A Sweet Find on an African Adventure

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

After traveling nearly 6,000 miles by plane, helicopter and jeep, Evan Smith, portfolio manager at U.S. Global, is walking along a dirt path in Kenema past dilapidated shops covered with rusted, corrugated metal. He can hardly believe he has arrived at his destination. Surrounded by hundreds of miles of forest and savannah, it's tough to imagine an agricultural diamond-in-the-rough nearby.

Kenema is in Sierra Leone, a country in the Western part of sub-Saharan Africa with 5.6 million people recovering from a decade-long civil war that ended 11 years ago. Today, the rural people, mostly farmers and fishermen, are peaceful and friendly, says Evan.

To get here, Evan flew from San Antonio, Texas to the largest city in Sierra Leone, Freetown, making stops in New York City, Ghana and Liberia. Then he boarded a four-person helicopter to fly east 150 miles, enduring heart-pounding drops and lifts between clouds and mountains before safely arriving at a cocoa plantation development.

The heart of Africa has been beating strong in recent years due to elevated commodity prices and resilient domestic demand, despite the global economic slowdown. Among the sub-Saharan African countries, Sierra Leone was the fastest growing country last year, according to the World Bank. Its economy experienced growth that is as rare today as Fancy Red diamonds. GDP increased a whopping 18 percent.

Non-profit organizations are taking note of the country’s progress. The Freedom House recently categorized Sierra Leone as a free country, which is unusual in sub-Saharan Africa. Among 50 countries and 900 million people, only 13 percent of people are considered free under the organization’s definition.

Sierra Leone is also becoming more attractive for business. In the World Bank’s Doing Business 2013 report, the country ranked 140, up from 148. One of its main findings this year is that “among the 50 economies with the biggest improvements since 2005, the largest share—a third—are in sub-Saharan Africa.”

Looking ahead, these countries are expected to be among the fastest growing economies in the world. The International Monetary Fund estimates that out of the top 20 countries with the highest projected compound annual growth rate from 2013 through 2017, 10 are in this area of the world.

This is the growth Agriterra is looking to capture in its development of a cocoa plantation that Evan traveled across the Atlantic Ocean to check out. Agriterra is a London-based company that invests in African agricultural businesses to serve the fast-growing economies of frontier markets, such as Mozambique and Sierra Leone.

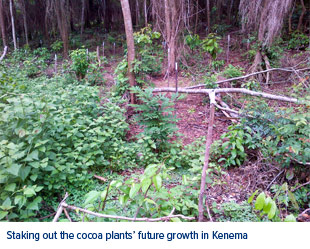

When Evan toured the grounds, he snapped pictures of the initial stages of development, as the company nurtures 250,000 seedlings in a technically advanced and irrigated nursery. Each cocoa sprout is planted in its own bag, under a canopy of screens which provides just the right amount of light. An irrigation system nourishes the plants, delivering the perfect amount of water and fertilizer.

After a few months, the seedlings will be mature enough to be transplanted to an area that provides the right amount of shade. You can see a three-meter grid of stakes designating where each plant will go in this photo below.

You may not think about where your Godiva chocolate originates, but the areas are limited. Cocoa grows best along the equator belt between the Tropic of Cancer and Tropic of Capricorn. Tropical conditions of plentiful rain and high humidity are ideal and “shading is indispensable in a cocoa tree's early years,” says the International Cocoa Organization (ICC).

While Sierra Leone is geographically situated along this band, it isn’t among the largest cocoa-producing countries. Most of the world’s chocolate originates from beans grown in Côte d'Ivoire, Ghana and Indonesia. Cocoa has traditionally been raised on small, individually owned farms, many of which have aging plants and therefore, lower yields. But with Agriterra’s advanced applications and solid operations, the development seems to be off to a sweet start.

So why is an oil and materials manager getting his boots dirty in Sierra Leone? The cocoa plantation is only one example of a company producing a commodity that we believe will be sought by the world’s growing middle class population. As more and more people reach this status, consumption of discretionary items, including chocolate, should increase.

Rather than limit the fund to energy and materials stocks, the portfolio managers take a multi-faceted approach, looking at 10 industries. By including companies such as grain processors, plantations and ranch lands, and agriculture companies, such as chemical and fertilizer stocks, we believe the fund can enhance returns with less volatility.

That’s why we keep our eyes open and boots on the ground because you never know where in the world you’ll find a sweet or savory opportunity.

Thanks to Evan Smith, who contributed to this commentary.

Drive for Five!

We hope our readers are rooting with us for the Spurs in their “Drive for Five!” battle against the Heat in the NBA Finals. With fierce competition between the teams—now tied 2-2—it’s bringing out the best in the players. Miami’s Big Three are tough to beat, but we are confident that Tim Duncan, Tony Parker and Manu Ginobili will bring home the championship trophy once more. GO SPURS GO!

Index Summary

- Major market indices closed lower this week. The Dow Jones Industrial Average fell 1.17 percent. The S&P 500 Stock Index moved lower by 1.01 percent, while the Nasdaq Composite dropped 1.32 percent. The Russell 2000 small capitalization index declined 0.63 percent this week.

- The Hang Seng Composite fell 2.87 percent; Taiwan declined 1.95 percent while the KOSPI dropped 1.80 percent.

- The 10-year Treasury bond yield fell 5 basis points this week to 2.13 percent.

Domestic Equity Market

The S&P 500 finished lower this week on global central bank policy uncertainty. The traditionally defensive groups were the best performers in an otherwise sloppy market.

click to enlarge

Strengths

- The telecom services sector was the leader for a second week in a row with AT&T and Verizon both continuing to grind higher after their recent sell-off.

- The health care sector was the second best performer, posting essentially flat performance for the week. Leaders were from a variety of industries, but outperformers included CR Bard, AmerisourceBergen and Pfizer.

- Gannett was the best performer in the S&P 500 this week gaining 20.20 percent. The company announced the acquisition of Belo, which solidifies Gannett’s position in the TV affiliate space and further diversifies the business.

Weaknesses

- The financials sector was the worst performer this week. Household names such as American Express, Citigroup and Morgan Stanley were among the worst performers.

- The energy sector also lagged this week as coal names were especially weak with Peabody Energy falling more than 10 percent and CONSOL Energy falling 5 percent. Coal prices remain very depressed and are pressuring many companies in the industry.

- First Solar was the worst performer in the S&P 500 this week, declining 15.78 percent. The company announced a secondary equity offering totaling $391 million, resulting in roughly 9 percent dilution.

Opportunity

- The current macro environment remains positive, as economic data remains robust enough to give investors confidence in an economic recovery, but not too strong as to force the Federal Reserve to change course in the near term.

- The market pulled back 5 percent and bounced right on cue, as it has done all year.

Threat

- A market consolidation could continue in the near term, as the S&P 500 had trended higher beyond its all-time record for a month, defying the proverbial “Sell in May” seasonal pattern.

- Mortgage rates stayed above 4 percent this week, and if housing were to slow down or pause for a period of time, that could be a significant drag for both the real economy and the markets.

The Economy and Bond Market

Treasury yields fell this week as Fed “tapering” (reducing quantitative easing (QE) and taking the first step on a long road toward tightening monetary policy) fears receded. The Fed meets next week and expectations are for the Fed to downplay the likelihood of an early end to QE. Mortgage rates have reacted to this tapering talk and have spiked sharply in the past month, rising to more than 4 percent, which is not likely what the Fed had intended.

click to enlarge

Strengths

- The National Federation of Independent Business (NFIB) sentiment gauge rose in May on relatively broad-based strength. This indicator provides a good read on small business sentiment.

- In a Manpower survey, 22 percent of firms intend on hiring or adding staff in the third quarter, which is the highest level in four years.

- Retail sales rose 0.6 percent in May, driven by strong auto sales.

Weaknesses

- Industrial production for May was unchanged and below expectations for modest growth.

- The Bank of Japan disappointed the markets this week by not expanding current policies and the financial markets reacted violently, indicating the fragile psyche of investors.

- University of Michigan Confidence Index came in below expectations for June.

Opportunity

- The Fed continues to remain committed to an extremely accommodative policy.

- Key global central bankers, such as the European Central Bank (ECB), Bank of England and the Bank of Japan, are still in easing mode. The Bank of Japan in particular is aggressively easing and the ECB recently cut interest rates.

- The recent sell-off in bonds may be an opportunity as growth remains weak, and this wouldn’t be the first time the markets got ahead of themselves.

Threat

- Inflation in some corners of the globe is getting the attention of policy makers and may be an early indicator for the rest of the world.

- Trade and/or currency “wars” cannot be ruled out which may cause unintended consequences and volatility in the financial markets.

- The recent bond market sell-off may be a “shot across the bow” as the markets reassess the changing macro dynamics.

Gold Market

For the week, spot gold closed at $1,390.74, up $7.69 per ounce, or 0.56 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, lost 3.12 percent. The U.S. Trade-Weighted Dollar Index lost 1.22 percent for the week.

Strengths

- The negative correlation between the U.S. dollar and gold has increased dramatically as of late, giving analysts one more tool to consider when looking at the price of gold. As the chart shows, the trade-weighted dollar has weakened significantly over the last few days, mainly due to a lower pace of monetary easing by the Bank of Japan and the European Central Bank, and the resulting strengthening of the Japanese yen and the euro. The dollar weakness should bode well for higher gold prices.

click to enlarge

- Klondex Mines reported metallurgical sampling results for May with an average diluted grade of 74 grams per ton. The high grade of the material allows for it to be direct smelted, which leads to typical recoveries in the high 90 percent range. As a result, Klondex has the potential to generate meaningful near-term revenue, according to Michael Dilay of Casimir Capital. On the same note, Torex Gold announced it has received final approval of its Environmental Impact Assessment for its Morelos project in Mexico. The company expects to begin construction as early as July of this year, which significantly de-risks its Morelos project and the overall valuation of the company.

- Over the past two years, Eldorado Gold is the best performer in the NYSE Arca Gold Bugs Index (HUI), which highlights the importance of overweighting the low-cost producers, and ensuring they can grow sustainably throughout the commodity cycle. Alamos Gold is not a component of the HUI Index, but it also compares favorably; it has a low-cost profile, is growing its production per share, paying a dividend, and repurchasing stock. See our CIO Frank Holmes’ Three Reasons to Buy Gold Equities Today and a Case Study on Ala mos Gold.

Weaknesses

- Nouriel Roubini published another article this week in which he continued to refer to gold’s run up to $1,900 per ounce as a bubble, and gives his opinion as to why the bubble has burst. Thanks to Chris Kwan at BMO, we were directed to comments from George Milling-Stanley – a former member of the World Gold Council – that refute Mr. Roubini’s claims. According to Milling-Stanley, a study from the World Gold Council titled “The 10-Year Gold Bull Market in Perspective,” dated September 17, 2010, demonstrated conclusively that trends in the gold price during this bull market had nothing in common with four acknowledged bubbles: gold in the 1970s, Japanese equities in the 1980s, tech stocks in the run-up to 2000, and real estate prices in the period preceding the crash in 2007.

- Not only has Newcrest Mining delivered news of a $6 billion write-down in asset values, Mineweb reports the Australian Securities Exchange (ASX) has questioned Newcrest over the timing of the profit warning, which was issued after several brokers had revised down their forecasts for the company, raising concerns in the market that some analysts had been briefed ahead of time. Newcrest Mining has responded to the inquiry by denying any wrong-doing.

- Kinross Gold announced it will abandon the development of its Fruta del Norte deposit in Ecuador, given the inability to negotiate suitable investment terms with the government. The government indicated it is not willing to continue the negotiation further, nor offer a sale of the asset to a prospective developer. The company has indicated it will take a $720 million charge in the second quarter of 2013, of which $20 million will be for cash severance and closure costs.

Opportunities

- The assumption on the street is that once the Fed starts tapering its QE program, the dollar will strengthen as real rates head up. Julien Garran, in his UBS Commodities and Mining Q&A, provided some insight into what really happened to the U.S. dollar in 1994, the last time we were in a similar situation. Back then, as the Fed hiked interest rates and real yields increased, the dollar should have rallied, but it fell instead and gave a boost to commodity prices. The reason was that despite a stronger-than-expected U.S. recovery, the European recovery surprised analysts, which triggered a currency move, thus selling off the dollar. This is particularly interesting today, as the ECB announced it would refrain from further monetary easing until further notice, a policy that surprised investors and led to a strengthening euro and weakening dollar this week.

click to enlarge

- On the same subject, the dollar continues to face the threat of negative real interest yields. Despite the assertion that real rates will continue to rise, we are of the opinion that the Fed is unlikely to allow further increases in government yields. The fiscal deficit needs to be financed, and the government cannot afford to refinance at higher yields than those of today. In addition, the natural trend of inflation will eventually force CPI numbers to escalate, which, rather than resulting in increasing real rates, would have the opposite effect of lowering real rates. This outcome should bode well for the commodities complex overall, but more strongly for gold, whose negative correlation with the dollar has been strengthening as of late.

- Pretium Resources released its Feasibility Study this week, confirming probable reserves of 6.6 million ounces at an average grate of 13.6 grams per ton. The valuation metrics look very positive, to the point where some analysts on the street are calling it “one of the best, if not the best, undeveloped gold project out there.” The next milestone will be details of the bulk sample which is expected in the fourth quarter of this year. This success validates our investment theory of supporting companies led by top managers, and developing rich resource bases.

Threats

- Paradigm Capital published a study on gold explorers and their expected lifetime based on their cash levels and current burn rates. On average, the companies studied have one year of cash burn remaining, something that has been worrying investors, given that a situation in which markets fail to improve, will see many of the explorers go dormant, bankrupt or be consolidated. However, Paradigm believes the sector will come back to life even if gold prices stabilize because the industry will adapt and reduce costs, signs of which should emerge fairly soon.

- On Ernst & Young’s “Business risks facing mining and metals 2013-2014” report, the company reports on a trend that has been evident on the stock pricing in the sector over the last few months: investors are pulling back from risky investments, namely junior explorers and developers. Instead, investors are seeking high-yielding, near-term opportunities, a style that has not favored gold mining stocks over the years. Fortunately, we have followed a dividend income approach over the years, which has helped avoid many of the extraordinary risks in the sector.

- A new amendment act has introduced a number of significant changes to South Africa’s mineral regulatory regime. The changes, signed into law by President Jacob Zuma, allow the Mines Minister to impose stricter conditions on mining rights where the land is occupied, which may go beyond the requirements of the Mining Charter. There could be further compliance and regulatory costs on the industry, according to Johannesburg-based law firm Webber Wentzel.

Energy and Natural Resources Market

click to enlarge

Strengths

- U.S. oil production grew at the fastest pace since BP started keeping records in 1965, because of unconventional sources such as shale and tight oil. An increase in output of about 1 million barrels a day caused net oil imports to the U.S. to drop by 930,000 barrels a day and imports are now 36 percent below their 2005 peak, BP said in its annual Statistical Review of World Energy this week. The expansion of both oil and natural gas production in the U.S. was the fastest in the world last year. The report highlights the potential scale of unconventional oil extraction.

- China's power consumption in May reached 426.9 billion kilowatt-hours (kWh), 5 percent higher than in the same period of 2012, the National Energy Administration (NEA) said on Friday. Total power consumption over the first five months reached 2.057 trillion kWh, up 4.9 percent compared with the same period a year earlier. Power consumption in China, the world's top energy user, is expected to grow more than 9 percent this year, faster than the 5.5-percent growth rate of 2012, the State Electricity Regulatory Commission (SERC) said in January.

Weaknesses

- The Energy Information Administration (EIA) lowered its forecast for U.S. gasoline demand for 2013 to the lowest level in 12 years. Gasoline consumption this year will average 8.66 million barrels a day, lower than the 8.68 million in last month’s projection and the lowest level since 2001, according to the agency’s monthly Short-Term Energy Outlook.

- Nymex natural gas futures fell 2.5 percent this week to settle at $3.74 per mmbtu as injections into storage were in line with estimates.

Opportunities

- Malaysian national oil company Petronas, says it expects to spend up to $16 billion to build a liquefied natural gas export facility in western Canada. Arif Mahmood, Petronas’ vice president of corporate planning, says the company will invest between $9 billion and $11 billion to construct two LNG liquefaction plants. Another $5 billion will be invested in a 750 kilometer-long pipeline, to be built by TransCanada Corp., to supply gas to the two plants, he said Tuesday in an email to The Associated Press. The Pacific Northwest LNG project, located on Lelu Island in the Port Edward district, will liquefy and export natural gas produced by Progress Energy Canada. Both companies are owned by Petronas, which secured its first LNG buyer, Japan Petroleum Exploration Co.

- Statoil predicts oil demand is expected to rise 0.5 percent per year to around 100 million barrels of oil per day by 2040, per a research report released by the Norwegian oil company. Statoil said that income growth and an increase in private transport in emerging economies were the most important factors contributing to higher oil demand growth. "Economic development will continue to drive energy demand, and energy is a prerequisite for economic growth," Statoil chief economist Eirik Wærness commented. The report predicted that annual global economic growth would continue on its current pattern of growth, with yearly growth averaging 2.8 percent over the next three decades. Emerging economies are expected to see 4.5 percent average annual growth with Organization for Economic Cooperation and Development (OECD) countries trailing at 1.9 p ercent. This economic growth will translate into global primary energy demand growth averaging 1.3 percent a year, or a total increase of 40 percent over the 27-year period, the in-house analysis said. Non-OECD countries are expected to account for the bulk of the energy demand rise, seeing demand growth of more than 60 percent by 2040.

Threats

- Changes to South Africa’s mining laws are likely to raise regulatory costs after amendments came into force last week, law firm Webber Wentzel said. The Mineral and Petroleum Resources Development Amendment Act (MPRDA) became effective June 7 after being signed into law by President Jacob Zuma. “The Amendment Act introduced a number of significant amendments to South Africa’s mineral regulatory regime,” the law firm said. “This is likely to impose further compliance and regulatory costs on the industry.” The changes stipulate that the mine’s minister must refuse an application for prospecting rights should those rights concentrate resources under the control one company, restricting “equitable access,” according to the law firm, which said the vague phrasing leaves the rule open to interpretation. The changes also allow the minister to impose stricter conditions on mining rights where the land is occupied, which may go beyond the requirements of the Mining Charter. The alterations, originally proposed in 2008, may be superseded by the Amendment Bill 2013, after it’s introduced to parliament later in June, Webber Wentzel said.

Emerging Markets

Strengths

- The rise in U.S. government bond yields that has threatened to reverse fund inflows into emerging markets is likely to prove as a red herring, according to BCA Research. With emerging market economies now surpassing 50 percent of world GDP, their higher savings rate will eventually cap any further increase in safe-haven bond yields. Although the higher savings rate does not fully eliminate the risk of weakening global growth, it does provide a floor for emerging market fund outflows.

click to enlarge

- Both the Chilean and Peruvian central banks left their benchmark rates unchanged this week. As commodity, export-driven economies both nations continue to face challenging external conditions amid weaker global demand. However, their domestic consumption growth continues to be resilient, and continues to support their expected economic growth levels for this year; 4.5 percent for Chile and 6.3 percent for Peru.

- Malaysia’s industrial production rose 4.7 percent year-over-year in April, more than three percentage points higher than expected and the first month-over-month increase since November, as demand from domestic infrastructure projects helped offset sluggish export growth.

- China’s inflation-adjusted retail sales growth accelerated to 12.1 percent in May, the fastest pace year-to-date, as the impact from the leadership’s anticorruption efforts was limited beyond catering, tobacco and liquor. Sales of gold, silver and other jewelry gained 38.4 percent in May from a year ago.

- Despite the past two weeks’ sell-off related to Federal Reserve tapering fears and a rebound in Japanese yen, the Philippines experienced the mildest foreign outflows within Southeast Asia and maintained a strong year-to-date inflow of $1.5 billion.

Weaknesses

- Russia and Brazil have seen the share of labor compensation as a percentage of GDP increase over the last decade, thus negatively impacting corporate earnings. It is worthwhile mentioning that most emerging markets have actually seen the share of labor income in GDP fall over the same period, giving way to higher corporate profits.

click to enlarge

- China’s new bank loans, aggregate financing, year-over-year growth rate of exports, imports, and industrial production in May, all came in lower than expected. Producer prices continue to deflate further, a clear reflection of anemic demand and an absence of government stimulus.

- The unemployment rate in the Philippines during April rose to a three-year high of 7.5 percent from 7.1 percent in March, while exports declined by a larger-than-expected 12.8 percent year-over-year in April, versus a 0.1 percent gain in March. Its central bank refrained from cutting interest rates given the recent sell-off in both Philippine equities and the Philippine peso

- Thailand, Indonesia and the Philippines recorded an aggregate $1.4 billion foreign outflow from equity funds last week. This is the highest weekly exodus since September 2011, or the height of the eurozone sovereign debt crisis.

- Homebuilders in Mexico continued to struggle this week. After multiple recent defaults on their debt, hopes were placed on favorable debt refinancing agreements with the syndicate banks. This week, Urbi, a real estate developer of low-income subsidized housing, failed to reach an agreement on its debt refinancing plans, casting doubt on the expected sector recovery.

Opportunities

- Worse-than-expected macroeconomic data, amid an apparently disrupted pro-growth government policy leaning in China, has again depressed Chinese equity valuations. Among the most reliable measures, price-to-book ratio has round-tripped back, approaching the lowest reading since the height of the eurozone debt crisis in October 2011. Historically, such cathartic cleansing was typically followed by a mean-reverting rally, and an overall 3.4 percent dividend yield, offering additional downside protection.

click to enlarge

- Continuing with the dividend yield theme, the recent commodity weakness and sell-off in emerging markets that depressed valuations now presents an opportunity for new entrants to invest in the upside optionality, earning a high dividend yield while waiting for stock market appreciation. Poland, Malaysia, Taiwan and Colombia, among others, all have dividend yields above 3 percent at the moment; significantly higher yields than U.S. government bonds. As a matter of fact, our Chief Investment Officer Frank Holmes recently wrote a piece on Why It Pays to Invest in Emerging Market Dividend-Payers.

- The leaders of Mexico’s main political parties announced that Parliament will hold two extraordinary sessions over the summer term to discuss pending projects. Among the projects to be discussed are the initial debates on President Pena Nieto’s long-awaited energy and fiscal reforms. Some doubts over Pena Nieto’s capacity to have the proposed reform bills passed by Parliament have been hovering over the Mexican market in recent weeks. The announcement on the reforms, which aim to boost investment and economic growth, should provide support to Mexican equities in the short and medium term, as well as increase the long-term upside.

Threats

- Despite Brazil’s effort to dismantle taxes previously imposed on foreign capital, which aimed to prevent an over-appreciation of the Brazilian real, the move could prove counterproductive in the short term. The loosening of capital controls is most likely to weaken the real, as both debt and equity investors sell emerging markets in favor of safer-haven investments. A short-term depreciation of the real could have upsetting consequences should inflation spike on higher import prices before imports can be substituted domestically.

- The Czech Prime Minister’s office is involved in a spying and bribery investigation, as one of his top aides and the head of military intelligence were arrested and charged on illegal spying and bribery accusations. Overnight on Thursday, police officers carried over 31 raids related to the investigation, seizing as much as $7.8 million in cash and gold. Prime Minister Necas has so far refused to resign despite opposition pressure. There is still little insight into the investigation; however, we view this as a serious threat to political stability in the country rather than a short-lived political dispute.

- Weak seasonality in Chinese manufacturing activity in the summer months, coupled with a dearth of material government policy action, may continue to weigh on investor sentiment in an otherwise frail market trading pattern for this time of year.

© US Global Investors