ING Fixed Income Perspectives May 2013

Bond Market Outlook

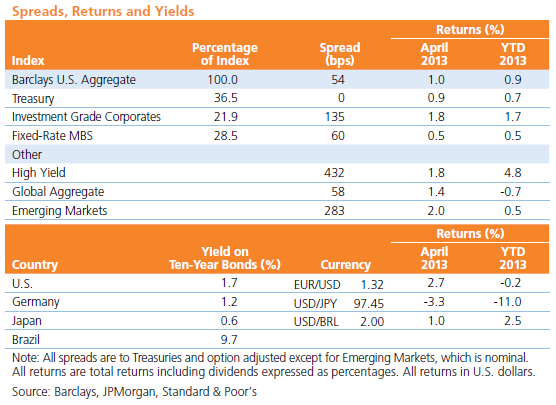

Global Interest Rates: With near-term tightening unlikely, funding conditions should remain accommodative.

Global Currencies:U.S. dollar strength is unsustainable until the Fed tapers its purchase programs; we continue to favor EM currencies over developed markets.

Corporates: The market has been resilient in the face of weaker macro data; we remain constructive on financials but cautious on the deep cyclical industries.

High Yield: We are constructive in the near term, but strong performance and high dollar prices have raised the risk of a pullback.

Mortgages: Central banks in the U.S. and Japan will continue to support mortgages, but uncertainty surrounding the timing of the Fed’s exit strategy will cause volatility.

Emerging Markets: We continue to favor sovereigns over corporates, high yield over investment grade and local over hard currency.

Macro Overview

How do you like them apples? By pointing out some Excel blunders in the data of Harvard economists Reinhart and Rogoff, a UMass-Amherst grad student appears to have gotten their number and in the process discredited their seminal work touting the merits of austerity. Though Good Will Hunting fans may be amused to see a couple of Harvardians get their comeuppance, you don’t need the titular character’s wicked smarts to deduce that harsh government spending cuts may not be the best way to pick up your economy.

■If the old adage that you have to spend money to make money is true, austerity — i.e., spending a whole lot less — doesn’t seem too bright. Of course, there’s also a maxim about spending more than you make. Whichever you subscribe to, finding growth in a time of debt is bedeviling the entire global economy. Falling commodity prices and lower growth in China and emerging markets indicate that global imbalances are still in the process of being unwound, suppressing demand from the developed world. Europe, in particular, finds itself smoldering in an austerity-induced recession.

■Luckily, central banks appear to have developed an adage of their own: you have to print money to make money. While it may lack the pedigree of those earlier chestnuts, this new saw has financial markets climbing and is buying time for the Reinharts and Rogoffs of the world to try to reconcile the need to grow with the need to spend less. Investors, meanwhile, are climbing the wall of worry, as the flood of central bank liquidity continues to be pulled into higher-yielding asset classes in this low-interest-rate environment.

■Our theory is that the U.S. will remain the most credible example of how to grow in a time of debt, buoyed by the strength of the consumer, as we wait for the handoff of central bank stimulus to the U.S. industrial base in the form of capital expenditure growth. Broadly, global caution will continue to suppress interest rates and commodity prices, which will be supportive of the U.S. dollar and the bond market in general.

Sector Overviews

Global Interest Rates

- Central banks have never been more accommodative. The Fed and Bank of Japan continue their ambitious purchase plans, and the ECB recently joined the party with a rate cut in May. Weak growth impulses and benign inflation conditions are likely to continue in the second and third quarters of 2013, and we expect funding conditions to remain easy.

- The recent sharp selloff in global duration was driven by a lack of transparency by the Bank of Japan in defining when they will step in and buy. While rich valuations do contribute to a negative strategic view, central bank liquidity will remain a major obstacle to a sustained selloff. We remain bearish on Japan and most other developed nations and broadly favor higher-yielding emerging markets like Brazil and Mexico.

Global Currencies

- We do not believe the U.S. dollar’s recent strength is sustainable until the Fed begins to taper its asset-purchase programs, unlikely in 2013 given the employment situation. However, we favor currencies like the Canadian dollar, Brazilian real and Mexican peso that will benefit from U.S. dollar strength and lower-beta currencies like the Chinese renminbi and Malyasian ringgit given yield and diversification benefits. We remain broadly bearish on developed market currencies like the euro, pound sterling and Japanese yen.

Investment Grade Corporates

- We’ve become more constructive on corporates, as the market has been resilient in the face of weaker macro data. With earnings season coming to a close, investors soon may focus more closely on macro and geopolitical headlines, but for now we are inclined to give the market the benefit of the doubt given the muted volatility in spreads this year.

- Financials, utilities and transportation continue to lead the market in excess return performance year to date, while the basic, energy and communications industries continue to lag thanks in part to negative event risk and, in terms of the first two, weakness in commodity prices. We remain constructive on financials and cautious on the deep cyclical industries.

High Yield Bonds Corporates

- Like the equity markets, the high yield market came under pressure in April before yields resumed their march lower into month end as stocks hit new record highs. Corporate fundamentals remain in good shape, though revenue gains are increasingly difficult to come by. Defaults are likely to remain low, but overall credit improvement appears to have ended.

- Net new issuance has been limited, and flows in search of yield continue to support the asset class. With spreads of approximately 450 bps, we are constructive on high yield in the near term; the recent strong performance and high dollar prices across rating categories have raised the risk of a near-term pullback, however.

Mortgages

- Although recent Fed comments support the continuation and pace of its purchase programs through 2014, uncertainty surrounding the timing of Bernanke’s exit strategy will continue to cause volatility in the agency RMBS market. We view mortgages as fairly valued, but high dollar prices and heighted prepay risk due to adjustments to HARP/HAMP are salient concerns, though demand continues to be dominated by the Fed and Japanese investors in support of the asset class.

- Non-agency RMBS continues to benefit from positive momentum in the U.S. housing market and the low-interestrate environment, as a flood of liquidity surges into a market with a shortage of bonds to buy. The regulatory environment is a major hurdle in what will be a multiyear recovery process for non-agency RMBS, but the asset class remains well-supported by banks, insurers and money managers seeking yield.

- Demand for CMBS has remained strong despite elevated new issuance. Certainty around the depth of problems in commercial real estate has increased. Going forward, there will be a premium on security selection as losses begin to materialize and valuations disperse. While we are concerned about underwriting standards, deals continue to be well received by the market.

Emerging Markets

- Emerging markets continue to feel the effects of a benign global growth environment. We still have a positive assessment on emerging sovereign debt given current valuations and spread levels, though we expect local markets — driven by the outlook for currency appreciation and higher yield — to continue to outperform.

- Emerging market corporate valuations have re-priced relative to domestic corporates as the weakness in commodity prices has filtered through to spreads. Geopolitical tensions in Asia and idiosyncratic events in Latin America have contributed to high yield underperformance in recent months. Emerging corporates may be due for a rebound, but the outlook for commodity prices will likely determine the sustainability of any rally.

ING U.S. Investment Management’s fixed income strategies cover a broad range of maturities, sectors and instruments, giving investors wide latitude to create a new portfolio structure or complement an existing one. We offer investment strategies across the yield curve and credit spectrum, as well as in specialized disciplines that focus on individual market sectors. We build portfolios one bond at a time, with a critical review of each security by experienced fixed income managers. As of December 31, 2012, ING U.S. Investment Management managed $127 billion in fixed income strategies in the United States.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 6523