The last few weeks have seen volatility emerge as concerns about the Fed’s policy of quantitative easing and the timing of changing it have taken center stage.

While there has been quite a bit of mindless blather concerning theFed’sbond purchases, the net result is that the economy and outlook for actual interest rates have remained unchanged. As a result stock prices had a little bump down,but have regained their footing.

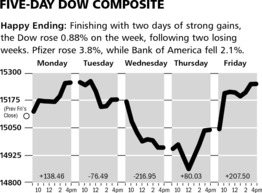

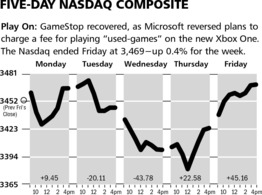

As the charts above illustrate, Friday’s employment data was good enough, (but hardly good) to restore confidence that the economy was not growing fast enough to cause a sudden change in Fed policy - which in my view has always been absurd but good enough so that economic bears had to throw in their towel as well.

As a result, the Dow Jones Industrial Average gained nearly a full percent while the NASDAQ Composite was higher by .38% despite big declines earlier in the week.

The Markets & Economy

All of this discussion about the Fed and its potential to “taper” (don’t you just love this new phrase) its quantitative easing policy is a joke and misses the point entirely. The real question is why/whether they should have started down this road to begin with. Trillions of dollars of assets have moved to the Fed’s balance sheet, and what has been accomplished in the real economy? Very little, is the answer.

Without having accomplished anything substantial, except creating either actual dependence or the perceived dependence by the financial markets on this policy, the debate is all about “tapering”. This is the equivalent of a country declaring victory and removing itself from the battlefield despite the facts on the ground.

I say this because our US economy, which is doing the best in the world, is still suffering. Last Friday the government reported that unemployment increased to 7.6%. In my view this number will be over 8% by the end of the year. At the same time the number of jobs in this country is still several million below the number in 2007, despite population gain and immigration. Record numbers of Americans are on various government transfer payment programs. Last week it was officially estimated that 49% of American families are receiving some sort of aid from the government sector. This friends is not a safety netpolicy for our society. It is a fancy way of creating a new and unsustainable way of life for our society.

The task for policy makers in Washington DC is to find policies which put people to work and, not put people on government support programs which all too often become a way of life. Until this happens, our economy will barely keep its head above zero percent growth if that. This scenario is most likely given the present set of economic policies and is about all we can hope for and we are lucky to be experiencing this.

Many exciting things, of course, are serving as a source of growth in the economy:

- America’s burgeoning energy independence is truly a story with legs with very positive long-term implications.

- At the same time our country’s status as having the reserve currency in the global economy allows us to finance our deficits easily (which are shrinking in the short-term), thus putting off the day of reckoning.

Just this morning S&P raised its rating on the sovereign debt of the USA to “ stable”. To the skeptics it might seem they did this due to pressure from the various investigations into their ratings moves during the real estate bubble, but it is a positive as far as it goes. Although perversely, this might cause concern that the Fed should taper sooner rather than later.

All in all,

- the US is the best economy in a lousy global market, and

- the US currency is the best fiat money in the world, and

- the US market is still a safe haven as witnessed by Japan’s nearly 20% correction over the past few weeks (until last night).

Thus our portfolios continue to ride out these storms and our cash holdings position us to take advantage of swoons as they most certainly will occur.

What to Expect This Week

The action is packed in towards the end of the week. That is when retail sales and industrial production will be revealed for May. In addition, more inflation (or is it deflation?) data will be announced.

Nothing is likely to change the scenario to the 2% +/- GDP

growth rate we have been in for a long time.

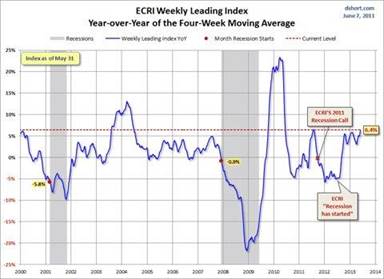

The weekly read from the Economic Cycle Research Institute (see chart below) has not changed in a long time. They still think we are in a recession, but I do believe it would take a shock to create that. Fed policy will be much discussed but little will change for many months, and that along with Europe breaking apart are the two most likely things which would pressure the stock market for the rest of 2013.

![]()

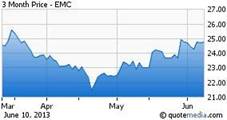

SYMBOL: EMC

Three Month Chart

EMC Corporation sailed through the market’s recent correction because the Company has at long last decided to engage in a little financial engineering, which we have discussed so often over the recent years. The Company initiated its first ever dividendfor shareholders of ten cents quarterly beginning next month, and at the same time raised its stock buyback to a stunning six billion dollars, which is over 10% of the Company’s entire market capitalization. EMC is inexpensive on an earnings basis despite being a leader in the Cloud computing segment of the Information Technology sector.

Smartphones, tablets and such are relying more and more on the Cloud and EMC is a value way of playing this trend, which will last for a long time. We like EMC here.

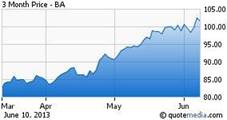

SYMBOL: BA

Three-Month Chart

Shares in Boeing have continued their advance since the Dreamliner problems have been dealt with. We have seen many increases in price targets for the shares with most of them now in the $120 to $125 range. Beyond that the Company has also committed to returning capital to its shareholders, and this means increasing dividends in the years to come.

One thing for sure, Boeing is a company for which there is little true competition (just one other global player). In the years to come, despite all of the various concerns expressed here and elsewhere, the increasing global population needs to travel. Shares in Boeing, while having recovered substantially, represent a fundamental safe haven in this crazy world, short of a world war, which diminishes the desire people have to see the world.

© McIntyre, Freedman & Flynn