Once again stock prices moved higher last week despite mostly poor economic data and a background in Washington DC of multiple scandals. The latter begging the question as to whether substantive policy actions are now off the table for the year.

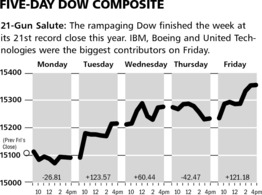

As the charts above illustrate, the Dow Jones Industrial Average climbed by 1.6% led by a resurgent Boeing. At the same time the

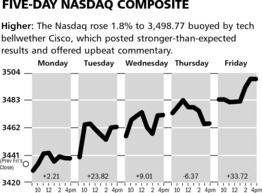

NASDAQ Composite jumped by 1.8% led by technology companies.

The Market & Economy

Last week’s reports on new home starts, regional manufacturing surveys and the weekly reading on initial unemployment claims were all very disappointing and imply that estimates of second quarter GDP growth rates will be lowered. My view of a two percent growing economy continues to be the best bet.

Those thinking we have turned the corner to higher growth underestimate the impact of higher taxes here at home and closing export markets due to recession overseas ( Europe & South America), and the stronger US dollar which represents a double whammy to the export sectors of our economy.

This along with the ongoing and negative impacts of planning for the implementation of Obamacare in 2014 will all serve to keep growth from moving to a higher level. These thoughts were validated just this morning by the President of the Dallas Federal Reserve

Board who indicated that the Fed has led the economy to water, but the economy doesn’t want to drink for the aforementioned reasons.

Also this morning, the Chicago Fed-National Activity index showed a negative reading. This measurement is about the best aggregate of coincident economic data out there and quite simply it looks like the economy is slowing as we head into another summer.

At the same time investors continue to prosper. Ironically this is due to the weak economic outlook which fosters the zero interest rate policy fueling this bull market. This monetary policy has spread to virtually every Central Bank of any importance out there, with many foreign central banks recently easing policy and engaging in their own version of quantitative easing. Thus talk about the Fed changing policy remains just that - talk.

As a result, financial engineering by corporations around the world continue. Buyouts and special dividends are just a couple of ways for companies to return money to shareholders (see our comments below about Freeport). Incidentally, the CEO of Apple told Congress last week what they didn’t want to hear - that is to lower and simplify the tax system in this country. Then corporations will start using their cash hoards to invest for growth, versus return of excess capital.

I am quite certain that message was lost upon the members, and don’t expect any serious attempt to change fiscal policy in this Congressional session.

What to Expect This Week

It’s the week leading up to the Memorial Day weekend, which starts the summer season for many. The biggest item will be Fed Chairman Bernanke testifying in front of Congress on Wednesday. There will not likely be any surprises here.

Additionally, three more pieces of economic data will be released as the week goes on. It is sad to say that the numbers coming this week on new home sales and durable goods will have very little impact on either investor psychology or the economic outlook.

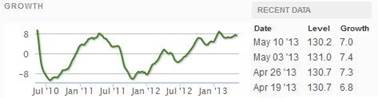

Finally, the Economic Cycle Research Institute’s weekly gauge of leading indicators fell last week (see chart next page). Overall though, there is no obvious change of trend going on here either. They, of course, view the US economy as already in a recession. My view is that the data does not support that notion.

Next Monday is MemorialDay. As such the markets will, of course be closed, and our next report to you will be two weeks from this morning.

![]()

SYMBOL: BRCD

Brocade Communications Systems reported second-quarter earnings results that were better than expected, but management lowered third-quarter guidance due to a slowdown in the storage business. The Company earned $0.17 per share, which was 2 cents better than consensus estimates. Revenues were roughly flat from the previous year at $538.8 million. We expect the slowdown in the storage market will be short-lived, and the networking division should more than offset any weakness at the division.

The operations at the Company during the quarter were solid, and management has been able keep margins high. Operating and net margins expanded since last year, and gross margins remained at 62 percent from last year. We expect further cost-cutting at the Company, which should lead to better operations in the second half of this year.

Shares of Brocade sold off modestly after this earnings release due to the decrease in next quarter’s earnings expectations. We look for the networking division to drive growth in the second half of this year. Last week Cisco Systems stated they see good market conditions around the world. The management team has also continued to be aggressive with its share repurchase plan and has been reducing its share base. Any improvement in the storage sector should lead to an $8 share price by the end of this year.

![]() Three-Month Chart

Three-Month Chart

![]()

SYMBOL: FCX

Both Freeport-McMoRan and Plains Exploration & Production announced special one-time dividends today to help the deal close on time. Plains will be paying out a one-time dividend of $3 per share immediately, while Freeport shareholders will receive a one-time $1 dividend once the deal closes. This essentially sweetens the bid for Plains, but should confirm the deal will get done. Plains shareholders are set to vote on the deal later today.

Investors have started to warm up to the prospects of this deal, especially as the price of copper and gold have come down. We look forward to hearing management’s larger plans for Plains, and believe the special one-time dividends are beneficial to shareholders. As investors become more comfortable with the closing of this deal, we expect the shares of Freeport to rally $40 by the end of this year.

![]() Three-Month Chart

Three-Month Chart

© McIntyre, Freedman & Flynn