Bond Realities: The Changing Landscape for Fixed Income and the Death of the Agg'

Earlier this year Andrew A. Johnson, Neuberger Berman’s Chief Investment Officer for Investment Grade Fixed Income, led a series of discussions with institutional clients about the state of the fixed income market and key ideas in approaching opportunistic fixed income investing in the current environment. Here, Mr. Johnson has adapted, and elaborated on, the concepts described at those meetings.

In my 20-plus years as a portfolio manager, I’ve seen the death of the Barclays U.S. Aggregate Bond Index, affectionately known as the “Agg,” forecast no fewer than three times. This reminds me of a quote from one of my favorite American authors, Mark Twain, who said, “The reports of my death have been greatly exaggerated.” The same could be said of the Agg, a market-weighted amalgam of fixed income assets which at any given time reflects the strengths, weaknesses—and distortions—of the overall U.S. bond market.

The first instance was during the Clinton years when unexpected government budget surpluses led to a reduced amount of new Treasury bond issuance, leading some pundits to forecast that the Agg would be left consisting largely of corporate debt and mortgages— something that obviously did not come to pass. The second occasion was in the early 2000s, when, on the shoulders of the real estate bubble, there was concern that ramped up issuance of mortgage-backed securities would transition the Agg to a beast with negative convexity and a duration potentially ranging from 3 to 8 years—something that also did not come to pass.

That brings us to today’s market, where the ballooning U.S. federal budget deficit is fueling expectations that the Agg will become dominated by Treasuries—making it an index devoid of significant yield, the victim of multiple interest rate cuts and quantitative easing. The constant “remaking” of the Agg reflects the changing nature of issuance patterns. The Agg is often critiqued as reflecting the most indebted issuers. I will not join the debate concerning its stature as the default benchmark in this paper. Rather, I argue in favor of benchmark-agnostic (or unaware) opportunistic investing. The prevailing low yields and more normalized spreads make the current environment especially ripe for opportunistic portfolio management.

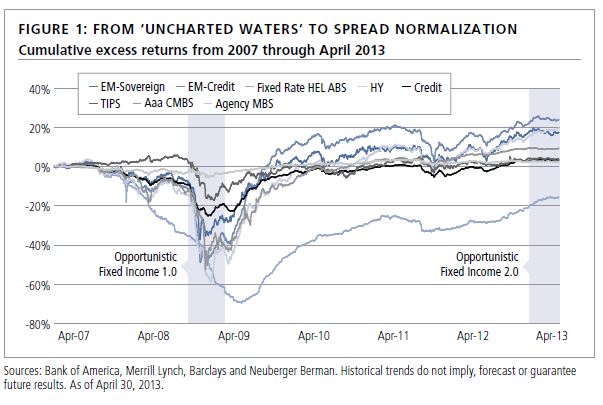

In many ways, the nature of what it means to be opportunistic has changed dramatically over time. Looking back at recent market stresses, the last distinct period of opportunistic investing, which I will call Opportunistic 1.0, was a byproduct of the financial crisis of 2008, when we witnessed extraordinary dislocation across the spread sectors. During that period, despite the climate of fear and illiquidity, in hindsight choices were fairly straightforward: Once you determined that the world was not plummeting into a global depression, opportunistic investing was essentially about harvesting excessive crisis risk premiums from the market. This essentially became a decision as to how much beta to have, and that decision was a function of your risk tolerance. In retrospect, where you chose to acquire your beta was much less important than the decision of how much beta to have.

Today, the environment is clearly different. Spreads have largely normalized. This new period, which I will refer to as Opportunistic 2.0, is characterized by fixed income markets that are no longer “screamingly cheap,” and in most cases are close to, if not fairly priced, relative to historical norms. Spread normalization combined with low absolute yields has created a huge challenge for investors: how to get an attractive risk-adjusted return in today’s fixed income market?

Now, more than ever, multiple tactics are needed to succeed in managing fixed income portfolios. While it is always beneficial for a manager to make smart sector allocations and timely duration decisions, we believe that this market in particular requires an expanded toolkit. For the right manager, this expanded toolkit should provide the resources to expand the duration band (potentially to allow negative duration), introduce pure alpha strategies and allocate to non-traditional fixed income asset classes. Based upon where we are in the current market cycle, you must think creatively and draw from more areas of the markets to capitalize on the opportunities that do exist.

Key Choices in Today’s Market

Impact of Benchmark

Among all the decisions an investor must make when it comes to opportunistic fixed income, I think that the choice of benchmark is significant, due to the constraints the choice of a benchmark places on an opportunistic manager in his or her quest for attractive absolute returns. Historically speaking, the choice of a benchmark has been based on many factors such as the return bogie clients wished to achieve, their liability structure, risk tolerance, etc. Within the current Opportunistic 2.0 environment, we feel that truly unconstrained opportunistic investing implies no benchmark. In my opinion, mandates are better designed by establishing clear return goals with a specific risk budget. That said an investor in opportunistic fixed income might desire a benchmark that establishes the neutral duration of the portfolio based on their specific needs.

For example, let’s suggest a scenario where your opportunistic fixed income manager has no opinion on the direction of interest rates or holds a very uncertain or weak view. With cash as a benchmark, you would expect the manager to maintain portfolio duration at or close to zero. On the other hand, if the same manager is given the Barclays U.S. Aggregate Bond Index as the benchmark, you would expect a portfolio reflecting no opinion or a weak view on the direction of interest rates to have duration within shooting distance of the benchmark. Even if the mandate allows for significant tracking error, the benchmark choice will likely anchor the manager as he or she wrestles with what a neutral duration position should look like. Alternatively, a truly unconstrained manager will arrive at a portfolio duration that is entirely driven by his or her assessment of the risk and return tradeoffs across the yield curve.

Risk and Return Objectives: Two Sides of the Same Coin

Given the unconstrained nature of true opportunistic mandates, we feel that setting return objectives and a risk budget with your manager is of critical importance. At my firm, we follow the fairly basic principle that risk and return must be consistent and reasonable in relation to one another. In that context, we think aspiring to an ex-ante information ratio (IR) of between 0.6 and 0.8 is reasonable. To achieve this, you either need to set risk or return. The natural inclination is to start with a return bogie, and, once that is established, the level of risk falls out as a function of the assumed IR.

While keeping an eye on tail risk is important in virtually any bond portfolio, it’s particularly important in an opportunistic portfolio, because by its nature, you are asking the manager to utilize asset classes with “fatter” tails. A key benefit of unconstrained mandates is that they provide potential for greater yield and return. That said, it’s important to understand that using this expanded toolkit requires a wider breadth of knowledge of the markets and sectors involved. This can represent a challenge for some managers that lack the size or scope to follow these markets.

A robust data set is required to estimate tail risk but sometimes the available information is not enough. An example would be what we learned from the financial crisis of 2008 – 2009, when what we affectionately call “toddler” asset classes such as non-agency RMBS showed their tails for the first time. Up until this period, the true risk and return properties of these asset classes were thought to be clearly understood. Without the benefit of performance histories that spanned a market cycle and included financial stress, however, it was all too common for managers to underestimate the risks inherent in these sectors. For toddler asset classes, some assumptions about the nature of the tails must be imposed upon the data.

Once armed with information—or at least assumptions—about tail risk, the next step is to manage it. Pension plans often consider how much they can afford to lose and how long it will take to recoup any loss. We use a rule of thumb that seeks to avoid tail risks implying losses that would exceed 2.5 years to recover as our starting point for an unconstrained mandate discussion. And, in our opinion, a red flag should go up if a manager suggests it’s possible to generate attractive returns and hedge tail risk completely. Such unanticipated risk comes with the territory—it can be anticipated and managed, but it won’t disappear.

Gauging The Opportunity

In terms of the fixed income opportunity set mentioned above, we believe that casting a wide net and allowing a manager to capitalize on the diversification and return benefits of all market sectors is critical. Within the confines of an investor’s return and risk decisions, the portfolio manager is free to evaluate opportunities in asset classes that might not ordinarily be included in a traditional portfolio. But how should managers go about finding opportunities with their expanded toolkit?

Our team considers three main questions in seeking to capitalize on mispricings in the bond market which we think are broadly useful in the management of an unconstrained mandate.

- What are the market’s expectations?

- Where do we have investment insight?

- How confident are we in our views?

The answer to the first question provides context; i.e., what is the market’s view of the asset classes’ risk/reward tradeoff. As for the second question, we compare and contrast our insight and opinion, analyzing where we have a differentiated view versus the market consensus. Finally, the third question requires us to measure the level of conviction that we have in our views, which in turn determines whether or not a view is actually implemented in a portfolio and how much of our risk budget we are willing to commit. In our opinion, it is imperative to understand how a manager arrives at their confidence level when making allocation decisions. Ensuring that a manager has a systematic approach to all three questions should be an important part of your selection process when granting opportunistic fixed income mandates.

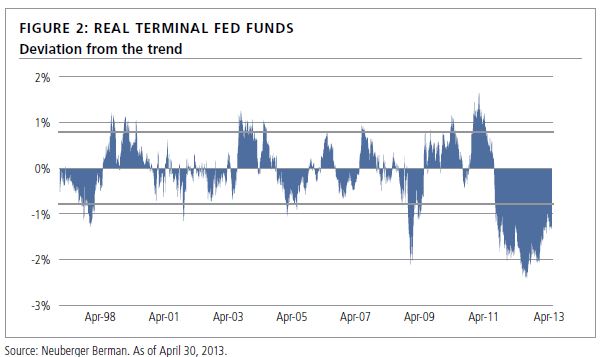

By way of example, let’s focus on rates for a moment, since a manager’s view on the subject, both in terms of direction and the rate of change, can have enormous implications for a portfolio’s return. As seen in the figure below, the real terminal Fed Funds rate fluctuates around an equilibrium rate, but is mean reverting. Historically, we have found opportunities when there are rate movements outside of one standard deviation. Making duration decisions when outliers occur may not guarantee success, but it does tend to improve the potential to add value.

While short-term interest rates are currently at or near historic low levels, the Federal Reserve will eventually need to reverse quantitative easing (one impact has been the large deviation in the figure above), which would likely have a negative impact on some fixed income sectors. Should rates rise at a pace somewhat greater than what appears to be priced by the market, we believe the ramifications will likely be modestly negative for the broad market over a one-year horizon—or far less severe than people fear. However, if rates were to rise materially sooner and at a much more rapid pace than currently priced, U.S. Treasuries would experience more negative returns (in our view, on the order of

-3% to -5%) over a one-year horizon. Ultimately, prospective returns of U.S. Treasuries and the broader investment-grade market, by extension, will be governed by the timing and pace of changes in Federal Reserve policy.

New Environment, New Approaches

From our perspective, there are exciting options for investors in the fixed income market. Opportunistic mandates can provide a real opportunity for investors’ fixed income portfolios. In our view, the keys to success will be in the approach and tools that managers choose to employ in seeking risk-adjusted returns. Investors may benefit from using managers that focus on the expanded toolkit described above. In order to effectively execute an opportunistic portfolio, investors and managers must maintain a clear focus on both the risk and return tradeoff and the implications of tail risk. Finally, it is important that investors understand the means by which a manager establishes and implements their investment views, ensuring that they employ a consistent and disciplined portfolio construction process.

This material is provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole. Neuberger Berman products and services may not be available in all jurisdictions or to all client types.

Investing entails risks, including possible loss of principal. Investments in hedge funds and private equity are speculative and involve a higher degree of risk than more traditional investments. Investments in hedge funds and private equity are intended for sophisticated investors only. Indexes are unmanaged and are not available for direct investment. Past performance is no guarantee of future results.

This material has been issued for use by the following entities; in the U.S. and Canada by Neuberger Berman LLC, a U.S. registered investment advisor and broker-dealer and member FINRA/SIPC; in Europe, Latin America and the Middle East by Neuberger Berman Europe Limited, which is authorised and regulated by the UK Financial Conduct Authority and is registered in England and Wales, Lansdowne House, 57 Berkeley Square, London, W1J 6ER; in Australia by Neuberger Berman Australia Pty Ltd (ACN 146 033 801, AFS Licence No. 391401), which is licensed and regulated by the Australian Securities and Investments Commission to deal in, and to provide financial product advice for, certain financial products to wholesale clients; in Hong Kong by Neuberger Berman Asia Limited, which is licensed and regulated by the Hong Kong Securities and Futures Commission;

in Singapore by Neuberger Berman Singapore Pte. Limited (Company No. 200821844K), which currently operates under an exemption from licensing under the Financial Advisers Act (Chapter 110) of Singapore for marketing of collective investment schemes to institutional investors; in Taiwan by Neuberger Berman Taiwan Limited, which is licensed and regulated by the Financial Services Commission (“FSC”) to deal with specific professional investors or financial institutions, for internal use only, and which is a separate entity and independently operated business, with SFB operating licence no.:(101) FSC SICE no.008, and address at: 10F, No. 1, Songzhi Road, Taipei, Telephone number: (02) 87268280; and in Japan and Korea by Neuberger Berman East Asia Limited, which is authorized and regulated by the Financial Services Agency of Japan and the Financial Services Commission of Republic of Korea, respectively (please visit https://www.nb.com/Japan/risk.html for additional disclosure items required under the Financial Instruments and Exchange Act of Japan). Except for the foregoing, this material is not intended for use or distribution within or aimed at the residents of any other country or jurisdiction. This document is not an advertisement and is not intended for public use or additional distribution in the following jurisdictions: Brunei, Thailand, Malaysia and China.

The “Neuberger Berman” name and logo are registered service marks of Neuberger Berman Group LLC. N0157 05/13 © 2013 Neuberger Berman LLC. All rights reserved.

© Neuberger Berman