The Puzzle Is Complex: Education Funding, Assessed Values and Housing Prices

While many look to Memorial Day as the official beginning of summer, we hope all took time to reflect on the true meaning of Memorial Day as a time to thank, recognize and remember those that have, are and stand ready to defend our country and all we stand for. I, for one, am incredibly grateful to the men and women that serve our country and put their lives on the line to defend our freedom, democracy and way of life. It is my hope that our government can put partisan bickering and intransigence aside to ensure the best interests of our country are served just as these men and women do when they approach their jobs.

This past week saw the release of some interesting data around education and Public School Revenue and Housing Prices. Mind you, I am pretty sure the data providers did not put the two together nor am I sure many others have. Nevertheless, the output left a pit in my stomach for parts of our country and, absent substantive work by our friends in DC, potentially for others as well.

The DIVER Filter module results below begin an interesting tale. First, the number of children enrolled in Public Elementary and Secondary school is up in almost 1,300 counties. However, in those 1,300 counties, Public School Revenue is down in 490 (more students, less dollars). This led me to ask “what is the basis for this declining revenue?” The tables below show us the totals for where that basis is Local Sources of Revenue (286 counties), State Sources of Revenue (266 counties) or Federal Sources of Revenue (339 counties).

What is the overlap? In other words, which counties are feeling the pain from a decline in all three sources? “Only” 59 of them. I take this a step further to provide a sense of which of those counties continued to feel the pain through 2012: which of those coutnies also saw a decline in Assessed Values? The results are summarized below. Importantly, be reminded that our analysis looked at those locations that meet all of our criteria.

DIVER Filter Module; State and County Taxation, Treasury and Assessment Offices; US Census Bureau.

|

State |

County |

|

Georgia |

Glascock |

|

Maryland |

Somerset |

|

Montana |

Beaverhead |

|

Wyoming |

Johnson |

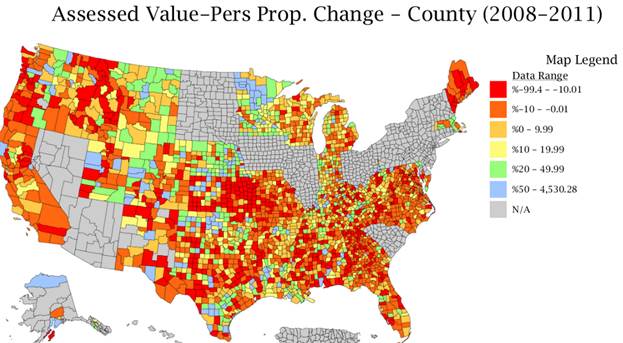

The four “standouts” above are not alone in seeing their Assessed Values fall. The most complete data we have for Assessed Values for 2012 looks at 2,421 of the 3,200+ counties. Assessed Values for 2012 v. 2011 are greater in 1,149 counties but, unfortunately, declined in 1,272 counties. Below is a longer term perspective on what has happened with Assessed Values. Orange, yellow, green and blue are greater than zero for the three year period. Why the focus? Assessed Values drive Property Tax Receipts which can be a primary source of local dollars for schools (see above).

DIVER Map Module; State and County Taxation, Treasury and Assessment Offices. 2012.

One can’t help but wonder (worry?), what happens if the recovery is not as robust as some suggest or if Washington can’t get its act together and come up with a responsible course of action? You say, come on, here you go again crying wolf. Things are improving. Employment and housing are doing pretty well (we addressed employment recently and will continue to watch it and income levels in the coming months). You also remind me of two factors: Assessed Values trail the housing market and prices by approximately 24 months and the housing market has been improving so much so that some of us are starting to hear of bidding wars (my sarcastic response: certainly has nothing to do with artificially low rates and the fact that over 95% of new mortgages end up with Fannie and Freddie).

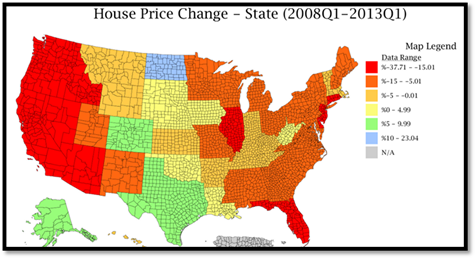

I concur with you regarding the delay in the impact of the change in Housing Prices on Assessed Values but worry that the decline in home values suffered across much of the US has not yet been fully realized in Assessed Values (DIVER subscribers – use the Filter Module to nail this one). My concern is supported by the counter-point (“Point/Counter-Point” – name the show and, for bonus points, the two comedians) to the position that ‘the housing market is as it was before the Great Recession.’ Looking at the recent House Price Change data one can see it is not as pretty a picture as one might think when we assess the data from when the Great Recession commenced (12/07) – only yellow, green and blue represent a positive change. For the record, Housing Prices in Georgia, Maryland, Montana and Wyoming (the home of our four highlighted counties above) still have not recovered to the pre-recession levels.

DIVER Map Module; FHFA.

Moreover, if you look to the FHFA’s Housing Index, those same four counties noted above have not seen their index level return to pre-recession levels. They are not alone. According to the FHFA, only 1,137 counties’ Housing Index Price is, as of the end of the 1st quarter of 2013, greater than it was at the end of 2007.

The puzzle is large and the pieces complex. The relative impact and importance of the various data points are for you to decide. The impact of the data points, those cited herein and the many others we reference weekly, is indisputable.

For more information on our Assessed Values database or the DIVER platform, please contact us at [email protected] or 203.276.6500.

Have a great week.

Gregg L. Bienstock

CEO & Co-Founder, Lumesis, Inc.

This Week’s Data :

- Education: Enrollment, Revenues, Spending & Debt, County, FY 2011

- Weekly Initial and Continued Jobless Claims, State, 5/11/2013

- Drought Intensity, County, 5/21/2013

- House Price Change and House Price Rank Change, 2012 Q1 - 2013 Q1, State

- Housing Price Index, County & State, 2013 Q1

- Coincident Index Change, April 2013, State

- NEW: Fed. Funds Received, State and County, 2013, 2012, 2011

- NEW: Fed. Funds Received per Capita, State and County, 2013, 2012, 2011

- Special Event: Tornadoes, County, 2013

- UPDATED: Bankruptcy Filings - Issuers, County, 2013

- UPDATED: Default Filings - Issuers, State, County, 2013

© Lumesis