzstan, could be added to the supply network by a new branch of the pipeline.

Table 1: China: Share of primary energy consumption

![]()

China: share of primary energy consumption (%)

June 2013

|

2000 |

2004 |

2008 |

2012 |

2016 |

2020 |

|

|

Coal |

69.0% |

68.8% |

70.1% |

70.4% |

69.9% |

67.8% |

|

Oil |

23.2% |

22.3% |

18.9% |

17.7% |

16.5% |

15.7% |

|

Gas |

2.3% |

2.5% |

3.6% |

4.7% |

6.5% |

9.3% |

|

Nuclear |

0.4% |

0.8% |

0.7% |

0.8% |

1.1% |

1.6% |

|

Hydro |

5.2% |

5.6% |

6.6% |

6.4% |

5.9% |

5.6% |

|

Total |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

100.0% |

Source: Guinness Atkinson, Bloomberg

Gas price reform

Even if the gas is physically available, there remains a pricing issue under the current mechanism, and this may well not be enough for firms to make a reasonable return for their efforts. At present, gas and oil prices are closely managed by the government, and as with the oil refiners, the government has demonstrated that it is happy for state-owned enterprises to make losses in order that retail and industrial prices for energy are kept under control. City gate gas prices are set by the National Development and Reform Commission (NDRC), but the aim of reform is to eventually allow well-head prices for domestic production to float based on market conditions. In 2011, the NDRC launched a pilot scheme whereby wholesale prices for unconventional gas were liberalized and aimed to link overall domestic natural gas prices more closely to the price of the imported fuel. Under the pilot, gas prices in Guangdong and Guangxi provinces were set based on a 10% discount to a weighted average of imported fuel oil and Liquid Petroleum Gas (LPG) prices. However, the liberalization has not been extended nationwide, and prices paid by the pipeline companies, town gas firms and bulk users remain, set quarterly based on current production costs plus a spread.

In addition to liberalizing gas pricing, China also needs to encourage the greater use of gas in transportation. While power generation or industrial users may plan over the long-term and can decide between one fuel and another, transportation users may not have the luxury of planning in the same way. In October 2012, the NDRC announced plans to encourage the use of both liquefied natural gas (LNG) and compressed natural gas (CNG) in transportation, with buses, taxis, lorries and ships all highlighted as preferred users. These fleet-type users are likely to be early adopters of gas for transportation, although individual vehicle users may follow later. Take up is high in some cities, with 85% of taxis and 92% of buses in Chongqing using LNG engines and around 50% of taxis nationally having adopted gas engines. There are around 1 million natural gas-powered vehicles on the roads in China, and the government targets a total of 3 million units by 2020. But this is still a drop in the ocean compared to the total of 15.49 million vehicles sold in China in 2012 alone.

The risks to China’s gassy future

Despite the current optimism about unconventional gas it is not easy to look at the rapid progress made in the US and extrapolate this to China. China presents a number of challenges, both physical and economic, which are likely to mean that China will struggle to achieve the same explosive growth in production as has been witnessed in the US.

Perhaps the outstanding challenge presented by China for hydrocarbon extraction is the difficulty of the natural environment in the most prospective basins. The Tarim basin is in the far west of China and is in an area that is effectively a desert. This makes it difficult and expensive to source the water needed for hydro-fracking. The Sichuan basin is in the South of the country in a relatively well populated area with undulating terrain, meaning that support structures such as bridges may also need to be constructed to support extraction. There is also a potential danger from seismic activity in the Sichuan basin, given this is a geologically active area, and there have been indications of an association between fracking and seismic activity elsewhere in the world.

If the geographic hurdles can be overcome, then the technical hurdles still present a challenge. The skills needed to successfully frack are difficult to master, and the international and US firms which possess them have tended to lose out to domestic Chinese firms on exploration and production work in China. This is beginning to change, with some investments by services majors into smaller Chinese services companies, such as Schlumberger’s investment in Hong Kong–listed Anton Oilfield Services. However, the majority of the work is still carried out by the services divisions of state-owned enterprises, which do not have a reputation for innovation.

The development of unconventional gas in the US was primarily led by private companies, and many of these were small exploration and production companies of a type that are thin on the ground in China. The Chinese hydrocarbon industries are dominated by state-owned enterprises and, in particular, the ‘big three’ of Petrochina, Sinopec and CNOOC. Given the structure of the economy in China, it is hard for smaller, private firms to make their mark, and it is particularly hard against the huge majors. The state-owned enterprises have the best access to capital and seem to have preferential treatment when it comes to licensing, creating an uneven playing field for the smaller firms to compete.

For these giant firms, unconventional gas is likely to be a small part of their overall earnings in the next three years. These firms have so far shown interest in unconventional gas but have not backed this interest with the investment needed to meet the government’s aggressive targets for production growth. For instance, the amount of capital spending on unconventional gas in 2012 in the US was $32bn, which matches the entire upstream capital spending in China in that year. It is difficult for smaller firms to get access to the capital they need to make up the shortfall, and the gas pricing mechanism is such that even if they could, the incentive may not be there for them.

The current industry structure also means that the smaller energy services players are focused on supporting the larger players and driven primarily by their investment plans. In recent years, this has meant supporting the ‘big three’ in their international investments, with domestic exploration and production being relatively less important.

As well as spending on the production side, there needs to be greater investment on the infrastructure for gas transmission, distribution and retail. This implies new pipelines to take the gas from the new fields to customers and also the delivery mechanisms by which gas can be supplied to its end users. For industrial customers this can be relatively simple, but for transport applications, such as fleet vehicles and cars, this requires a network of local fueling stations across the country. The 12th five year plan running to 2015 envisages the network of refilling stations to double to around 2000 stations.

China’s unconventional challenge

Although China has significant reserves of unconventional gas and the government has set aggressive targets for development, it is far from certain that these targets can be met. Certainly, the explosive growth in production that has been witnessed in the US may be impossible for now, given the physical and industrial constraints which exist. Addressing these will take a great deal of effort and investment from the government, and a significant part of the solution is likely to come from the smaller, more nimble, service providers and exploration and production companies which are currently disadvantaged in China. Meaningful gas price reform to allow prices to float would be helpful but is unlikely in the context of tight restrictions on a range of prices in China.

Ultimately, the large state-owned enterprises have the capital and licenses to carry out the development of unconventional gas, but they must be incentivized, or forced, to do so if the government is serious about meeting its own targets.

Market Review

Market Performance Ending May 31st, 2013

|

May 2013 |

Year to date |

2012 |

2011 |

2010 |

2009 |

|

|

Australia |

-11.89% |

0.48% |

22.25% |

-10.77% |

14.69% |

73.87% |

|

China |

-0.86% |

-4.29% |

22.69% |

-18.36% |

4.59% |

62.06% |

|

Hong Kong |

-1.70% |

4.41% |

28.26% |

-15.78% |

23.28% |

60.48% |

|

Indonesia |

-3.86% |

11.29% |

6.11% |

5.19% |

35.47% |

136.12% |

|

Korea |

0.43% |

-6.31% |

20.99% |

-13.55% |

25.84% |

74.44% |

|

Malaysia |

3.19% |

7.03% |

14.54% |

0.11% |

37.67% |

51.26% |

|

New Zealand |

-13.01% |

2.68% |

31.54% |

5.90% |

8.73% |

49.89% |

|

Philippines |

-3.09% |

18.36% |

47.52% |

0.04% |

35.24% |

67.34% |

|

Singapore |

-4.88% |

1.28% |

30.98% |

-17.54% |

22.03% |

73.18% |

|

Taiwan |

-0.23% |

3.74% |

17.43% |

-20.18% |

23.14% |

80.23% |

|

Thailand |

-7.26% |

5.70% |

35.01% |

-2.72% |

56.67% |

76.59% |

|

MSCI AC Far East Free ex Japan |

-1.09% |

0.04% |

22.06% |

-14.75% |

19.41% |

68.56% |

|

MSCI AC Pacific ex Japan * |

-4.25% |

0.39% |

22.72% |

-13.59% |

17.95% |

71.51% |

*MSCI AC Pacific includes Australia & New Zealand

(MSCI Indices were used for regional & individual market performance)

May was a mixed month for global equities, with the possibility of a reduction in the asset purchase program by the US Federal Reserve causing some investor disquiet. Asian equities also performed poorly with a sell-off in Japanese assets creating a negative background for the region. Last month currency moves between local currencies and the US Dollar also drove meaningful return differences between the Asian equity markets.

The worst-performing countries in May were Australia and New Zealand, which both fell sharply in US dollar terms. Both Australia and New Zealand performed reasonably well in local currency terms, but it was a fall in value in their currencies relative to the US dollar which did much of the damage. The MSCI Australia was down 4.80% in May in local currency terms, but it was off 11.89% in US dollar terms. The rationale for the difference is that international investors seem concerned about Australia’s exposure to North Asia through its mining and resources industry in the face of mixed demand for its products.

Thailand also underperformed the wider region in May, finishing down 7.26% in US Dollar terms. In local currency terms, the MSCI Thailand was only down 3.71%. Economic growth seems to be slowing slightly in Thailand, and the central bank cut interest rates by 0.25% to 2.50% owing to what it described as ‘tepid domestic demand’ and the potential for delay to the government’s infrastructure investment plans. From the bottom up, however, property pre-sales remained buoyant, although the central bank did describe the ‘growth of private credit and household debts’ as ‘elevated’.

On a positive note, Malaysia’s stock index enjoyed a bounce following victory for incumbent Najib Razak in the recent general election. The 3.19% rally reflects market relief in favor of the status quo and represents some affirmation of Najib’s Economic Transformation Programme (ETP), the centerpieces of which are infrastructure spending and administrative reform. However, there may be some volatility to come as some results are disputed by the opposition, and there could be a leadership election within Najib’s party, United Malays National Organisation (UNMO), given the incumbent coalition won less than 47% of the popular vote.

Major Indices total returns for the five years ending May 31, 2013

China Economic Monitor

Chinese headline growth remained on course to meet the government’s target of 7-8% for the medium term, but a number of the individual economic indicators suggest that growth may be slowing again in the world’s second-largest economy. Monetary stimulus drove a brief respite from the slowdown during the final quarter of 2012 and the first quarter of 2013, but it now seems that this momentum may not have endured.

The new Chinese Premier, Li Keqiang, is reported to closely follow three indicators: railway freight, electricity production and loan growth, and these are giving mixed signals as to the state of the economy. Railway freight growth has been contracting since the turn of the year, and it has now reached a level of contraction to match that seen during 1998 and 2009, albeit rail freight is at a much higher absolute level than during either of those years. Loan growth has also started to slow but remains respectable relative to GDP at 14.5% year over year. Electricity production growth is also respectable at 5.3% year over year in May.

Source: National Bureau of Statistics, Bloomberg

Loan and deposit growth have continued their trends of recent months, with an acceleration in deposit growth again in May and another contraction of loan growth. Deposit growth was 16.2% year on year in May, slightly ahead of 14.5% loan growth. This suggests that Chinese banks are continuing to rebuild the liability side of the balance sheet and that the impact of monetary stimulus in 2011-2 is fading. This is of some concern, as it appears that the stimulus has not succeeded in creating a lasting re-acceleration of economic growth. However there are some grounds for optimism in the figures for non-bank lending – commonly known as ‘shadow banking’. The growth on non-bank lending slowed in May, amounting to 40.9% of total new lending, compared to around half of all lending in the previous two months.

Inflation remains under control in China, and in May both the consumer price index (CPI) and the producer price index (PPI) contracted further. Although this fulfils the government’s goal of preventing rapid price rises, the lack of inflation may in fact reflect underlying slow growth rather than just the impact of policy. The continued deflation in the PPI is of some concern, with a contraction of 2.9% year on year in May. If this continues it can compress business margins and hurt corporate earnings growth. On the consumer price side, increases in food prices remain relatively benign with chicken, duck and pork prices down slightly year on year. Egg, rice, oil and flour prices are up year on year, but we believe these small increases are not of concern.

Vehicle sales in China were flat in May 2013 compared to the previous month at around 1.4 million units. However, for the first time in some months, the US overtook China, recording sales of 1.44 million units. This reflects the improving performance of the US economy and also the current slowdown in growth which looks to be underway in China. From the bottom-up, the makers of Japanese-branded cars in China have reported improving volumes, but this seems to be related to price cuts rather than a real improvement in demand. By contrast, consumer attention seems to be shifting to European brands, rather than to domestic brands.

Source: China Automotive Information Net, Bloomberg

Performance data quoted represents past performance and does not guarantee future results. Index performance is not illustrative of Guinness Atkinson fund performance and an investment cannot be made in an index. For Guinness Atkinson Fund performance, visitgafunds. com .

Mutual fund investing involves risk and loss of principal is possible. Investments in foreign securities involve greater volatility, political, economic and currency risks and differences in accounting methods. Non-diversified funds concentrate assets in fewer holdings than diversified funds. Therefore, non- diversified funds are more exposed to individual stock volatility than diversified funds. Investments in smaller companies involve additional risks such as limited liquidity and greater volatility. The Fund may invest in derivatives which involves risks different from, and in certain cases, greater than the risks presented by traditional investments.

Fund holdings and/or sector allocations are subject to change at any time and are not recommendations to buy or sell any security

The MSCI All Country Far East Free ex-Japan Index (MSCI AC Far East free ex-Japan Index) is a free float- adjusted, capitalization-weighted index that is designed to measure equity market performance in the Asia region excluding Japan. The Index is made up of the stock markets of China, Hong Kong, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand.

The MSCI All Country Pacific Free ex-Japan Index (MSCI AC Pacific Index) is a free float-adjusted, capitalization-weighted index that is designed to measure equity market performance in the Pacific region. The Index is made up of the stock markets of Australia, China, Hong Kong, Indonesia, Korea, Malaysia, New Zealand, Philippines, Singapore, Taiwan and Thailand.

The S&P 500 Index is a broad based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general.

The STOXX Europe 50 Index (STXE 50), Europe’s leading Blue-chip index, provides a representation of supersector leaders in Europe. The index covers 50 stocks from 18 European countries: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom.

The MSCI Australia Index is designed to reflect the performance of the domestic Australia equity market, excluding foreign companies listed on the Australia Stock Exchange.

The MSCI Thailand Index is designed to reflect the performance of the domestic Thailand equity market.

Consumer Price Index (CPI) is a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food and medical care.

Producer Price Index (PPI) is a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time.

Retail Price Index (RPI) is a measure of consumer inflation produced by the United Kingdom’s Office for National Statistics.

One cannot invest directly in an index.

Upstream is the exploration and production stage of the oil and gas industry.

This information is authorized for use when preceded or accompanied by a prospectus for the Guinness Atkinson Funds. The prospectus contains more complete information, including investment objectives, risks, fees and expenses related to an ongoing investment in the Funds. Please read the prospectus carefully before investing.

Opinions expressed are subject to change, are not guaranteed and should not be considered investment advice

Distributed by Quasar Distributors, LLC.

© Guinness Atkinson Asset Management