“Those who have knowledge don’t predict. Those who predict don’t have knowledge.”

Lao Tzu, Chinese philosopher, 6th century BC

Several years ago, off-duty airline pilot Robert Thompson walked into a convenience store somewhere in the United States; however, having just entered the store, he turned around and left again without buying anything because, as he would later testify, something about the place spooked him. Was it the customer wearing a heavy jacket despite the hot weather? Maybe the shop assistant’s intense focus on the customer in the jacket? Or was it the single car in the parking lot with the engine running? Whatever drove him to walk out of there, Thompson’s decision was the right one. Shortly after he left the store, a police officer walked straight in to an armed robbery and was shot and killed. Thompson did not realise it at the time, but his reaction came instantly and instinctively, way before he became cognisant of the potential danger.

Now, go back some 80 years to March 1933 when unemployment in the United States was reaching an all-time high. Thousands of banks had failed in previous months. Bread lines stretched around entire blocks in many cities across the country. Against this depressing backdrop, Roosevelt was about to deliver his first address to the American people. The newly elected President began his speech not by discussing economic conditions but with a powerful observation that still resonates today:

“So, first of all, let me assert my firm belief that the only thing we have to fear is fear itself - nameless, unreasoning, unjustified terror which paralyzes needed efforts to convert retreat into advance”.1

Fear impacts our behavioural patterns, whether consciously or subconsciously. If someone threatens us with a knife, the instinctive reaction will be to take flight. If the stock market falls 20% in a single day, we will tend to react in very much the same way, even if the threat is not physical.

Fear, like greed, makes people, and that would include investors, behave irrationally. You may argue that physical threats cannot be compared to financial threats and, in some respects, they cannot, but research into the human brain suggests that it is the same part of the brain that kicks into action in both instances.

The Efficient Markets Hypothesis

I trained as an economist in the late 1970s and early 1980s and was indoctrinated to believe in Modern Portfolio Theory (MPT), the Capital Asset Pricing Model and, over and above all else, the Efficient Markets Hypothesis (EMH). I wasn’t alone. Millions of students all over the world have been taught the same since the 1960s and they still are.

MPT is based on a number of assumptions, some of which are more restrictive than others. For example, it is assumed that the relationship between risk and returns is linear and that it is static, not only over time but also under varying market conditions. It is also assumed that investors behave rationally at all times. Last, but not least, returns are assumed to be stationary (normally distributed) and markets are assumed to be efficient. In this type of world, alpha doesn’t exist.

Obviously, if you want to pick a fight, each of those assumptions can be challenged, but that’s not the point. The real question is whether the sum of those assumptions is so far off the mark that it renders the entire theory absolutely useless. Effectively the question is whether EMH, and with it MPT, should be ditched altogether.

Behavioural economists take a different view

The battle lines between believers and non-believers have been drawn for years. Supporters of EMH say that while behavioural biases most certainly exist in the real world, they are of limited relevance because markets will tend to arbitrage those inefficiencies out very quickly. Opponents of EMH argue that those biases are systemic and have an ongoing, significant effect on markets, because investors suffer from over-confidence and other biases. One group of opponents – behavioural economists – are known for taking a particularly dim view of EMH.

James Montier, one of the best known proponents of behavioural finance, wrote a now famous paper back in 2005 called Seven Sins of Fund Management – A Behavioural Critique. In his paper he asked an interesting question: Given the overwhelming evidence that investors are simply awful at predicting the future, why does forecasting play such a pivotal role in the investment process? He provided a plausible explanation himself:

“In part the obsession with forecasts probably stems from the ingrained love of efficient markets. It might seem odd to talk of efficient markets and active managers in the same sentence, but the behaviour of many market participants is actually consistent with market efficiency [EMH]. That is, many investors believe they need to know more than everyone else to outperform. This is consistent with EMH because the only way to beat an efficient market is to know something that isn’t in the price (i.e. non public information). One way of knowing more is to be able to forecast the future better than everyone else.”

Not resting on his laurels, James went on to provide an explanation as to why we get it so horribly wrong most of the time. He believes it is due to a phenomenon psychologists call ‘ anchoring’ and did a simple study to demonstrate how it affects decisions by asking his fund manager clients to write down the last four digits of their telephone number. He then asked them whether the number of doctors in their capital city is higher or lower than the last four digits of their telephone number, before finally asking them for their best guess as to the actual number of doctors in their capital city. Those with the last four digits of their phone number greater than 7,000 reported an average of 6,762 doctors, whilst those with telephone numbers below 2000 arrived at an average 2,270 doctors.

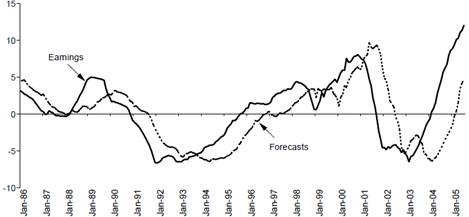

The conclusion is straightforward. When faced with the unknown, people (in this case, fund managers) will use whatever information they can get hold of. Hence we shouldn’t really be surprised that fund managers extrapolate current earnings trends when forecasting future earnings, despite the evidence that it is a futile exercise. In his paper James Montier provided powerful evidence of such anchoring amongst equity analysts (chart 1).

(A very good friend of mine, who happens to be a meteorologist, always tells me that the most accurate weather forecast for tomorrow is today’s weather, so perhaps I should treat anchoring with a little bit more respect, but that’s a story for another day.)

Chart 1: U.S. corporate earnings – actual vs. forecasts (deviation from trend)

Source: James Montier, Seven Sins of Fund Management, DrKW, 2005

Another example of behavioural biases is provided by MIT Professor Dr. Andrew Lo in his 2011 paper which you can find here. Dr. Lo makes the following point:

“Suppose you’reoffered two investment opportunities, A and B: A yields a sure profit of $240,000, and B is a lottery ticket yielding $1 million with a 25% probability and $0 with 75% probability. If you had to choose between A and B, which would you prefer? While investment B has an expected value of $250,000 which is higher than A’s payoff, you may not care about this fact because you’ll receive either $1 million or zero, not the expected value. It seems like there’s no right or wrong choice here; it’s simply a matter of personal preference. Faced with this choice, most subjects prefer A, the sure profit, to B, despite the fact that B offers a significant probability of winning considerably more. This is an example of risk aversion.

Now suppose you’re faced with another two choices, C and D: C yields a sure loss of $750,000, and D is a lottery ticket yielding $0 with 25% probability and a loss of $1 million with 75% probability. Which would you prefer? This situation is not as absurd as it might seem at first glance; many financial decisions involve choosing between the lesser of two evils. In this case, most subjects choose D, despite the fact that D is more risky than C.

When faced with two choices that both involve losses, individuals seem to behave in exactly the opposite way - they’re risk seeking in this case, not risk averse as in the case of A versus B. The fact that individuals tend to be risk averse in the face of gains and risk seeking in the face of losses - which Kahneman and Tversky (1979) called “aversion to sure loss” – can lead to some very poor financial decisions.

To see why, observe that the combination of the most popular choices, A and D, is equivalent to a single lottery ticket yielding $240,000 with 25% probability and -$760,000 with 75% probability, whereas the combination of the least popular choices, B and C, is equivalent to a single lottery ticket yielding $250,000 with 25% probability and -$750, 000 with 75% probability. The B and C combination has the same probabilities of gains and losses, but the gain is $10,000 higher and the loss is $10,000 lower. In other words, B and C is identical to A and D plus a sure profit of $10,000. In light of this analysis, would you still prefer A and D?”

For having “ integrated insights from psychological research into economic science, especially concerning human judgment and decision-making under uncertainty", Kahneman was awarded the Nobel Prize in Economics in 20022, the first time ever that a psychologist walked away with this prestigous award, and a sign that the establishment had finally begun to take behavioural finance seriously.

The Great Modulation

Now, you may begin to think that I am firmly siding with the proponents of behavioural finance and thus the opponents of EMH, but it is not that simple. What creates the doubt in my mind is that, for almost 70 years, EMH actually worked rather well. Between the mid-1930s and the early 2000s you could, by and large, ignore the occasional shortcomings of EMH and apply MPT in your portfolio construction.

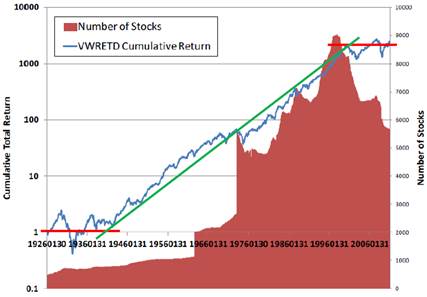

Chart 2: U.S. actual earnings vs. forecasts (deviation from trend)

Source: “Adaptive Markets and the New World Order”, Dr. Andrew Lo, December 2011.

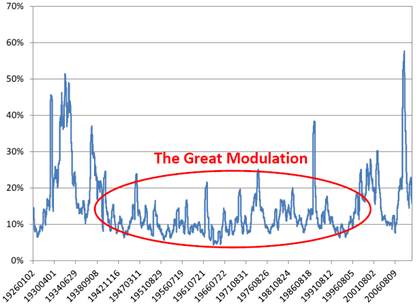

Following the Great Depression, the world entered an unprecedented period of economic growth and prosperity which resulted in a long and virtually uninterrupted rise in stock prices (chart 2). Dr. Lo calls this period the Great Modulation which is characterised not only by strong equity returns but also by comparatively low volatility (chart 3). Apart from a brief period around the October 1987 crash, equity volatility didn’t break the mid-twenties level for more than six decades which is quite an achievement.

During this period, the U.S. stock market, and with it most other stock markets around the world, produced a nearly linear, log-cumulative growth curve. Indexing your portfolio over the entire period (which is what true believers in EMH want(ed) you to do) would have yielded a return that would almost certainly have outperformed 99.9% of all active managers. It would be hard to shoot down MPT and EMH on the back of the performance of financial markets over this period.

Chart 3: Annualised volatility of U.S. equity returns ( 125-day rolling window)

Source: “Adaptive Markets and the New World Order”, Dr. Andrew Lo, December 2011.

One of the consequences of this extraordinary period was the invention of the 60/40 model. All you had to do - and many did it, and continue to do it - was to invest 60% in equities, 40% in bonds and sit back and let time do the job for you. Irresistibly simple. Then it all changed.

The new paradigm

Two major equity bear markets in the last 13 years have traumatised investors. The belief in MPT in general and EMH in particular has been shaken and finance theory will have to be re-written, or so it looks. So what is it specifically that has changed? Human behaviour certainly hasn’t. Greed and fear have been factors to be reckoned with since day nought. Dr. Lo, who has pioneered the research into how EMH can be adapted to incorporate behavioural factors, offers the following explanation (and I paraphrase):

The growing importance of the financial services industry, together with geopolitical changes (the U.S. is no longer the only dominant economic force in the global economy), and rapid advances in technology, have destabilised the equilibrium. The obvious implication, or so Dr. Lo argues, is that investors must change some of the tools in their tool box.

Interestingly, he doesn’t suggest that EMH should be mothballed altogether. To the contrary, he believes that EMH can work for extended periods of time provided investors behave rationally. I had the pleasure of meeting him in Cambridge (Massachusetts) a few weeks ago, and he delivered a convincing case that investor behaviour is actually rational most of the time when looked upon in aggregate. He calls it the Wisdom of Crowds and illustrated what he means with a simple example:

Imagine somebody puts a large jar full of jelly beans in front of you and you are meant to guess how many jelly beans the jar contains. You have no idea, but you are up for it, so you come up with a number. Sadly, unless you happen to be lucky, the chances are that your guess is miles off the true number. Now imagine that the same question is put to a large number of people and that the mean is calculated as the simple average of all the estimates. Interestingly, research suggests that the mean estimate is likely to be within a few percentage points of the true number. The Wisdom of Crowds.

The FT ran a story at the height of the credit boom back in April 20063 on the rapid growth of the CDO market in Europe. When asked by the FT to comment on this remarkable growth, Cian O’Carroll, European head of structured products at Fortis Investments, replied:

“You buy an AA-rated corporate bond you get paid Libor plus 20 basis points; you buy an AA-rated CDO and you get Libor plus 110 basis points.”

On the back of this statement, and despite all the evidence of froth in financial markets in 2005-07, it seems like the crowd was still quite wise. As Dr. Lo states in his 2011 paper:

“It may not have been the disciples of the Efficient Markets Hypothesis that were misled during these frothy times, but more likely those who were convinced they had discovered a free lunch.”

Occasionally, the Wisdom of Crowds turns into the Madness of Mobs and all rational behaviour goes out the window. History provides many examples of that - from the tulip mania in the Netherlands in the 17th century to the more recent bubbles we have experienced in dot com stocks and housing markets around the world. The once golden boy of central banking, Alan Greenspan, labelled it irrational exuberance in a speech in 1996 when commenting on what already then looked like lofty P/E levels on U.S. equities. As we now know, the bull market not only continued for a further 3 ½ years; it actually grew stronger. Once the mob gets going, it takes a great deal to stop it.

EMH is entirely unsuited to deal with froth. Charlie Munger (of Berkshire Hathaway fame) once said, and I paraphrase, what made economists love the EMH is that the maths behind it is so neat whereas the alternative truth is a little messy.

The Adaptive Markets Hypothesis

So what is the alternative to EMH? Dr. Lo has labelled it the Adaptive Markets Hypothesis (AMH), a name he coined back in 2004. AMH is an attempt to reconcile EMH with behavioural finance. AMH begins with the recognition that human behaviour is a complex combination of decision making systems. The focus is not on any single behaviour, but rather on how human behaviour responds to changing market conditions. Humans (investors) are neither perfectly rational nor entirely irrational. It all depends on circumstances.

In Dr. Lo’s own words4, AMH is characterised by:

- Individuals who act in their own self-interest;

- Individuals who make mistakes;

- Individuals who can learn and adapt;

- Strong competition which drives adaptation and innovation;

- A natural selection process which shapes market ecology; and

- An evolutionary process which determines market dynamics.

The implications of AMH

AMH and EMH only agree on the first point. Investors usually act in their own self-interest. The rest is a departure from classic EMH thinking. The consequences of this are many and quite profound.

For example, according to AMH, the relationship between risk and return is not linear and it is certainly not stable over time. This implies that the equity risk premium should fluctuate meaningfully as a function of time and cycle. I note with interest that people who entered the investment management industry in the 1980s and 1990s ‘grew up’ in a world where the relationship between risk and return was extraordinarily stable; EMH by and large worked. I suspect that many of those individuals continue to subscribe to EMH and see the more recent changes in the investment environment as an aberration. My suspicion that this is indeed the case only gets stronger when I see how many continue to cling to the 60/40 model.

Another implication of AMH is that the relative attractiveness of investment strategies will ebb and flow over time as some strategies (asset classes) are likely to perform better in certain types of environments than in others. Income generating strategies have performed very well recently, partly because of demographic factors which have driven pension funds and individuals away from equities and into asset classes offering a higher yield. EMH assumes that such ‘arbitrage’ opportunities are competed away immediately.

Furthermore, AMH, unlike EMH, distinguishes between characteristics such as ‘growth’ and ‘value’, permitting investors to take advantage of sentiment factors. A classic example is the late 1990s when value investors dramatically underperformed growth investors. AMH would have picked up such a trend. EMH did not.

Importantly, AMH also provides a distinction between risk and potential. In EMH, returns are normally distributed and there is no distinction between downside risk (bad volatility) and upside potential (good volatility).

Concluding Remarks

AMH is a new paradigm, still very much in its infancy, but there are things investors can take away from this.

Most importantly, if the best you can hope for in a world of rational investors is to perform in line with the markets (classic EMH thinking), then a vital consequence of AMH is that you can actually outperform the markets over time through a dynamic allocation strategy which varies the capital it allocates to equities in response to changing levels of risk.

Secondly, unless you truly believe that the current environment is an aberration, and the ‘good old days’ will soon return, the 60/40 model should be buried once and for all. It is entirely inadequate to deal with the realities of the current environment. Many universities and business schools around the world are yet to figure this out, so students all over the world continue to graduate in the belief that EMH has it all worked out, but the reality is starkly different.

Finally, EMH is a hypothesis. MPT is what practitioners in the investment management industry use to implement the theories behind EMH. AMH is a hypothesis as much as EMH is and tools allowing investors to adopt this new paradigm must be further developed. The process has already begun, though. If you are interested in learning more about how it works, please contact us.

Niels C. Jensen

6 June 2013

© Absolute Return Partners LLP 2013. Registered in England No. OC303480. Authorised and Regulated by the Financial Conduct Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP ( ARP). ARP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

Absolute Return Partners

Absolute Return Partners LLP is a London based client-driven, alternative investment boutique. We provide independent asset management and investment advisory services globally to institutional investors.

We are a company with a simple mission – delivering superior risk-adjusted returns to our clients. We believe that we can achieve this through a disciplined risk management approach and an investment process based on our open architecture platform.

Our focus is strictly on absolute returns. We use a diversified range of both traditional and alternative asset classes when creating portfolios for our clients.

We have eliminated all conflicts of interest with our transparent business model and we offer flexible solutions, tailored to match specific needs.

We are authorised and regulated by the Financial Conduct Authority in the UK.

1 A full account of the convenience store incident and the Roosevelt speech can be found in “Fear, Greed, and Financial Crises: A Cognitive Neurosciences Perspective”, by Dr. Andrew Lo, October 2011.

2 Kahneman did most of his work with Tversky but he had sadly passed away prematurely back in 1996.

3 “CDOs explode after growing interest”, FT Mandate, April 2006.

4 “Reconciling Efficient Markets with Behavioral Finance: The Adaptive Markets Hypothesis, Dr. Andrew Lo, The Journal of Investment Consulting, Vol. 7 no. 2, 2005.

© Absolute Return Partners