A week on from the sparks of theFOMCminutes and we can see how the market handles the subtler parts of Fed communication. Not well. Most of the dove camp talked about adjusting purchases up or down depending on economic conditions (all very reasonable and consistent) but stressed there was really nothing in the data for change. The hawk that counts, Bullard of the St. Louis Fed, even called for continued QE given low inflation. So the “employment is too low, continue” and "inflation is too low, continue” camps agree. The “QE is an inflation time bomb and it doesn’t make any difference anyway” camp remains marginalized.

Kocherlakota of the Minneapolis Fed trumped the discussions saying the gains from tightening on the grounds of financial instability are slight and the losses from tightening before employment and inflation hit target, are “tangible and significant.” To us that seems the prevailing wisdom.

The market seems to have priced in a taper of around $10bn a month sometime in September. And what we saw clearly last week was a market riddled with risk. The lack of liquidity of some mortgage pools was stunning. The street simply didn’t want them. Not surprising perhaps because the Fed’s holdings ofMBSincreased around $104bn since March and agency production of 3.0% and 3.5% coupons was $315bn over the same period. Any buyer taking a third of production will disrupt the market. This makes the rest of the “reach for yield” market risky. High yield is showing extraordinarily low spreads and at around 430bp, we feel we’re not paid enough to take part.

The 10-year note sold off with a low of 2.24% and made some damage to the technicals. The key for us is the hurdle of “sustained improvement in employment,” which isn’t there. Bernanke sounded optimistic on theNFPfront but it’s way too early to declare. NFPs are on the same 6-month average as they were a year ago…and two years ago. For now the market is consolidating and will put every economic number under the microscope.

A 2.5% World

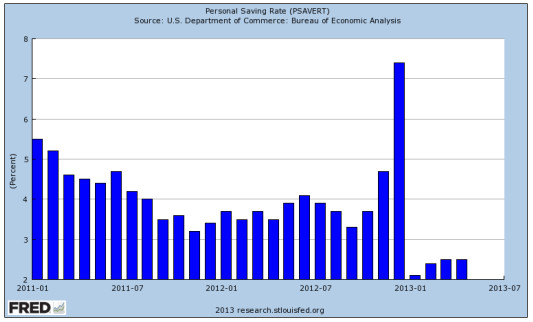

The second revision of Q1 GDP saw slippage in inventories and exports and a rise in personal consumption. Growth came in at 2.4%. Worse perhaps was nominal GDP growth of 3.6%. It has breached 4% only twice in the last nine quarters. A healthier number for any meaningful growth is around 7%. Government expenditures fell nearly 5% and that was before the sequester took hold. It’s now around 4% lower than a year ago. But the more worrying number was personal income, which declined in nominal value. Consumers ran down savings to keep spending up. Here it is (the spike in December was due to a one-off dividend increase):

Source: Federal Reserve Bank of St. Louis, Economic Research

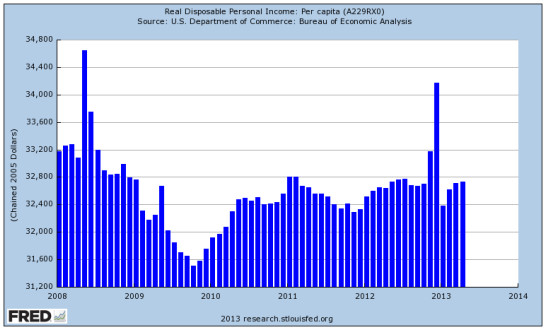

A series that we look at is the disposable income per capita, which looks like this:

Source: Federal Reserve Bank of St. Louis, Economic Research

Sputtering along. Look for a gradual improvement but even with housing and wealth effects going in the right direction, consumers are not in any rush.

Sources: Bloomberg, Barclays, Capital Economics, CRT Capital, Federal Reserve Bank of St. Louis, Trend Macro, Congressional Budget Office, FactSet, Federal Reserve Board, JP Morgan, Bureau of Economic Analysis, Federal Reserve Bank of Minneapolis, Sentinel Asset Management, Inc.

© Sentinel Investments

http://www.sentinelinvestments.com