Stocks Climb Amid Mixed Data

Equity markets crawled higher last week amid a mixed week of economic data, with the S&P 500 rising 0.8% and the DJIA gaining 0.9%. Performance was choppy, with the market selling off Tuesday and Wednesday, only to rebound sharply on the final days of the week. In the wake of a positively received government jobs report on Friday, the Dow posted its second highest gain of 2013.

The Federal Reserve released its Beige Book last week, which synthesizes economic and market information from around the country. Market participants scrutinize this document due to its influence on the Fed’s thinking. The latest report revealed a slightly weaker assessment of the US economy, with the characterization as “modest to moderate recovery” instead of the “moderate recovery” in the previous edition.

The Beige Book did identify a few bright spots in the economy, notably real estate and construction. The survey indicated employment remains a stubborn component of the economy.

Manufacturing has emerged as a clear source of softness in the US economy. On Monday, the Institute of Supply Management (ISM) released its monthly diffusion index that evaluates the health of the manufacturing sector. May’s reading disappointed consensus expectations by two points, falling into contractionary territory at 49.0.

Unfortunately, Monday’s ISM report revealed a sector that is experiencing a broad-scale slowdown. New orders sank 3.5 points to 48.8, production contracted at 48.6, and employment remained stagnant near the 50-level. Monday’s report mirrors other important manufacturing measures such as the regional Federal Reserve surveys that have deteriorated recently.

Encouragingly, however, ISM reported that its measure of service sector activity strengthened in May to 53.7. Given the greater prominence of service related industries in the US economy, ISM’s less heralded indicator is arguably more important. The most recent report was bolstered by gains in business activity/production and new orders, which spell continued momentum for the sector. The survey noted that while a majority of respondents are optimistic about business conditions, they remain uncertain about the long-term outlook.

The week’s economic data was headlined by the May government jobs report on Friday. At 175,000, the nonfarm payroll survey came in right in line with expectations. This “goldilocks” figure, as the Wall Street Journal termed it, was well received by investors for not being so strong as to threaten a “tapering” of Fed policy, but also not too weak to signal a slowdown in the economy.

Prior months’ revisions were essentially a wash, with April revised lower by 16,000 and March revised up 4,000. Among the report’s components in May, private service sector jobs generated the biggest gains with the addition of 179,000 jobs. This was concentrated in professional & business services, leisure & hospitality, retail trade, and education.

On the unemployment front, the headline rate ticked up one tenth to 7.6%. This increase was primarily attributable to a 420,000 increase in the labor force. The denominator in the unemployment equation has led to month-to-month volatility in the unemployment rate in recent months.

Overall, the household survey data revealed little material change from the prior month. The underemployment rate, which adds in discouraged workers and part-time workers who wish to be full time, dropped one tenth to 13.8%.

Risk parity – new thinking or new packaging?

Ever since Harry Markowitz brought forth the notion of mean-variance optimization in 1952, academics and practitioners alike have sought ways to build more robust asset allocation methodologies. Recently, the most talked about approach in the institutional world is risk parity, which seeks to focus on risk as its primary input. Risk parity is intuitively appealing, but suffers many pitfalls that investors need to consider.

In its simplest form, risk parity advocates diversifying portfolios by risk, as opposed to by dollars. For investors, that translates into a portfolio that equally weights each asset class by volatility.

Risk parity was brought to the forefront by firms such as Bridgewater Associates, with the idea being that traditional methods of asset allocation were inadequate. For example, a portfolio that allocates 60% to equities and 40% to bonds actually derives more than 90% of its risk from the equity component.

Source: Invesco

To satisfy the shortcomings of stock/bond portfolios, professional investors began to look at portfolios from the perspective of risk. The resulting portfolio typically increases exposure to “lower volatility” asset classes such as fixed income, while reducing exposure to equities. Normalizing the volatility of a risk parity portfolio relative to a 60/40 portfolio requires leverage on lower volatility assets such as bonds.

Source: JP Morgan Asset Management

The empirical results have been attractive to date. From 1971 through the end of 2012, a risk parity portfolio targeting a 10% volatility delivered a 10.4% return versus an 8.7% return for a 60/40 portfolio.

Source: Reddington

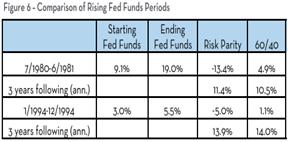

Critics of risk parity argue the period of secularly declining interest rates for the past 30+ years acted as a significant tailwind to risk parity portfolios, particularly given the application of leverage to lower volatility assets.

Leverage is not a bad thing, if managed appropriately, but it can cause problems during periods of shock or unexpected performance. Research from NEPC demonstrates that in the early 80s and again during the mid-90s, we did encounter brief periods of rising interest rates. At those points, risk parity portfolios began to lag 60/40 portfolios by a reasonably wide margin.

Source: NEPC

Risk parity holds a certain amount of intuitive appeal, as mean-variance optimized portfolios require three inputs – risk, correlations, and return. Risk parity portfolios only require an input for risk, thereby minimizing user error at the input stage of the process. Limiting input risk is one of the biggest selling points for risk parity portfolios.

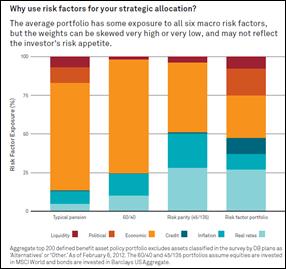

Investors in the retail and institutional world continue devoting more time and resources to risk parity methodologies. Going forward, there is likely to be increasing interest in the approach and further research into newer, more sophisticated ways of thinking. Already, a number of asset managers are moving beyond risk parity, towards risk factor investing. What risk parity ignores is the principal that multiple risks define the returns for a given asset class, and similar risk factors may permeate a number of asset classes. If those risk factors are viewed under an aggregate lens in the risk parity framework, the resulting portfolio may not be as diversified as one is originally led to believe.

Source: Blackrock

Ultimately, while the “risk” in risk parity is represented by volatility or standard deviation, that does not account for actual risk, or the permanent impairment of capital. New asset allocation approaches are accounting for a growing number of risk factors and everyday investors are benefitting from that dialogue. Risk parity is a step in the right direction, but it hardly represents the investment panacea so many desire.

Bloomberg said it best recently when they stated, “While the press today is filled with stories about the popularity of this strategy it is probably just a matter of time before poor performance makes risk parity yet another failed savior.”

the week ahead

A few important economic data points are on tap for this week. Those include retail sales, industrial production, and the NFIB’s Small Business Optimism survey. Additionally, a spate of Chinese economic data is released on Sunday before the week starts which could influence markets.

Other important events this week include a German court’s ruling on the constitutionality of the OMT program (the backstop put into place by the ECB which has calmed financial market fears in Europe), as well as a meeting of the Bank of Japan. Some observers believe the BoJ may enact new measures to mitigate volatility in its government bond markets.

Other central banks meeting this week include Russia, New Zealand, Indonesia, South Korea, the Philippines, Chile, and Peru. No policy changes are expected from that group

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

For more information, please visit our website at http://www.Fortigent.com.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent