May Flowers Bring Best Equity Market Since 1997 as Bonds Wilt

Executive Summary

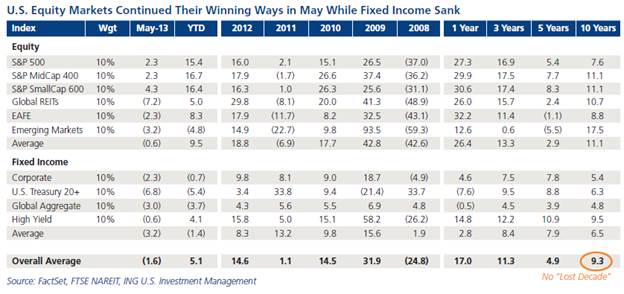

- The S&P 500 has opened 2013 with its best year-through-May return since 1997. U.S. Treasury prices, in contrast, plunged last month on talks of Fed “tapering”.

- Don’t expect the reflation in bond yields to continue in the near term, as the Fed continues to struggle in its current war against deflation.

- Fundamental business activity — not quantitative easing — is the wellspring of sustained economic growth, creating lasting sales and profits.

- For investors, the two biggest self-defeating fears continue to be 1) the fear of buying equities and 2) the fear of buying bonds.

May flowers usually follow April showers, but the markets have enjoyed nothing but blue skies for the past seven months. The S&P 500 Index has not had a down month since last October and has posted its best year-to-date return through May since 1997. The blue sky for equities contrasts with the storm that swept through the U.S. Treasury bond market, which plunged nearly 7% in May.

Investors can’t have it both ways — bond yields can’t stay low forever while equity markets respond to “green shoots” of economic growth. The best-case scenario for the economy is that equity markets rise — as they have been — and bond yields go back up to normal, as they have not done since the credit crisis five years ago. Is now the time we get back to normal? If so, what does it mean for stocks and bonds?

Will QE Go on Forever?

The mere mention of “tapering” the current quantitative easing (QE) program, which could be found only by scouring the depths of the Fed minutes, sent Treasury yields soaring in recent weeks. Improvements in employment, housing and GDP growth likely prompted the Fed to at least discuss moderating its extraordinary monetary stimulus.

Despite the effects of coordinated global monetary stimulus, the cornerstone of our Global Perspectives philosophy — fundamentals drive the markets — ultimately remains unshakable. Accordingly, “printing money” — a pejorative if not precise label for “quantitative easing” — simply is not and never will be a sustainable strategy. QE is a temporary shock intended to stimulate economic growth in the short term, whereas entrepreneurial risk-taking creates the lasting sales and profits that are the wellspring of the economy. Fundamental business activity is the sustainable market force.

At the end of May markets got a taste of what an initial rise in bond yields will mean.

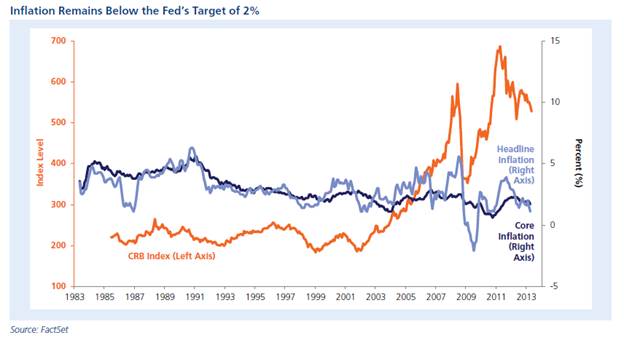

The ten-year Treasury yield ended the month at the year’s high of 2.20%. The rise in yields precipitated a sharp hit to bond prices and overall negative returns, raising fears of a repeat of 1994 when aggressive Fed action wreaked havoc in the bond market, unfortunately at a time of substantial risk taking in fixed income. On top of the swoon in bond prices, high-income assets such as REITs also got whacked in May. So should we now expect a pronounced surge in yields and a corresponding adverse impact to bond returns? Certainly not, if current inflation readings relative to the Fed’s 2% target are any indication, because it actually looks like the Fed is failing in this mandate. For example:

- The consumer price index in April increased only 1.1% year over year.

- The personal consumption expenditure price index — the Fed’s preferred measure of inflation — dropped 0.3% in April after being down 0.1% in March, and is only up 0.74% year over year.

- Wholesale prices, as reflected by the producer price index, declined 0.7% in April and are up only 0.7% year over year.

The Fed has explicitly disclosed the measures that will prompt the tapering of its asset-purchase program — namely, maintaining an inflation level of 2% while reducing the unemployment rate to 6.5%. We are not there yet, but there are good signs. Keep in mind that the U.S. is not an island; for our economy to grow, global markets must grow as well. Results here are also mixed, but positive signs are evident.

Market Fundamentals

Since the wind down of the Fed’s extraordinary support measures depends on fundamentals, let’s revisit our ABCDs, beginning with the first and most important factor.

Advancing earnings growth. First quarter earnings season is coming to a close, and U.S. corporations have once again surprised on the upside. Defying expectations of slightly negative growth (which were later ratcheted up to 2.1% at the start of reporting season), earnings have grown 3.3% in the first quarter of 2013 over the first quarter of 2012. Financial companies once again led the way in earnings growth, at 11.2%, with defensive stocks in the telecom and utilities sectors also showing strong profit growth.

Broadening manufacturing. Despite the tailwind of cheap natural gas, manufacturing stumbled in May, with the ISM Manufacturing Index posting its lowest reading since June 2009 at 49.0. While regional indexes were wildly divergent, the overall trend in manufacturing could be best described as flat and pensive. This is a concern because last summer when manufacturing went below 50, earnings subsequently went negative for the third quarter. It was true then and is true now that global growth is faltering due to the impact of Europe in recession, China slowing, and the U.S. at subpar growth. Recall it was that at that point, September 2012, when ECB president Mario Draghi pledged “outright monetary transaction” and Fed Chairman Bernanke initiated $40 billion per month of stimulus, which was expanded to $85 billion later in the year.

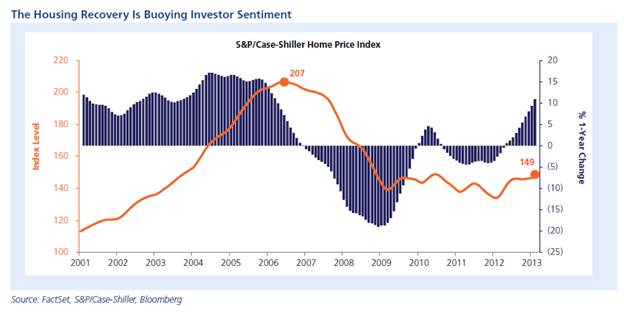

Consumer as the game changer. Consumer spending remains a bright spot in the economy. Consumer confidence surged to a five-year high in May. And why not? The S&P 500 is up more than 15% this year, interest rates remain low thanks to the Fed, and the housing market recovery is looking better every month.

- The S&P/Case-Shiller home price index shot up 10.2% in the first quarter of 2013 over 2012, with all regions of the country reporting gains.

- Pending home sales for April reached three-year highs, indicating strong housing demand.

- The year-over-year rise in home prices has added $1 trillion to homeowners’ net worth.

- Retail sales are up 3.6% over a year ago, not surprisingly, as consumers are feathering their nests with appliances, furniture, garden accessories and new cars in the driveway (auto sales are up 10.2% over last year).

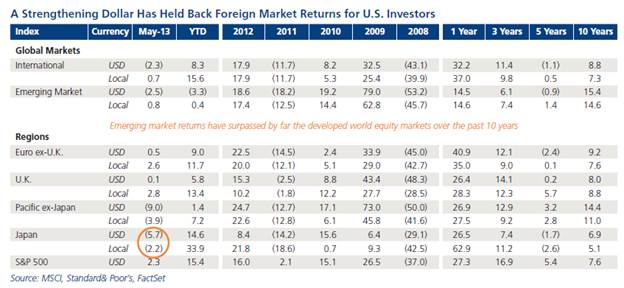

Developing Markets. Overall, emerging markets have been hammered this year, and both the global equity and bond markets have seen outflows in funds as U.S. equity markets have surged and U.S. bond yields have ticked up. The headlines are abuzz with China’s under-reported debt-to-GDP burden (stemming from rampant government spending in an effort to juice growth) as well as news that the expected recovery in Brazil has stubbornly refused to materialize. However, investors who look beyond the noise will find that expected growth opportunities are still higher in developing countries than in the developed nations.

Global Growth for Sustainable Markets

Global growth is a function of each country’s economic activity and free trade throughout the world. So just how strong is global growth?

- In the U.S., first quarter GDP growth was a respectable 2.4%.

- In Japan, first quarter GDP growth surprised the markets at a robust 3.5%.

- Europe has continued to go from bad to worse, with recession spreading throughout the region.

- In China, both achieved and expected growth has been ratcheted down.

- Organization for Economic Co-operation and Development (OECD) growth estimates for its membership were revised down to 3.4% and 4.3% for 2013 and 2014, respectively.

- Non-OECD growth is expected to be 5.4% and 6.5% for 2013 and 2014, respectively.

The OECD is composed mostly of developed markets, but Mexico, Turkey, Chile and South Korea, to name a few, are also in the mix; non-OECD countries consist of emerging and frontier markets. Obviously, to the extent global growth is on track, it’s the less-developed markets that are leading the way.

So investors should keep an eye on the frontier markets — like the PIVOT countries (Peru, Indonesia, Vietnam, Oman and Turkey) — as sustainable drivers of future growth. Our PIVOT acronym is not meant to supplant the BRICs (Brazil, Russia, India and China) but rather to encourage investors to look far and wide for growth and opportunity. Although growth in these countries has not been immune to the global slowdown, it is far stronger than the latest U.S. GDP reading.

- Peru’s first quarter growth declined to a still-high 4.8%, primarily due to a softening of industrial metals prices.

- Indonesia just posted its tenth straight quarter of growth above 6%.

- Vietnam’s 2013 forecast was reduced by the IMF to 5.2% as the country struggles to implement banking reforms.

- Oman’s nominal annual GDP growth exceeds 22%; it is investing in infrastructure and aggressively seeking foreign investment to diversify away from the oil industry.

- Turkey, despite recent widespread protests and unrest, is still the fastest-growing economy in Europe, expanding at 5.1%.

Fear, not Volatility, Destroys Returns

For investors, the two biggest self-defeating fears continue to be:

- The fear of buying equities

- The fear of buying bonds

The litany of excuses for not investing would fill Noah’s ark, but those who remained on the sidelines since the recession ended four years ago have paid dearly. The fear of equities is usually derived from a false belief that the market is overvalued and due for a correction. But the consensus forecast for S&P 500 earnings is $110, which equates to a price/earnings multiple of 15 — about the historical norm. Valuations near normal suggest normal volatility but not sharp corrections. The fear of buying bonds has been rooted in an inexplicable fear of inflation, which has been and continues to be flat wrong. Although May was a tough month for bonds, what has changed in the economy to warrant a fear of inflation? Nothing, especially since the Fed’s current war against deflation has generated mixed results at best.

The only way to build wealth is to accept normal volatility. Without question, putting all the eggs in one basket would be a serious mistake. A well-diversified portfolio encompassing a broad range of risky assets is not only sound investment theory, it is the practical, prudent way to go.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 6611