FASTER THAN A SPEEDING BULLET

Do you remember hiding under the sheets listening to radio when your parents thought you were asleep? If so, I have an unbelievable collection of all the old-time radio shows we listened to when we were kids, if you have about six months’ spare time. Find your favorite, click on it, and it lists literally hundreds of episodes you can re-live. For example, check out comedy, mystery, drama, Westerns – including such greats as Superman, Flash Gordon, Suspense, Cisco Kid, Burns & Allan, Amos & Andy, and hundreds more. If you don’t remember but want to find out how great old radio could be, check it out at http://www.dumb.com/oldtimeradio/.

GROWING UP

Exchange Traded Funds (ETFs) are entering their third decade, having grown from $500 million in 1993 to $1.34 trillion in 2013. Pretty impressive.

CAVEAT EMPTOR

It seems like a day doesn’t go by without a story about conflicts of interest in the financial services world. An example was a recent New York Times article “Selling the Home Brand: A Look Inside an Elite JPMorgan Unit.” According to the story,

“Everything is scripted for the brokers in an elite group at JPMorgan Chase: the sales pitches; the personal voice mail message; even the preferred desk candy, Glitterati Fruit & Berry.

In a three-inch-thick training manual, the bank, the nation’s largest, details how to recruit clients, pitch products and, ultimately, close the deal — or, as JPMorgan puts it, “get to Yes!”

And, according to former JPMorgan brokers, the firm adheres to the popular Wall Street version of the “open platform”; i.e., we do not restrict our investments to only our proprietary products. We search the world for the best; it just so happens that in most cases that’s us! As one broker [Mr. Burris] explained it,

“The bank, Mr. Burris’s bosses explained, examines the amount of JPMorgan-branded portfolios of mutual funds that brokers sell. ‘If you look at our firm, 50 percent of all our sales go’ to those investments, Mr. Haigis [one of Mr. Burris’ managers] said. Furthermore, he said, such products draw less scrutiny from the Financial Industry Regulatory Authority, which polices Wall Street.”

http://dealbook.nytimes.com/2013/03/02/selling-the-home-brand-a-look-inside-an-elite-jpmorgan-unit- 2/?hp

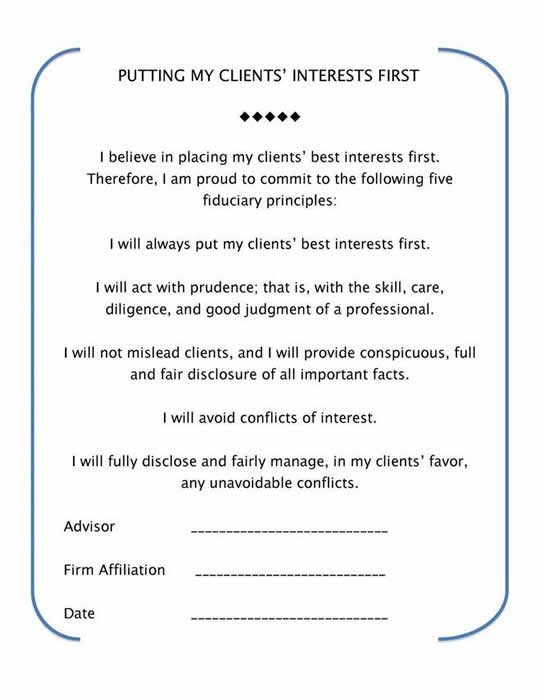

The issue for investors is, “Will your interest be placed first?” There are lots of good brokers and investment advisors, but it’s up to you to ensure your interest is protected. Although there are no

guarantees, one way of mitigating the risk of conflicting advice is to have your financial advisor sign the “mom-and-pop” fiduciary commitment developed by the Committee for the Fiduciary Standard. I’ve attached a copy at the end of the NewsLetter.

GOLF ANYONE?

Golfers like to brag not only about their scores but also golfing in general. Here are a few impressive statistics that my golfing readers might want to use to impress their non-golfing friends.

- Total annual economic impact - $176.8 billion!

- $3.9 billion was the national charitable impact of golf in 2011.

- Golf courses provide 2,020,060 acres of greenspace in the U.S. alone.

- 2,500 square feet of turf-grass releases enough oxygen for a family of four to breathe.

Walking 18 holes is equal to a 5-mile walk and playing 18 holes burns roughly 2,000 calories. [Josh says “nonsense!” The number of calories burned seems over stated. I burn 700 calories running at full speed for an hour at my weight. Here is what I found for calorie burn related to golf http://www.mycaloriesburned.com/calories-burned-playing-golf/.]

All this cool information is from Martina, who is actively involved in planning many charitable golfing programs.

SOAP BOX

If you’ve been reading my NewsLetters for very long, you know I’ve been active with a number of professional friends in pushing Congress and regulators to establish a serious fiduciary standard for anyone providing personalized investment advice. Well, recently the SEC sent out a request for comment regarding this issue. I responded with what I believe is a simple, credible “mom-and-pop” solution to the issues. If you’d like to see my response, just let Martina know ([email protected] or 305 448-8882 x235).

OH MY

More bad news for gurus from Institutional Investor. “The results are in and they are persistent. Institutional investors – from mutual funds to endowments to pension plans – are below average

when it comes to doing their job.”

FOR OLD PEOPLE

- Reporters interviewing a 104-year-old woman asked: “And what do you think is the best thing about being 104?” She simply replied, “No peer pressure.”

- I feel like my body has gotten totally out of shape, so I got my doctor's permission to join a fitness club and start exercising. I decided to take an aerobics class for seniors. I bent, twisted, gyrated, jumped up and down, and perspired for an hour. But by the time I got my leotard on, the class was over.

- The Senility Prayer: God grant me the senility to forget the people I never liked anyway, the good fortune to run into the ones I do, and the eyesight to tell the difference.

Thought For The Day from a woman: I don’t want to brag or make anyone jealous or anything, but I can still fit into the earrings I wore in high school.

IT DOES WHAT?

Ever wondered how Google works? It gives a new meaning to Rube Goldberg. Go to http://www.ppcblog.com/how-google-works/ (a blog post from one of our clients) and you’ll see. Below is just the “tip of the iceberg”.

I’LL SURE MISS HIM

I recently learned that Walter Updegrave may be retiring from Money. Walter always had something worthwhile to say and one of his last columns was no exception. Addressing the frequently asked question, “If interest rates rise, the value of my bond funds will fall. Should I take money out now?” he sagely answered, “Decide how much of your savings should be in bonds …Then stick to that percentage regardless of what prognosticators say rates may do…But whatever you do, don’t abandon bonds altogether: despite today’s low rates, they still deserve a place in your portfolio.” Couldn’t agree more!

MEA CULPA

I’m always picking on gurus, but that doesn’t mean I don’t enjoy pretending to be one. Here I am at the Tiburon CEO Conference in New York.

IT WORKS

Apropos of Walter’s advice, I recently chatted with a reporter that pointed out to me that the stats from S&P show that from 2009-2012—during a period of recovery—just 25.7% of U.S. stock funds beat their respective indexes. That got me wondering about how the combination of allocation and rebalancing (i.e., an investment policy) fared during the Great Recession. So, I looked at the return of a static 40% bond/60% stock portfolio versus a similar one that was rebalanced (I used the Vanguard Balanced Index) and here’s what I found.

|

From 10/2007 to 3/31/2013 |

|

|

Bond Index (40%) |

37.3% |

|

S&P 500 (60%) |

16.1% |

|

40% bond and 60% stock |

24.6% |

|

Vanguard Balanced index |

30.5% |

I also looked at “recovery” from 10/2007 (about the market peak)

Rebalanced balanced (Vanguard) was back in the black by 10/2010 S&P didn’t recover until almost two years later (7/2012)

A PLUG

I, along with a number of clients, write books and I’d like to introduce you to the latest – How To Survive Within Our Healthcare System (Volume 1) by Philip A. Scheinberg M.D. and Linda A. Scheinberg R.N. Linda wrote to us that “ Phil and I have spent a couple of years or more writing a book that we believe will be of value to anyone who reads it. It has given us the opportunity to provide ongoing medical advice that is critical to everyone. The journey has been exciting and we are proud of the result. We hope it will become a part of your library.” A number of us at E&K now have our own copies and we agree. You can get yours at: http://www.amazon.com/s/ref=nb_sb_noss?url=search-alias%3Daps&field- keywords=How+To+Survive+Within+Our+Healthcare+System.

BUMMER

According to a recent study by Natixis Global, the United States ranks 19th in the quality of retirement available to senior citizens. The study reports that the low ranking is due mainly to the better social and healthcare safety nets that exist in European countries that outranked the United States.

There were 150 countries included in the study about future needs. Coming out on top were Norway, Switzerland, Luxembourg, Sweden, and Austria, with other U.S.-beating countries including the Czech Republic, Japan, Slovenia and Slovakia.

According to Financial Advisor, the really depressing conclusion was, “The economic downturn has also taken a major toll on retirement savings. Fifty-three percent of American workers 30 and older are on a path that will leave them unprepared for retirement, up significantly from 38 percent just two years ago.”

The only silver lining is that there will be an increasing need for good financial planning.

GOOD NEWS OR BAD NEWS?

From my friend Allan Starkie’s News Posting: “The report, Water Water Everywhere, examined 358 hedge funds and found that, while the majority of managers polled (55 per cent) predict better performance in 2013 versus 2012, nearly half (42 per cent) believe this year will prove “difficult or somewhat difficult” for the hedge fund industry.” I’m rooting for the 55%.

WHO KNEW?

According to Bloomberg Businessweek, honeybees annually pollinate $201 billion worth of crops; without their dilligent work, we wouldn’t have crops that provide about 90% of the planet’s food. So, I guess I shouldn’t be surprised to read in Fortune that the earnings from renting bees just for the almond bloom earns $228 million. Incredibly, that’s almost as much as the $258 million earned from all honey production.

IT’S ABOUT TIME

Women now account for more than 50% of all workers in high-paying management, professional and related occupations, and, according to the DOL as reported in Financial Planning, women are projected to account for 51.2% of the increase in total labor force growth through 2018.

ONE WORD ESSAYS

From my friend Peter

DETERMINATION EXCITEMENT CURIOSITY

CONFUSION AWE FRIENDHIP

SO MUCH FOR GURUS

A recent Aspiriant newsletter reminded readers that in “December 2010, well-known analyst Meredith Whitney appeared on 60 Minutes and predicted ‘50 to 100 sizable defaults’ in the municipal bond market due to the deteriorating fiscal situation in cities and states across the country. The concerns she raised resulted in record asset outflows from municipal bond mutual funds – $4 billion flowed out of municipal bond mutual funds in the week ended January 19, 2011, the most since 1992, when Lipper started tracking the data. That week’s outflow marked the 10th straight week of net redemptions, totaling $20.6 billion, according to Lipper.”

What actually happened? From 2/1/2011 to 2/1/2013, the Barclay Muni 10 year index was up 19.5% or an annualized 9.3% (and that’s tax free). The moral is beware of gurus and financial pornography.

Adding guru insult to guru injury, the latest S&P SPIVA Scorecard found:

- 63.25% of large-cap funds, 80.45% of mid-cap funds, and 66.5% of small-cap funds underperformed their benchmark indices.

- 66.26% of global equity funds underperformed their benchmarks over the past three years. (http://now.eloqua.com/es.asp?s=795&e=721851&elq=c464f7652f664c2e980cd3d8f02c6e50) Institutional managers are well aware of these kinds of stories. For example, Pension & Investors reports that CalPERS, the California retirement system and the largest public pension fund in the United States, is considering whether active managers, once fees are taken into consideration, achieve better returns than the fund's passive index strategies. Today more than half of the $250 billion plan is passive.

Kind of explains why, in spite of our agnostic philosophy, our equity allocations are dominated by cost and tax-efficient index/passive funds.

GURLS RULE, BOYS DROOL

With a headline like this, I couldn’t resist. From the pages of Rep magazine, here are the results of female hedge fund managers compared to the male dominated (84%) global hedge fund universe.

Women HFRX Global Hedge Fund Index

|

Compound Annual Return |

3.6% |

-3% |

|

Largest Monthly Gain |

7.3 |

3.1 |

|

Largest Monthly Loss |

-7.6 |

-9.3 |

THE FUTURE

The Apple Watch

I’m ready! Rumor is its due out soon. According to Forbes, it could have “…multiple applications such as secured-building entry, secure computer or device access, or even secure car or home entry. The Biometrics assures the iWatch wearer is the authenticated user and provides an additional layer of authentication, which could be very important across the board from enterprise to personal security.” Cult of Mac writes “Someone sends you a text or posts a picture on Facebook, you’ll get calendar meeting alerts and other standard types of incoming information, and they will flash on the watch. Siri will nudge you about all kinds of random things: “You’re near the cleaners — pick up your laundry,” or “Do you want me to remind Steve about your meeting?”

I believe Apple will enable custom haptics (haptics are the buzzes and rumbles of physical motion you feel when your phone is on vibrate) for the iWatch. You’ll be able to set up custom vibration patterns for specific people and/or specific types of information, so you won’t even need to look at the watch to get some kinds of messages. You’ll be given enough information by buzzing to make a decision even to look at the watch or not look. For example, you’ll have a specific pattern of buzzes for incoming text messages and another pattern when someone in your “Close Friends” group on Facebook posts a status update.

Read more at http://www.cultofmac.com/220962/why-the-apple-iwatch-will-have-these-6-killer- features/#GpxlKDQfi0KAruVg.99

Google Glasses

Here’s Techradar’s take: “The core of Google Glass is its tiny prism display which sits not in your eyeline, but a little above it. You can see what is on the display by glancing up. The glasses also have an embedded camera, microphone, GPS and, reportedly, use bone induction to give you sound. Voice control is used to control the device; you say 'ok glass' to get a range of options including taking pictures, videos, send messages using speech to text, ‘hang out’ with people or get directions to somewhere. You access these options by saying them out loud. Most of this functionality is self- explanatory; hang out is Google's video conferencing technology and allows you to talk to a people over web cam, and stream them what you are seeing and the directions use Google Maps and the inbuilt GPS to help you find your way. The results are displayed on the prism - essentially putting data into your view like a head up display (HUD). It's potentially incredibly handy. Also rather nifty is the potential for automatic voice and speech recognition. People are already developing some rather cool/scary apps for Google Glass - including one that allows you to identify your friends in a crowd, and another that allows you to dictate an email.”

Graphene Aerogel

This amazing ultra-light aerogel has a density lower than that of helium and just twice that of hydrogen. Created by a research team from China’s Zhejiang University, the material is very strong and extremely elastic, bouncing back after being compressed. It can also absorb up to 900 times its own weight in oil and do so quickly, with one gram of aerogel able to absorb up to 68.8 grams of organics per second – making it attractive for mopping up oil spills at sea. Better yet, due to its elasticity, both the oil absorbed and the aerogel can be recycled. No telling what other neat uses may be developed.

FOR SOMEONE WHO HAS EVERYTHING

Here are a few gifts ideas highlighted in Architectural Digest for those who don’t worry about retirement.

Cartier stainless desk clock - $7,500 – of course it’s a sizeable 6” x7”

Set of Pratesi queen size sheets - $5,700 and Pillow shams at only $990 each – can’t put a price on comfort.

SHE REALLY CARES AND I AGREE

Back in 2010, under the auspices of Ms. Phyllis Borzi, Assistant Secretary of Labor, the DOL proposed a rule expanding the duty of “fiduciary” to include IRA accounts (they are not currently protected under a fiduciary standard). Not too surprisingly, there was fierce resistance from many in the financial services world and the proposal was withdrawn. Well, a few months ago, I and a few of my fellow Fiduciary Committee members had the opportunity to meet with Ms. Borzi and her staff. We were extremely impressed with her understanding of the issues and left convinced that the DOL would resubmit its earlier proposal.

For me the major “take-away” was the reason for Ms. Borzi’s strong belief in the importance of the proposed change. As with many practitioners who have been in the trenches for decades, I tend to think of IRA’s as small accounts with funds accumulated from modest $2,000+ annual contributions. What Ms. Borzi reminded us of is that we’re not talking about small dollars; there are currently in excess of $5 trillion in defined contribution plans (largely 401Ks). Those dollars are currently under professional management and are protected under the stringent fiduciary

from their pension into an IRA, they will lose both professional management and the fiduciary protection. The DOL believes investment advice for those retirement dollars should continue to be protected by a fiduciary standard. I agree.

Rumor is that the DOL will reissue its proposal soon. I’ll keep you posted. Here’s why Ms. Borzi is concerned:

GAO Investigates IRA Rollover Practices by Money Management Firms. Seven out of 30 money management firms encouraged IRA rollovers with misleading statements, according to a GAO report to be released today.

The Washington Post’s Michael Fletcher reported Tuesday on the GAO study, which looked into misleading fee disclosure and marketing practices by money management companies regarding IRA rollovers from 401(k) plans. Undercover personnel from GAO contacted 30 money management firms, posing as workers about to change jobs. Seven of the firms provided incorrect information, including the statement that there would be no cost to roll over the money. The GAO also found that five of 10 websites indicated that there were no fees for opening an IRA. Their conclusion: Even though it would be better for employees to leave their money in their current plans, the firms encouraged IRA rollovers with misleading statements to harvest bigger fees.

Roughly 90% of new IRA money comes from employer plans.

GOOD NEWS (I THINK)

Don’t know if we’re eating cheaper or just less. According to Bloomberg Businessweek, the average

U.S. housdehold annual allocation to food dropped over 30% in less than 30 years. Today, as a percentage of income, we spend half as much as households in France and only a quarter of those in India.

CONFIRMATION

Craig Israelson, a professor at Bringham Young, writes a regular (and excellent) investment column for Financial Planning magazine. In his “Tale of the Tape: Value vs. Growth,” he revisits the past research and finds “…a real difference in performance.” His conclusion: “These findings do not argue for the eliminating growth-oriented assets from a portolfio. They do suggest, however, that overweighting value stocks is justified in the long run – particlurly among small-cap U. S. stock mutual funds.” As we’ve overweighted small and value for decades, this is good news.

SPEAKING OF INVESTMENTS

It’s always nice to find others catching on. We’ve been major users of ETFs for many years and Research Magazine reports that last year investments in ETFs jumped 27.6%. Today they hold over $1.3 trillion in assets.

FUNDAMENTALS? FORGET ABOUT ‘EM!

That’s the title of an excellent article by Paul Lim reporting on a Vanguard study. I’d subtitle it “Overconfidence.” Roger Aliaga-Diaz, one of the co-authors, noted, “We’re not saying fundamental factors don’t matter. Rather, it’s that using fundaments to predict the future doesn’t work because so many other factors can drive returns above or below historical averages for long stretches.” Jason Hu, chief investment officer at Research Affiliates, adds, “Market earnings forecasts aren’t useful

either. Not only are analysts overly optimistic, but they ‘tend to move in herds-they don’t want their forecasts to be that different from what others are saying.’”

According to Vanguard:

Measurement % of Returns It Explains

Shiller 10 yr P/E 43.5%

Dividend yield 17.6%

Rainfall 6.0%

Trailing GDP growth 5.4% Trailing earnings growth 0.8% Corporate profit margins 0.5% Earnings and GCP forecasts 0.1%

Worth keeping in mind the next time you believe you can accurately divine the market future by analyizing the current available fundamnetal data.

MORE GOOD NEWS

I’ve reported before about the dire outlook for some law school grads, but it seems that for those that do have jobs it’s not so bad. According to the ABA Journal current salary ranges look like:

|

Experience |

Firm Size |

Salary Range |

|

First Year |

10-35 |

$58,250-$84,750 |

|

4-9 years |

10-35 |

$87,250-$157,500 |

|

35-75 |

$119,750-$178,250 |

IT’S NOT JUST GLOBAL MARKETS

I frequently write about investment globalization, but a recent article in Accounting Today reminded me it’s not just markets. Last year, over 2,000 took the CPA exam in Japan and almost 1,500 did in South Korea. The fastest growing area is the Middle East, with an increase over 150% in the Palestinian Territories and over 100% in Kuwait.

IF YOU’VE HAD TOO MUCH GOOD NEWS

CFA Institute’s magazine provides a solution in it’s article “Time-Bomb Zombie Swans From Outer Space.” As the story points out, there are lots of things investors know to worry about, but what ought to keep us up at night are the black swans (i.e., an unanticipated event that has a major impact) we don’t see. Their list included:

Derivatives Blow Up Japan (Finally) Implodes The Petrodollar Dies U.S. Pension Defaults Spike A Debt Jubilee Resets the System (i.e., a widespread forgiveness of debt engineered by the government). Cyber attack that cripples the economy.

Unfortunately, I don’t have room to describe each of these, but the article makes a credible case for each. You can find it at http://www.cfapubs.org/doi/pdf/10.2469/cfm.v24.n2.10.

Of course, it left out the rather obvious “What about Cyprus?”

KID STUFF

In my last NewsLetter I showed a crayon bandolier for kids. Well, Anne who is expecting her first child pretty soon sent me an alternative for girls, although she’ll have to plan on the bandolier as her soon- to-be, Casen, is a little boy.

http://cberrybaby.blogspot.com/2008/08/giveaway-new-crayon-apron-designs.html

Parenting listed this as one of the best toys for kids of all ages. http://www.parenting.com/gallery/best- toys-for-kids?pnid=115435

OVER-OPTIMISTIC

A classic behavioral characteristic is over-optimism, and it alone causes many poor investment decisions. Take investing in startups: investors tend to focus on the positive (e.g., with the benefit of hindsight we know that Google is at about 10 times its IPO price) but forget the potential negative. Reality according to CNNMoney is that while 20% of startups pay off big, 40% only pay off modestly and, possibly most important, 40% fail outright. The moral? Next time you’re enamored about the possible investment in a startup be sure and consider the consequences to your lifestyle of an outright failure.

TIDBITS

From Rep magazine

- 23.5 – Factor by which the number of registered lobbyists (12,655) outnumber members of Congress (535)

- Number of commercial banks and savings institutions in the U.S. in 1913 when the Fed was established (26,000) vs. 2013 (7,657)

- 29 - Of the top 50 universities in the world, the number located in the U.S.

- $53,900 – Median pay for 2012 MBA graduates with 3 years or less experience, down 4.6% from 2007

KEEP IT IN MIND

March 9th was the four-year anniversary of the current bull market. However, NASDAQ still has quite a way to go and on an inflation-adjusted basis, we’re still below prior highs.

CNBC's Josh Brown said the other day that a 5% correction occurs, on average, three times a year. A 10% correction is, again on average, an annual occurrence. And a 20% drop hits every three and a half years. The catch is that’s “on average.” Just as I learned in my engineering classes a zillion years ago, two “100-year storms” might occur two years in a row.

Although it’s fun to bandy about these kinds of numbers, what do all those statistics tell us? It’s clear the market may make a significant correction or it may not. My point is the same mantra we constantly preach. To make money in the market you have to be in the market, and if you plan for your needed short-term liquidity (our five year mantra) you can ignore all of the financial pornography constantly predicting tomorrows market (consistently incorrectly).

CHEAP AIR

If you’re in the air as often as I am, this is handy stuff to know. Money reports that a survey by cheapair.com of 580 million 2012 fare records found the best time to buy non-holiday tickets is 49

days prior to departure for domestic flights and 81 days for international flights. For most holidays it’s

about ten weeks. According to FareCompare, the best day is Tuesday, while a Texas A&M study found weekends best for non-vacation destinations. To confirm your timing go to Kayak.com’s Price Trend or Bing.travel.com’s Price Predictor.

GOOD STUFF

As my readers know, I often include tidbits from Money Magazine and the recent “Six Secrets of Retirement” is a story worth looking up.

http://money.cnn.com/2013/02/18/retirement/investments-stocks-funds.moneymag/index.html

A REAL GURU

I’m often picking on self proclaimed gurus, but I recently came across the real deal in a Readers Digest story. It seems that in a December 1900 Ladies’ Home Journal article “What May Happen in the Next Hundred Years,” civil engineer John Watkins wrote “These prophecies will seem strange, almost impossible…” Well, as my formal education was in Civil Engineering, I was proud of and impressed with Mr. Watkin’s prognostications. Here are a few:

Television – “Man will see around the world. Persons of all kinds will be brought within focus of cameras connected electronically with screens at opposite ends of circuits, thousands of miles apart.”

Digital Color Photography – “Photographs will be telegraphed from any distance. If there will be a battle in China a hundreds years hence, snapshots of its most striking events will be published in the newspaper an hour later…photographs will reproduce all of nature’s colors.”

Express Trains – “Trains will run two miles a minute. Express trains, one hundred and fifty miles per hour.”

Prepackaged Meals – “Ready-cooked meals will be bought from establishmnets similar to our bakeries of today.”

AMAZING!!!

CLOSING NEED TO KNOW

At least for those of you with small kids. According to my friend Mark Freedman’s newsletter, “Here's a sign that the economy is improving. The Tooth Fairy Poll published yearly by Delta Dental recently announced that the average gift from the flying angel climbed to $2.42 last year. That's up from $2.10 or 15.2% from last year.” (http://www.theoriginaltoothfairypoll.com/news-release/)

As always, hope you enjoyed. Please drop me a note or give me a call (305 448-8882 x235) if there are any of these tidbits (or anything else) you’d like to chat about.

Cordially yours,

Harold Evensky, CFP®, AIF® President

FIDUCIARY OATH

© Evensky & Katz

© Evensky & Katz / Foldes Financial Wealth Management