Asia Brief: China's Car Fleet The Largest in the World?

Car sales in China have grown rapidly since 2009 and it is on course to outstrip the US in terms of the size of its car fleet by the end of this decade. This presents a major challenge to the Chinese government, which must balance its people’s happiness and political stability with economic development in an environment which has already been compromised. The momentum of demand for new passenger vehicles is likely to make air quality worse and Beijing has introduced emissions and efficiency standards to address the problem. China will also need to use more high quality gasoline and new refining capacity may be needed. However, oil is relatively low as a proportion of overall energy usage and in aggregate China should be able to handle the additional energy needs of its growing vehicle fleet.

The largest car fleet in the world?

May 2013

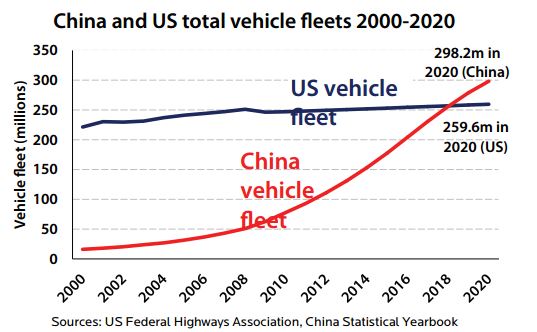

The growth in consumption in China has major implications for the environment, the global economy and world energy demand. One of the most significant drivers of this is the likely growth in the Chinese car fleet, and on current trends, it could outstrip the US car fleet by the end of the current decade (see chart below). This is not alarmism. It is simply based on continuing the current level of annual sales of around 20 million units and represents almost a tripling in the number of vehicles on the road in China. As with many things in China, the scale of this development is awe-inspiring, but this may well not be the end of it, given that China’s population is around four times that of the US and there is no reason in principle why car sales should slow down once the artificial level of parity with the US has been achieved.

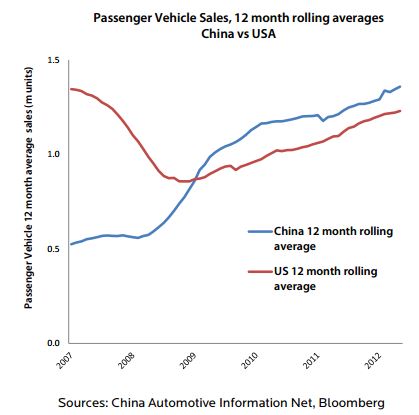

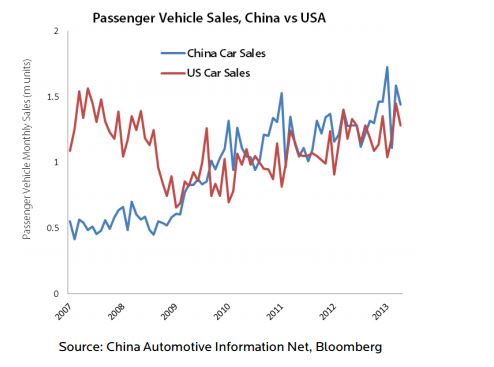

An acceleration of vehicle sales in China has been underway for some time and in 2009 the government introduced a range of subsidies such as a ‘cash for clunkers’ scheme, and this provoked a doubling average sales volume, from half a million to around a million units a month. Perhaps most surprising is that even once the subsidies were withdrawn vehicle sales remained around one million units a month (see chart at the top of pg. 3). This has continued to climb, even despite a slowdown in economic activity over the last year, and China has now had higher average monthly car sales than the US for almost three years.

Rising car sales and Chinese energy consumption

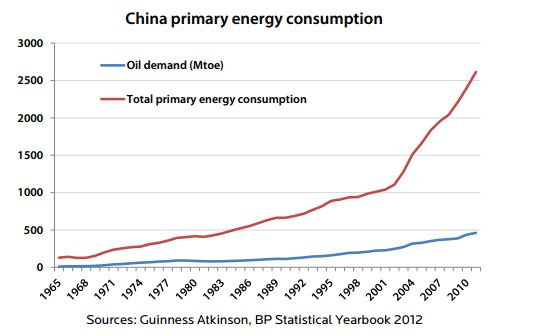

Chinese energy demand has been growing rapidly as the economy has industrialized, but it is notable that oil demand has not kept pace with overall energy consumption (see chart below). This means that China potentially has the headroom to increase its oil demand without tilting its overall energy usage too much in the direction of oil. The reason that China has been able to achieve this is because much of its baseline and industrial demand for energy is met by domestic coal deposits rather than imported oil.

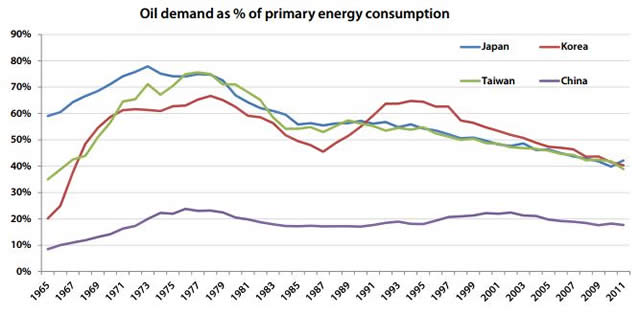

This puts China at an advantage compared to its regional peers, all of whom went through a similar process as China when their investment-led growth phases cooled and consumption became more significant as a driver of Gross Domestic Product (GDP) growth. Unlike Japan, South Korea and Taiwan (see chart below), Chinese oil demand relative to primary energy consumption has barely crept above 20%, while these other nations peaked at 70-80% before falling back to around 50% following the end of their investment phases of growth. For Japan, South Korea and Taiwan, with few energy resources of their own, imported oil was the quickest and easiest method of ramping up energy consumption domestically, but it left them exposed to imported inflation if international oil prices rose. With large coal deposits of its own, China has been in an advantageous position, and this could allow it to rapidly expand vehicle usage without a debilitating effect on its balance of payments status and inflation.

The efficiency challenge

The Chinese government seems aware of the potential additional demand for energy as a result of the growth in the car fleet and increased passenger kilometers travelled, and the Ministry of Industry has announced that new fuel efficiency standards will be implemented from May 1st 2013. These standards aim to bring down the average fuel consumption of vehicles sold in China on a progressive basis between now and 2015 to 6.9 liters per 100 kilometers. This will be a challenge for the Chinese car manufacturers, in particular, the domestic makers which generally fail to meet this consumption standard at present.

The idea is to apply the new standards across the range of vehicles sold by a manufacturer, such that some more efficient vehicles may effectively ‘subsidize’ the less efficient cars. Electric vehicles and plug-in hybrid vehicles are zero rated for the purposes of the scheme, and this should encourage manufacturers to consider including these in their fleet to help meet the overall targets. To date the sales of alternative fuel vehicles have been disappointing, and according to the Chinese Association of Automobile manufacturers (CAAM) 11,375 electric vehicles and 1,416 plug-in hybrids were sold in

2012.

There may be better prospects for natural gas-fuelled vehicles, although China is pursuing a different strategy to the US with a focus on passenger cars powered by compressed natural gas in China, rather than freight vehicles powered by liquid natural gas in the US. China has also concentrated on taxis and buses as early adopters, and half of the installed taxi fleet of 1.1 million taxis is already running on natural gas. By the end of the last 5 year plan in 2010, China had an installed base of 1,000 gas refilling stations for compressed natural gas, and the plan for the current five year plan to 2015 is to double this. However, the demand from consumers for these vehicles has been much more circumspect, and in 2012 it is estimated that less than 30,000 natural gas passenger vehicles, only 0.2% of the total new passenger cars, were sold last year.

Protecting the environment

A significant increase in the Chinese car fleet presents serious challenges to the government, as it means significantly greater demand for fuel and greater carbon and pollutant emissions. The mandate for the new Chinese government is more complex than for previous administrations, and there is a recognition that the happiness and stability of the Chinese people can no longer be bought with just material gain. After decades of rapid economic expansion, the environmental hangover is serious, and poor air quality has become a serious matter for the authorities. Poor air quality is a major issue in the larger Chinese cities, not least Beijing, which has taken steps to force drivers to improve the quality of gasoline they use. On February 1st 2013, a new emissions standard, Bejiing V, was introduced, and this is similar to the Euro V emissions standards. The new standard will prevent new vehicles being sold or registered if they fail to meet stricter emissions standards for particulate matter. While this is unlikely to solve the issue in the near term, it is at least a start in dealing with an issue that could get much worse if the projections for car sales in China over the rest of this decade come to pass.

Although Beijing V, and potentially China V, should be helpful in reducing particulate matter emissions, it will be difficult to roll it out nationally in the near future given China lacks the refining capacity to scale up the supply of the required high-grade fuels, and many of the vehicle manufacturers sell vehicles that are not in compliance with the new standard.

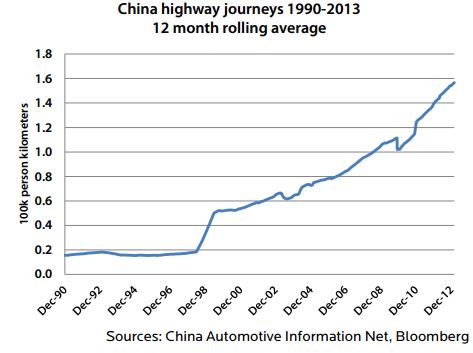

More cars means more journeys and more roads

There is growing demand for passenger vehicle transportation, and Chinese highway journeys have been growing with little interruption since the early 1990s (see chart at top of pg. 6). Although public transportation has seen faster growth in terms of passenger usage, China’s scale and geography suggest that affordable personal transportation could see significant growth in the coming years. This offers the possibility of both a growing fleet of vehicles and greater usage of those vehicles.

As well as developing the vehicle fleet, the government is also encouraging the development of an appropriate road network for the country. In line with encouraging economic development outside of the coastal provinces, the government is keen to build new roads to make the interior of the country a better place for economic activity. The scale of the challenge is not trivial – it is estimated that at the end of 2010 there were 1,200 townships and 120,000 villages without paved roads. This is a significant cost to the economy, and logistics is estimated to cost 18% of GDP in China, compared to 8% in the European Union and 9.5% in the US. In the 12th 5 year plan there is significant spending on new roads planned, with the ultimate aim of having all townships and 90% of villages accessible by 2015.

China on the move

Getting China on the road is a herculean task, and China may well have the largest car fleet in the world in a few short years. Energy consumption will inevitably rise as a result of the growth in car sales, but China is in a favorable position relative to its peers, as it uses much less oil in its energy mix relative to other Asian peers at this stage in their development. Although the rapid nature of this growth means that the Chinese car fleet will be in aggregate relatively young, there is good demand for both SUVs (Sports Utility Vehicles) and high performance luxury cars, which tend to use more energy than the lower powered, smaller cars.

The scale of the investment required in both fixed infrastructure and vehicles offers a growth opportunity to investors, while the government needs to keep its people on-side and manage the process responsibly. The government’s first task remains to limit the damage from increased emissions and keep its first tier cities as places where people can live and work happily and safely.

Market Review

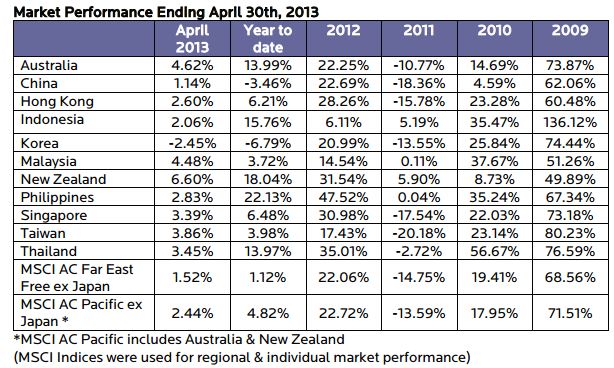

Asian equities performed well in April, with most markets up strongly. South Korea was the notable outlier, which finished the month down 2.45%. For the year to date only China and South Korea remain in negative territory, and five of the markets have already achieved double digit returns. The top-performing markets in April were New Zealand, Australia and Malaysia, while the Philippines and New Zealand have been the best performers year to date.

The malaise in South Korea is partly related to continued sabre-rattling by the North Korean regime, but it is also due to sluggish growth in the economy. To address this, the South Korean central bank recently cut interest rates for the first time since October 2012. This takes policy interest rates to 2.5%, which is their lowest level since early 2011. Despite the weak equity performance, there are signs of recovery in the Korean property market with April’s data showing lower unsold inventories, higher transaction volumes and flat prices.

China continues to confound investor expectations with good GDP growth of 7.7% in the first quarter failing to spark a sustained recovery in equities. It seems the market is still coming to terms with the slower pace of economic growth, and the newly re-appointed central bank governor, Zhou Xiaochuan, described the current growth rate as ‘normal’, and that China must sacrifice short-term growth for restructuring. Concerns also remain about China’s indebtedness, with one of the international rating agencies reducing China’s sovereign debt rating in April as a result of the growth in non-bank lending.

Elsewhere in the region, Indonesia’s credit outlook was downgraded from positive to stable as a result of an ongoing disagreement between President Yudhoyono and the parliament over fuel subsidies. Investors had hoped that the fuel subsidies would be reduced or withdrawn altogether in the near future, but the President demanded that parliament offer cash transfers to the poor to soften the impact of the removal. Parliamentary approval has not yet been granted, and the debate between the two sides could take some time.

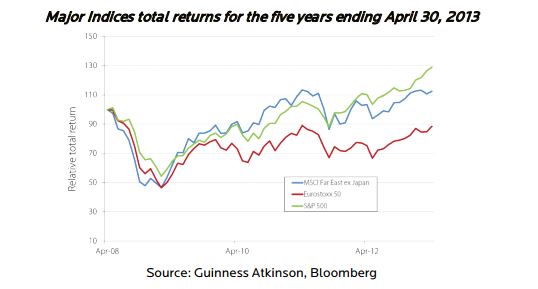

Over the last five years, the S&P 500 index has outperformed both the Asian and European benchmark indices (the MSCI All Country Far East Free ex-Japan Index and STOXX Europe 50 Index). The Asian reference benchmark we use has performed sluggishly so far this year, with China and South Korea particularly holding back the wider market due to their heavy benchmark weights. European equities remain well behind the other two regions, although they have performed relatively well so far this year.

China Economic Monitor

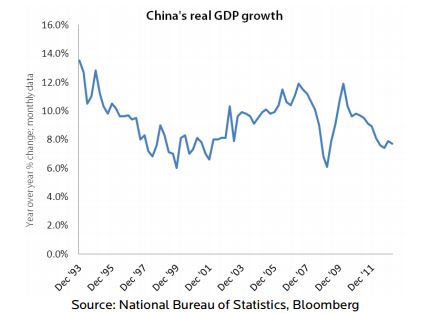

Chinese growth remains relatively healthy despite a slowdown in recent months. At 7.7% in real terms for the first quarter of 2013, this is well ahead of the levels recently achieved by other economies of its size, although it is lower than China has achieved in recent years. The economy is on track to achieve the new government’s stated target of doubling real GDP and GDP per capita between 2010 and 2020. There have been signs of softness in growth elsewhere in Asia, but so far Chinese policymakers have not reacted by cutting interest rates, nor has there been a move on the currency in response to the devaluation of the Japanese Yen in recent months.

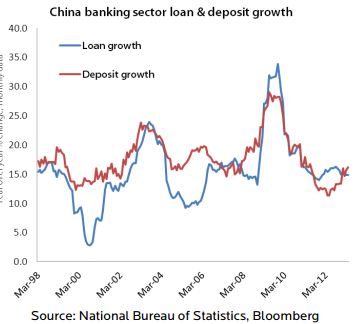

Deposit growth has rebounded strongly in recent months to achieve a rate of 16% in April, its highest level since June of 2011. Although the Chinese banks have substantial deposit-taking franchises, there is some disquiet at the central bank at the level of wholesale financing undertaking by the banks, and this growth in deposits may be a reflection of a desire to shore up the liability side of their balance sheets. On the lending side, loan growth remained solid at 16% year over year in April, which is reasonable. However, total social financing grew 81% in April year over year, suggesting that other forms of financing grew much quicker than bank lending. Set against the background of slower growth in China, there remains a question in some investors’ minds as to where the additional financing is going and how much is going to state-owned enterprises and the property sector at the expense of the private sector.

The data suggest that inflation in China remains well under control, with falls in both the rate of growth in the retail price index and the producer price index in April. Consumer prices also seem to be manageable, with falls in wholesale pork prices in recent weeks suggesting that inflation is being held at bay despite the central bank’s monetary stimulus policies. However, there is some concern that the low inflation could in fact reflect sustained weakness in underlying economic activity, with falling producer prices suggesting that corporate margins in manufacturing could come under pressure.

Passenger vehicle sales in China fell slightly in April to 1.44 million units. Although this is disappointing, the absolute level of sales remains above that sold in the US in April (1.28 million units), and is high by historical standards. The fall in unit sales is in line with the data we see elsewhere in the economy, which suggests that growth is reasonable, but has not re-accelerated in the way we hoped earlier this year.

Performance data quoted represents past performance and does not guarantee future results. Index performance is not illustrative of Guinness Atkinson fund performance and an investment cannot be made in an index. For Guinness Atkinson Fund performance, visit gafunds.com.

Mutual fund investing involves risk and loss of principal is possible. Investments in foreign securities involve greater volatility, political, economic and currency risks and differences in accounting methods. Non-diversified funds concentrate assets in fewer holdings than diversified funds. Therefore, non- diversified funds are more exposed to individual stock volatility than diversified funds. Investments in smaller companies involve additional risks such as limited liquidity and greater volatility. The Fund may invest in derivatives which involves risks different from, and in certain cases, greater than the risks presented by traditional investments.

The MSCI All Country Far East Free ex-Japan Index (MSCI AC Far East free ex-Japan Index) is a free float- adjusted, capitalization-weighted index that is designed to measure equity market performance in the Asia region excluding Japan. The Index is made up of the stock markets of China, Hong Kong, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand.

The MSCI All Country Pacific Free ex-Japan Index (MSCI AC Pacific Index) is a free float-adjusted, capitalization-weighted index that is designed to measure equity market performance in the Pacific region. The Index is made up of the stock markets of Australia, China, Hong Kong, Indonesia, Korea, Malaysia, New Zealand, Philippines, Singapore, Taiwan and Thailand.

The S&P 500 Index is a broad based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general.

The STOXX Europe 50 Index (STXE 50), Europe’s leading Blue-chip index, provides a representation of supersector leaders in Europe. The index covers 50 stocks from 18 European countries: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom.

Consumer Price Index (CPI) is a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food and medical care.

Producer Price Index (PPI) is a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time.

Retail Price Index (RPI) is a measure of consumer inflation produced by the United Kingdom’s Office for National Statistics.

One cannot invest directly in an index.

This information is authorized for use when preceded or accompanied by a prospectus for the Guinness Atkinson Funds. The prospectus contains more complete information, including investment objectives, risks, fees and expenses related to an ongoing investment in the Funds. Please read the prospectus carefully before investing.

Opinions expressed are subject to change, are not guaranteed and should not be considered investment advice

Distributed by Quasar Distributors, LLC.

© Guinness Atkinson Asset Management