While the “Sell In May” market anomaly is well-known, there’s little recognition of the impact this seasonal anomaly has historically had on stock market leadership. There’s one effect in particular I found so eye-popping that I broke ranks with Rogoff/Reinhart and rechecked my numbers. We can’t believe we’re the only ones to have noticed this, but I suspect there’s some intellectual sheepishness surrounding any discussion of seasonal market patterns—just as there was sheepishness in the practice of technical analysis before academics belatedly (and begrudgingly) admitted there might actually be something “there.”

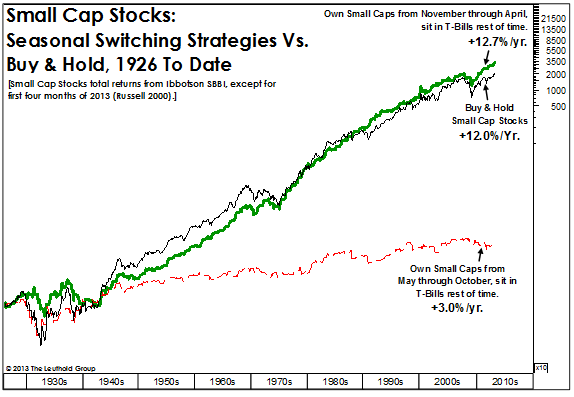

Let’s cut to the chase. Those inclined to sell in May should sell Small Caps. The seasonal pattern here can only be described as stunning, with all of Small Caps’ excess return since 1926 earned during the seasonally strong months of November through April. Over the last 87 years, one could have sat in cash each May through October and beaten “Small Cap Buy and Hold” on a total return basis. (The risk-adjusted return improvement is therefore astronomical.)

We like to find symmetry in market patterns or anomalies, so we reviewed the performance of the “inverted” seasonal Small Cap strategy (i.e., sit in Treasury bills during the “good” November-April period, and own Small Caps from May through October). Not a good idea, historically. This strategy has underperformed Treasury bills since 1926, compounding at 3.0% per year versus 3.4% for the 3-month U.S. Treasury bill.

Frankly, we don’t know what to make of this, nor whether we should even try to capitalize on it. But—with the MTI now in Neutral and our fundamental preference for Large over Small Caps intact—we’re suddenly big fans of this anomaly, at least for the next six months.

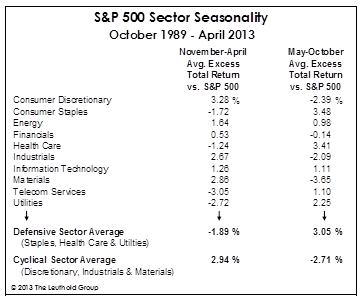

What if you’re a benchmark-pure Large Cap manager and have no Small Caps to sell? Easy. Sell cyclicals. They, like Small Caps, tend to lag defensive ones during the stock market’s seasonally weak months, although the data set backing up this finding is much shorter than the one used for Small Caps.

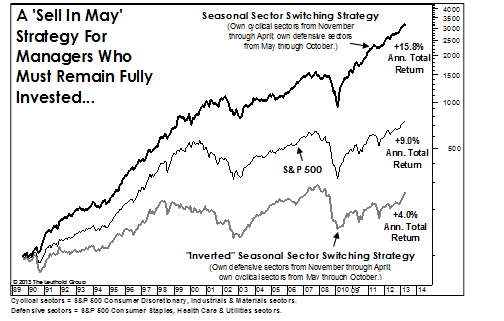

Since the inception of the S&P 500 sector data in late 1989 (and probably for much longer), it’s been beneficial to own cyclicals (Discretionary, Industrials and Materials) during the seasonally strong market months of November through April, then swap into defensives (Staples, Health Care and Utilities) for the May-October period. We view this as a “Sell In May” strategy for those who must remain fully invested, and it’s delivered a 15.8% annualized return since 1990. The S&P 500 is up only 9.0% annually over the same period, and the “inverted” strategy (own defensives during seasonally strong six months and cyclicals during weak six months) has earned a pathetic 4.0% per year.

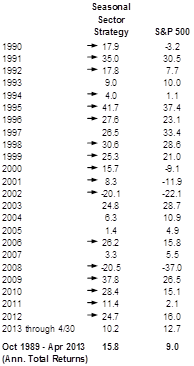

Annual results for the Seasonal Sector Switching Strategy are impressive, with the portfolio beating the S&P 500 in 17 of 23 years. Thanks to cyclical groups’ underperformance YTD, though, it’s a bit behind in 2013.

Oddly enough, while this seasonal bias isn’t part of our group model, the top two sectors in the latest domestic rankings (based on a “roll-up” of industry scores) are Staples and Health Care.

© Leuthold Weeden Capital Management