Recent Volatility in the Foreign Exchange Market and the Strengthening Yen

There are two issues underlying the increased currency market volatility; depreciation of the Yen may have resulted in worldwide competitive devaluation and concern about early tapering of quantitative easing (QE) in the U.S. appears to have triggered currency depreciation for countries that are running current account deficits.

Depreciation of the Yen had continued in isolation until right after the announcement by the Bank of Japan (BOJ) of unorthodox monetary easing measures of a “different dimension” unveiled by Governor Kuroda on April 4. However, subsequent monetary easing by other countries has led to a situation where several countries appear to be competing to pursue weaker currencies. At the same time, several currencies have started depreciating relative to the U.S. dollar (USD), especially those that are running current account deficits or those where economic growth is stagnating.

There is a view that early tapering of QE in the U.S. is a factor behind the strong USD. However, it is worth noting that early tapering of QE might tend to drive U.S. stock prices downward, which could result in a weaker USD and a stronger Yen.

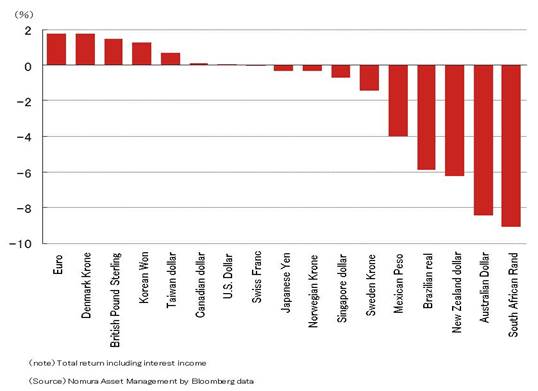

The chart below shows currency returns relative to the USD since the announcement of unorthodox monetary easing measures in April until June 10. Strong currencies include European and East Asian currencies such as the Korean won and the New Taiwan dollar. On the other hand, weak currencies, which have depreciated significantly, include natural resource producing countries in the Southern Hemisphere and high interest rate currencies.

Exchange Rate Movement Relative to USD

% Difference from April 1, 2013 through June 10, 2013

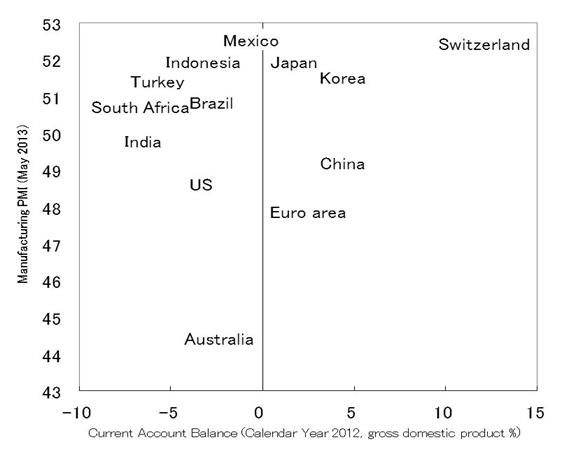

The below chart shows the current account balance on the horizontal axis, while manufacturing Purchasing Managers Index (PMI) is shown on the vertical axis (current account balance is the difference between a nation’s total exports of goods, services and transfers, and its total imports of them. The level of the current account is followed as an indicator of trends in foreign trade). Currently, there is a tendency that currencies of weak economies (low PMI) with current account deficits (at the lower left hand side of the chart) are likely to be sold (weak). The Australian dollar is a typical example. At the same time, currencies of strong economies with a current account surplus (at the upper right hand side) are likely to be bought (strong). The strong Yen recently can be explained from this perspective.

Current Account Balance and Manufacturing PMI

![]()

![]()

Furthermore, foreign exchange markets entered a “risk off” mode ahead of the stock market. For market expectations to shift back towards fund inflows to current account deficit countries with high interest rates, then the U.S. dollar would need to weaken against a wide range of currencies other than the Yen. The progress of tapered withdrawal from QE in the U.S. would be a key influence.

We maintained our view that a combination of the “three arrows” of Abenomics, Japan’s recent approach to reflating its economy, will lead to an economic recovery and stock market appreciation in Japan. At the same time, we have kept a certain distance from the commonly shared view that a loose monetary policy would lead to a significantly weaker Yen. Recent high volatility in the currency markets seems to have been the result of rapid unwinding of short Yen positions, which have been accumulated while excessive expectations for a weaker Yen have receded.

Also, the reason why we are seeing “weaker stock prices and a stronger Yen” simultaneously may be that there are many investors who believe Abenomics is synonymous with “higher stock prices and weaker Yen.”

We sense that upward pressure on the Yen will persist for a while due to the influence of global money flows. However, sales and earnings of exporters are expected to expand through volume growth even without further depreciation of the Yen. From the beginning, we thought that steady implementation of the growth strategy (the third arrow of Abenomics) would be the key to increase the potential growth rate of the Japanese economy. There is a tendency that progress on politically sensitive issues might not meet investors’ expectations before the Upper House election (which will most probably be held on July 21).

International investing involves certain risks and increased volatility not associated with investing solely in the U.S. These risks include currency fluctuations, economic or financial instability, lack of timely or reliable financial information or unfavorable political or legal developments. These risks are magnified in emerging markets. Securities focusing on limited geographic areas and/or sectors may result in greater market volatility. Investing in securities issued by smaller companies typically involves greater risk than investing in larger, more established companies.

Investors should carefully consider the investment objectives, risks, charges and expenses of each Fund before investing. This and other important information is contained in the Nomura Partners Funds, Inc. prospectus, which may be obtained by contacting your financial advisor, by calling Nomura Partners Funds at 1-800-535-2726, or visiting our website at nomurapartnersfunds.com. Please read the prospectus carefully before investing.

This report was prepared by Nomura Asset Management Co., Ltd. for information purposes only. Although this report is based upon sources we believe to be reliable, we do not guarantee its accuracy or completeness. Unless otherwise stated, all statements, figures, graphs and other information included in this report are as of the date of this report and are subject to change without notice. Forecasts, estimates, and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. The contents of this report are not intended in any way to indicate or guarantee future investment results. Further, this report is not intended as a solicitation or recommendation with respect to the purchase or sale of any particular investment. This report may not be copied, re-distributed, or reproduced in whole or in part without the prior written approval of Nomura Asset Management Co., Ltd.

Investments are not FDIC-insured, nor are they deposits or guaranteed by a bank or other entity.

Distributed by Foreside Fund Services, LLC.

© Nomura Asset Management