Stock prices came under pressure last week over the strength of the Japanese Yen versus the dollar which led to a large decline in stock prices there as well as the misplaced fears domestically that the Federal Reserve Board will pull forward its timetable for “tapering” its quantitative easing policy.

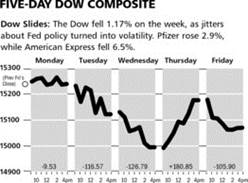

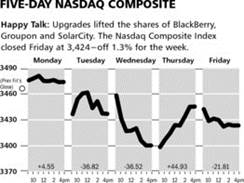

As the charts above illustrate, the Dow Jones Industrial Average declined by 1.2% while the NASDAQ Composite dropped by 1.3% over these concerns.

The Markets & Economy

The economic data last week continued to show a mixed picture. Initial jobless claims are encouraging as far as they go, but the creation of full time jobs is not sufficient to lower the unemployment rate or to increase personal income (part time workers to avoid Obamacare being the culprit at present). At the same time industrial production is no higher today than one year ago, along with capacity utilization. Accordingly, inflationary pressures are actually diminishing at present. This is something which is hardly indicative of strong demand either domestically or most certainly abroad.

In fact, commodities in general have been out of favor for much of this year, and the gold bugs must truly be getting frustrated with the decline being seen in precious metals. Only the occasional (actually all too frequent) episodes of financial confusion from Europe, such as we saw last week in Greece, are providing support for gold at this point.

But all of this is really beside the point on a day by day basis as the market moves are based upon not the news, but how the world’s Central Bankers are going to react to the news.

There is much to-do in the financial press about this week’s two-day meeting of the Fed. Last week saw concern that the Fed would signal the winds of a policy shift. To which I ask, based upon what? Their two mandates of low unemployment and controlled inflation are notcurrently being achieved.

Unemployment rose last month and I believe is headed for 8% by year-end. At the same time, the inflation measures the Fed closely monitors are similarly sending signs of excess capacity and disinflation at the very least.

Frankly, for the Fed to change policy now, under these circumstances, would be to admit the policy was not appropriate in the first place. That might be accurate, but the Fed would never admit to it either explicitly or tacitly. Thus investor concerns over such a development, I think, have been over estimated and should not continue to be the reason for a pullback in stock prices.

What to Expect This Week

The market is off to a very strong start this morning as the fears mentioned above somehow have disappeared over the weekend. The Fed will conduct its meetings and announce what its view is via a press conference on Wednesday. Clearly, the markets are now viewing this week’s Fed actions as a basic no change in policy.

This is most likely due to the fact that second quarter GDP estimates are still calling for sub 2% growth. While most economists expect the second half of the year to be better, I do not. For the past several years the second half has proven weaker, and with China, Japan and Europe slipping, I just don’t see where the growth is going to come from.

Of course, this year will also see the business community facing the full pressure of Obamacare which starts in January 2014. Confidence is not there today. As a result for the full year of 2013, when all is said and done, we will be lucky to see 2% growth.

Our weekly review of the leading indicators from the Economic Cycle Research Institute (see charts next page) show no change. They interpret that to mean a recession. I interpret their data to mean nothing is changing dramatically one way or the other.

Consequently, I believe the Fed will leave investors this week with the parameters for what would cause them to change policy, but at the same time the notion that we are far from that point today. This will also provide support to the financial markets.

SPECTRA ENERGY SYMBOL: SE

Shares in Spectra Energy, Symbol SEsoared last week when the Company announced plans to dramatically reshape itself via use of its captive Master Limited Partnership Spectra Energy Partners. SE will drop down all of its transmissionand storage assets to its subsidiary. This will result in higher rates of growth at SE, which will allow the Company to raise its dividend by twelve cents annually versus a previous target of eight cents.

To say that Wall Street loved this transaction is an understatement. Shares in SE jumped by 15% last week, which is pretty good for a pipeline utility company. Most price targets have moved upwards to the high thirties. This Company has always represented, along with Enterprise Products and Southwestern Energy, our way of participating in the long-term energy revolution taking place here in the United States.

The fundamentals are great, and while there may be pullbacks, a new faster growth period has begun for us in SE with this transaction.

![]()

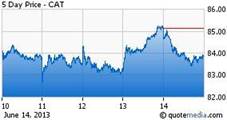

SYMBOL: CAT

Shares in Caterpillar, Symbol CAT, also showed relative strength last week when the Company increased its quarterly dividend to $.60 from $.52. Caterpillar has now grown its dividend at nearly a 9% growth rate over the past five yearsand currently yields almost 3%.

Shares in Caterpillar have been under pressure this year as a result of concerns over the global economy, especially in China. While this is disappointing in the near-term, this Company is the gold standard name to own when the global economy picks up, and the stock price is cheap on any kind of price-earnings basis.

Only a full blown and extended global recession could hurt the shares at this point. The increase in the dividend just lent more support to the share price, which would soar if the economy was actually doing what so many of the “happy talkers” want you to believe.

© McIntyre, Freedman & Flynn