26 Years of Wealth Effect: Equity Valuation in the Greenspan/Bernanke Era

“We are all Keynesians now.” –Milton Friedman

I recently observed that P/E multiples are becoming stretched versus historic experience. Historically rich valuations, however, should be viewed in context of today’s highly supportive monetary environment.

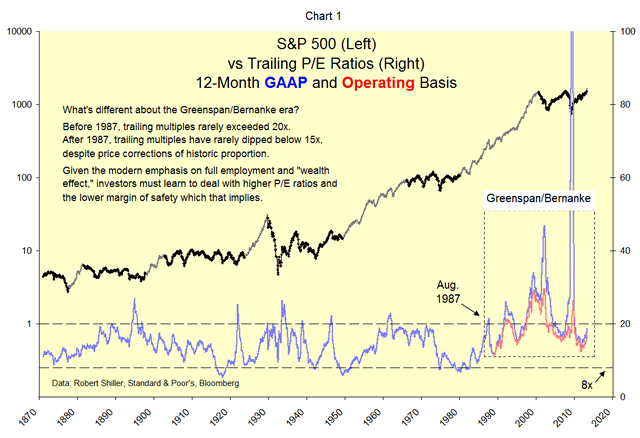

The Greenspan/Bernanke era has been characterized by substantially elevated P/E ratios. On an operating basis, for example, 12-month trailing multiples have averaged 19x over the past 26 years and have rarely dipped below 15x. See Chart 1 below.

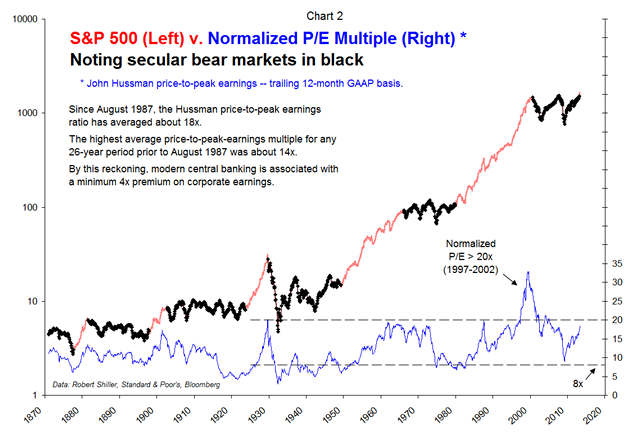

Chart 2 presents an alternative approach to valuation. Here, P/E ratios are adjusted for earnings volatility using the John Hussman price-to-peak-earnings (P/PE) method. This method eliminates earnings shortfalls that often occur during market downturns. The idea is to emphasize earnings capacity over reported earnings.

From a P/PE perspective, equities approached historic cheapness in 2009, reaching a normalized multiple of about 9x. Yet even on a normalized basis, the modern period is the richest on record. The average of normalized multiples during the Greenspan/Bernanke era has exceeded the average of any prior 26-year period by a minimum increment of nearly 4x. Median P/PE ratios tell a similar story: earnings-based valuations have become persistently rich.

So, why are modern P/E ratios so obviously elevated?

The quick answer is low interest rates. But nominal (and real) interest rates were also very low in the 1940’s and 1950’s. And the Greenspan/Bernanke period has featured relatively high nominal (and real) interest rates from time to time.

A better explanation is the Fed’s increased reliance on the “wealth effect” as a transmission mechanism to the real economy. During the market crash of 1987, Alan Greenspan promised to support the economic and financial system. Ben Bernanke has obviously taken the notion to new levels. At last year’s Jackson Hole conference, he explained as follows:

…[I]t is probably not a coincidence that the sustained recovery in U.S. equity prices began in March 2009, shortly after the FOMC's decision to greatly expand securities purchases. This effect is potentially important because stock values affect both consumption and investment decisions.

Increased reliance on equity prices should come as no surprise. The Fed has been operating under a dual mandate of price stability and full employment since 1978. When the interest rate mechanism is exhausted, the wealth effect is perhaps the only lever available to promote full employment.

Meanwhile, the US economy is more leveraged today than in the past. It now takes nearly four units of total debt (household, corporate and government) to produce a unit of GDP. Prior to 1986, less than two units of debt were required to generate a unit of output.

Leverage, of course, is a two-edged sword, magnifying good times and bad. Today’s leveraged economy has become increasingly vulnerable to market and/or economic downturns, suggesting that today’s monetary conditions may persist well into the future.

So what’s an investor to do?

Given the growing importance of equity prices in monetary doctrine, investors should expect higher valuations at market bottoms, and perhaps also at market tops. If the “greatest crisis since the 1930’s” produced a single-digit normalized multiple for only three short months, then routine market corrections are likely to bottom at much richer levels – perhaps in the vicinity of 14x-to-15x. With respect to market tops, the old ceiling of 20x may no longer apply.

This is not to say that valuation premiums are permanent. The current monetary environment will eventually change. It’s also possible – though perhaps implausible – that monetary accommodation ceases to work in the familiar way.

While grappling with these thorny issues, investors must learn to deal with today’s elevated valuations and the lower margin of safety which that implies. Paraphrasing Milton Friedman, “We are all momentum investors now.”

© Charter Trust Company