I recently explored the possibility of a bond “massacre” akin to that of 1994. In 1994, the market was surprised by the Fed’s aggressive response to improving economic conditions. This resulted in a 26% price loss in 30-year Treasury bonds from cyclical top to cyclical bottom.

But is the 1994 experience relevant today? With New York Fed chief Bill Dudley and other Fed officials explicitly discussing the need to avoid a 1994-like scenario, perhaps another analogy is more fitting. The scenario which comes to mind is the summer of 1987. At that time, the stock market was “melting up” while the Fed gradually increased its target rate from a low of 5.875% in December 1986 to a high of 7.25% in September 1987. A ratchet of 1.375% was considered a minor, even timid, adjustment in those days.

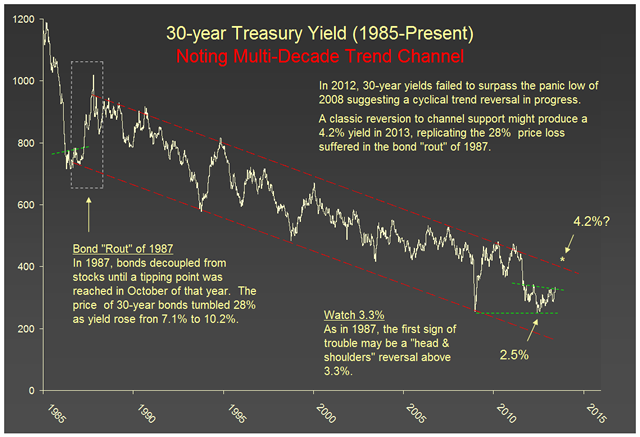

In April of 1987, with Fed funds at 6.0%, the long bond broke down from a “head & shoulders” reversal pattern. See chart below. The stock market continued to rally, advancing another 15% into late August. Bond prices tumbled lower until equities finally cracked in late October. The total price loss on 30-year Treasury bonds was 28% from cyclical top to cyclical bottom.

So, is 1987 relevant today? Perhaps, or perhaps not. The purpose of market analogies is not to predict the future, but to examine human behavior. A classic reversion to channel support near 4.0% on 30’s is not a farfetched scenario given the current backdrop of easy money and rising stock prices. If money is flowing out of bonds and into stocks (as in 1987) there should be no mystery at all.

© Charter Trust Company