Equity asset allocations have become more global in recent years as investors have sought to reduce the long standing home country bias in their portfolios. Further propelling this trend has been the growing aversion to traditional asset class structures and indeed, conventional asset class definitions, in the aftermath of the 2008-2009 global fi nancial crisis. Against this backdrop, global equity strategies have continued to garner asset fl ows in Europe and have slowly begun to gain traction in the U.S. after years of tepid demand. These strategies are typically large cap developed market-oriented in nature, with signifi cant weightings in big multinational corporations, overlooking the relatively attractive global small cap opportunity set.

While the trend toward more globalized allocations is positive, investors should be mindful of the potential for unintended large cap biased exposure in their portfolios. The inclusion of dedicated small cap mandates helps to off set this bias, but the traditional approach of regionalized small cap exposure is less than optimal. Adding geographically unconstrained small cap exposure is the better solution to enhancing the risk-adjusted return profile of the overall asset allocation. In advocating for a global approach to small cap investing, this paper reviews the current global equity investment landscape and addresses some of the key benefits of global small cap.

Globalization of Asset Allocations

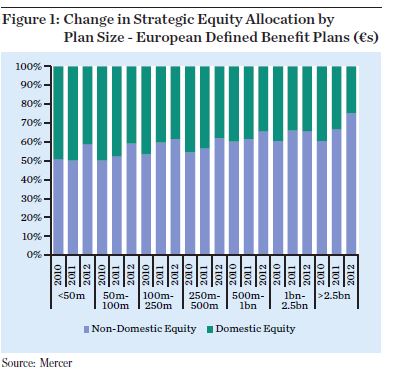

Although the search for lower volatility has driven reduced equity allocations in favor of alternatives, equities continue to play a significant role in investor portfolios. The composition of equity allocations has been evolving, however, from domestic to non-domestic oriented structures. Mercer’s recent survey of European defined benefit plans showed a significant increase in non-domestic equity allocations from 2010 to 2012 among smaller plans (less than €500m in assets), catching up somewhat with their larger counterparts who had previously adopted more globalized allocation structures.1 As illustrated in Figure 1, Mercer found that the average increase in non-domestic equity exposure as a percentage of total equity exposure for small plans was approximately 16% during the three year period, compared to 10% for larger plans (€500m to €2.5bn). Interestingly, among the largest defi ned benefit plans (greater than €2.5bn in assets), which already maintained higher non-domestic allocations, the increase was 25%. It should be noted that this group also had the largest reduction in overall equity exposure during the three year period, from 38% to 24%.

Defined benefit plans in the United States have historically maintained higher domestic equity allocations than European plans. Similar to Europe, U.S. plans have increased their exposure to non-domestic equities amid a broader reduction in equities. While a similar analysis by Wilshire of U.S. defined benefit plan allocations showed a recent moderation in the growth of "international" (non-domestic) allocations, the ten year trend was strong, with the average international allocation increasing from approximately 17% to over 30% of total equity exposure. 2 As in Europe, large plans have moved more aggressively to globalize than small plans in the U.S., maintaining a roughly 60/40 domestic/international percentage split versus 80/20 for smaller plans.

Global Equity Implementation

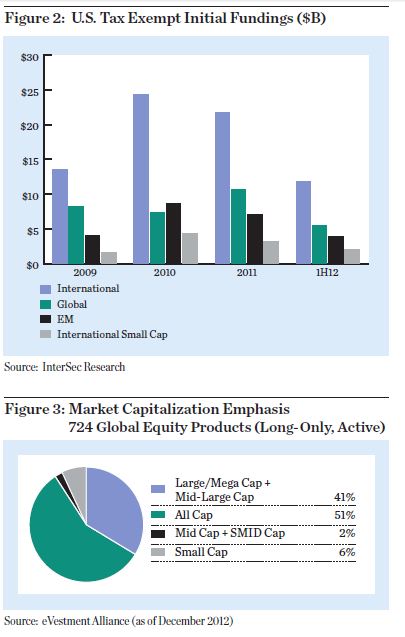

Global equity strategies have been increasingly utilized by investors in recent years, reflecting shifting equity asset allocation structures. While U.S. investors have generally preferred to maintain control of the domestic/international split through a more traditional structure that separates U.S. equities from international, many have carved out space for dedicated global managers. Funding activity from InterSec Research (Figure 2) illustrates the significant asset flows from U.S. tax-exempt investors into global equity strategies relative to other international mandates from 2009 onward. It would be reasonable to expect global equity to gain a greater share of initial fundings prospectively given the growing demand for broader mandates and greater capacity constraints in emerging markets and international small capitalization strategies.

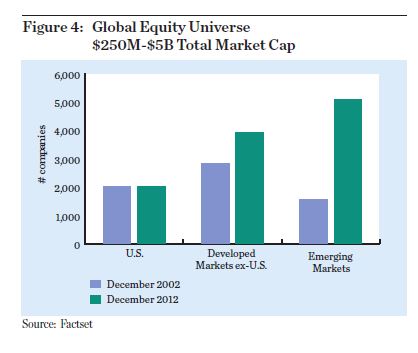

Looking more closely at the composition of initial global equity fundings during this time period, InterSec found that the vast majority of flows were into strategies benchmarked to the larger cap-oriented MSCI World and ACWI indices. This is consistent with historical flows and the broader global equity manager universe, which is dominated by large cap strategies. An analysis of over 700 actively managed long-only global equity products on the eVestment Alliance database points to a significant large cap bias among the universe of investment managers, as evidenced by stated market cap emphasis (Figure 3). While approximately half of this sample was defi ned as All Cap, the weighted average and median market caps reported for these All Cap products suggest a meaningful large cap orientation.

The dominance of global large cap allocations and strategies argues for a more diversified approach to global equity investing. As outlined in the next section, the addition of a dedicated global small cap mandate can improve the overall equity allocation risk/return profile and help investors better achieve their objectives.

Global Small Cap Universe

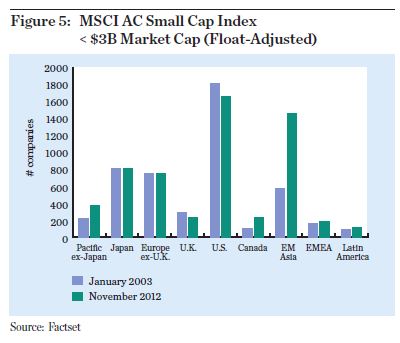

The global small cap universe has grown signifi cantly in the last 10 years, from approximately 6,400 companies to over 11,000 currently. As illustrated in Figure 4, this growth has been almost exclusively outside of the U.S., with significant expansion in developed ex-U.S. and emerging markets small cap. Growth in the latter has more than tripled during the 10 year period, as emerging market economies have stabilized and capital markets have developed.

The MSCI All Country World Small Cap Index has reflected this trend in its changing composition since its inception in early 2003. An analysis of geographic sub-regions focusing on the investable small cap opportunity set, as measured by free float-adjusted market capitalization less than $3 billion, highlights the tremendous growth in the Emerging Asia region (Figure 5). Within developed markets, the number of small cap index companies in Pacific ex-Japan and Canada has significantly outgrown Japan and Europe ex-U.K., while the U.S. and U.K. have actually contracted.

Although company growth has been strongest in the Emerging Asia region, which includes China, India, Korea, Taiwan and Indonesia, the traditional developed markets of the U.S., Europe and Japan continue to comprise a majority of the small cap universe. Adopting a global approach to small cap thus provides exposure to the expanding universe of small companies while maintaining a balanced diversification profile across high growth and mature economies, allowing managers to find the best companies regardless of domicile.

Small Cap Portfolio Implementation

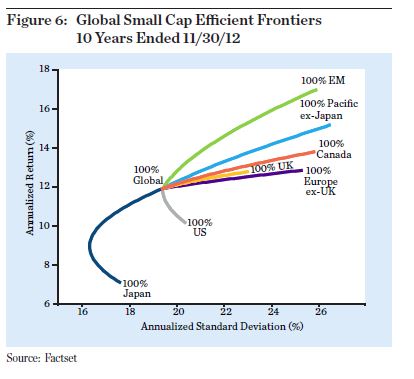

Investors have traditionally pursued a regionalized approach to small cap investing, maintaining a mix of local market and international small cap managers and retaining control of the regional allocation split. One limitation of this approach is that certain countries or regions can be underrepresented. For example, non-U.S. small cap asset owners and investment managers commonly utilize developed market-only benchmarks such as the MSCI World ex-U.S. Small Cap or EAFE Small Cap, and may be structurally underweight emerging markets small cap. Long term historical efficient frontiers for the MSCI small cap regional indices illustrate the risk/return tradeoff of regional versus global allocations. As shown in Figure 6, a global small cap mix offers attractive risk-adjusted returns

relative to individual regions.

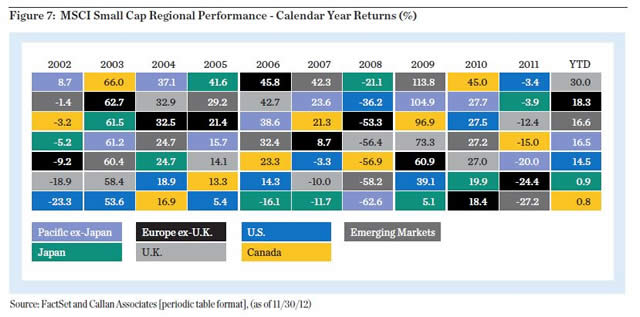

The historical risk-adjusted return profile of emerging markets small cap underscores the case for truly global small cap exposure that includes these high growth markets in a balanced approach. The efficient frontier analysis also highlights the suboptimal risk/reward profi le of U.S. small cap relative to the global portfolio. Figure 7 further illustrates the importance of broad regional diversification, with substantial variation in regional returns on a calendar year basis. The wide dispersion of annual returns also bolsters the argument for global small cap diversification and allowing managers the ability to decide amongst opportunities across sectors and regions. While regional divisions within small cap equity allocations are unlikely to be fully replaced by global structures in the near term, the historical evidence suggests that investors should consider integrating global small cap mandates into existing portfolios.

Global Security Selection

When considering the merits of global small cap and potential success of adding this type of unconventional exposure, it is instructive to focus on the potential value added through geographically unconstrained stock selection. Return correlations have generally increased across a range of asset classes in recent years, contributing to the popularity of alternative investments. This trend has also been evident in small cap equities. As Figure 8 illustrates, rolling three year correlations between U.S. and international small cap have increased measurably since the global financial crisis, mitigating some of the effectiveness of regional diversification. Security selection and sector eff ects become increasingly important in a rising correlation environment, contributing to the attractiveness of an active global small cap approach emphasizing fundamental stock selection across global sectors. Viewing the world through a global sector lens is much more meaningful in this context, and incorporating the broadest representation of sectors and stocks into the selection process is critical. Figure 9 compares sector weightings for the broad global small cap index to the primary regional small cap indices, highlighting the more balanced sector opportunity set available to a global small cap manager.

Maintaining a broad global sector perspective is consistent with the globalization of supply chains and customer bases, even for small cap companies as costs and barriers to conducting business across borders decrease. A global mandate provides the opportunity to compare a potential portfolio candidate to industry peers regardless of domicile, allowing investment managers the freedom to identify who they believe to be the best companies globally in each sector.

Globally integrated research is the key to unlocking the potential of a geographically unconstrained small capstrategy. This contrasts with the less effective “bolt-on” approach whereby separate regional strategies are loosely combined to arrive at a “global” portfolio. True integration of research across regions facilitates the expression of a team’s highest conviction investment ideas. In an effort to illustrate the framework for an integrated approach to research, Figure 10 provides a two dimensional view of sector and region exposure for a hypothetical global small cap portfolio. In reviewing Consumer sector opportunities, for example, a globally integrated research team has the ability to effectively compare and contrast specialty retail and apparel companies based in the U.S., Germany and China both relative to their respective local competitors and in a global peer context. In the hypothetical portfolio example, this exercise has resulted in the inclusion of several compelling Consumer investments across regions, with an emphasis in the U.S. and emerging markets.

By further example, if the manager believes the U.S. Industrials opportunity set to be superior relative to the non-U.S. universe based on fundamental cross-border analysis, that viewpoint can be fully expressed in a global portfolio context, whereas the inherent limitations of a non-U.S. portfolio would lead to either a reduced Industrials weighting or potential investment in lower preference companies.

Conclusion

In advocating for global small cap investing, this paper has highlighted shortcomings in the current approach to global equity investing and described some of the key benefits of global small cap and how it can be most effectively implemented. Small cap investing has always been an exciting area ripe with undiscovered opportunities. The pursuit of these opportunities in a geographically unconstrained approach should appeal to investors seeking to move beyond traditional asset allocation boundaries.

1 Mercer Asset Allocation Survey: European Institutional Marketplace Overview 2012

2 Wilshire Trust Universe Comparison Service: Asset Allocation Trends for Defined Benefit Plans. Benefits Magazine, November 2012

Important Disclosure

This material is provided for general information purposes only and is not intended as investment advice or a recommendation to purchase or sell any security. Any discussion of particular topics is not meant to be comprehensive and may be subject to change. Any investment or strategy mentioned herein may not be suitable for every investor. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed.

Information and opinions expressed are those of the presenter. Information is current as of the date appearing in this material only and subject to change without notice. Past performance is not indicative of future results. For more information, please visit williamblair.com. Forward looking statements and outlook for investment returns are for illustrative purposes only and may not reflect actual results achieved.

© William Blair