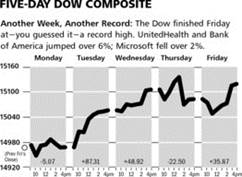

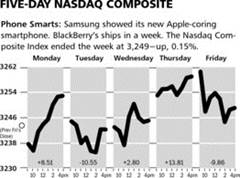

Stocks moved higher again last week as the data continues to reflect an economy that continues to trudge along to the consternation of many.

As the charts above illustrate, the Dow Jones Industrial Average gained nearly a full percent, while the NASDAQ Composite led by a resurgentApple

moved higher by 1.7%.

The Markets & Economy

Central banks around the world are joining in on the easing parade currently being led by the USA and Japan. This is flooding the world with money, which is being used to finance the unthinkable - that being European sovereign debt, despite the deterioration of the fundamentals throughout Europe. All those bond bears here in America need only look to the rates being achieved in basket-case economies such as Italy and Spain. You then quickly realize that the US bond market might not be as overvalued as most would have you believe.

There was very little of consequence released last week on the domestic economy. Our current estimate for the national deficit this year has fallen to below one trillion dollars. This is good, but comes from higher taxes and the smaller increase in spending emanating from the sequester. It is not indicative of the impending explosion of entitlement spending which remains the real problem.

Imagine what we could be doing if those missing twelve million jobs I referred to last week changed to working people paying taxes instead of sitting on the various government dole programs? Both the number of those on disability (now over ten million) and the number of people on food stamps (48 million) have ballooned to record numbers despite this so-called recovery.

What to Expect This Week

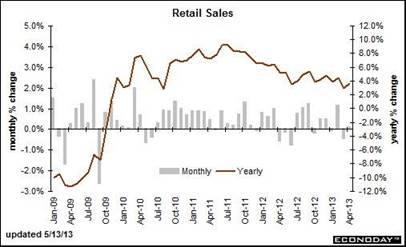

Much more economic data is expected including this morning’s better-than-predicted report on retail sales for the month of April (see chart below). Retail sales grew despite the drop in gasoline prices. This was unexpected and is a good sign for the economy, especially considering people were also paying their taxes last month. This resulted in receipts which were quite strong as evidenced by the lower deficit estimates referred to above.

Thus, the conundrum which is our economy continues. Low claims for initial jobless layoffs and reports such as this morning’s numbers are good, but they are offset by major weakness overseas, a very strong dollar and the increasing burden of government regulatory expense in areas such as health care and energy etc…

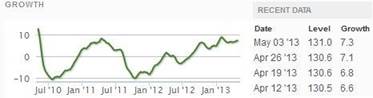

All in all, for the present, the economy to me looks to still have enough momentum to grow, but below trend line. This is confirmed by the lack of upward movement in the weekly report from the Economic Cycle Research Institute’s report on leading indicators (see chart below).

Accordingly, the weekend report in the Wall Street Journal notwithstanding, concerning the Fed’s plans “someday” to change quantitative easing policy - don’t expect any changes. This article is causing some upset this morning, but is merely an attempt by the Fed to discourage speculation (a little late for that). I don’t look for anything to change anytime soon, and expect economic weakness to be the focus over the course of the summer. This means 2013 will look like 2012, 2011 and 2010, which was the year the Obama Administration called the “recovery summer”. It didn’t happen then and it won’t this year either.

![]()

SYMBOL: MRO

Marathon Oil reported first-quarter earnings results that were less than Wall Street’s expectations, due to higher exploration costs and writing down the value of some assets. The Company earned $0.51 per share, as revenues grew by 2 percent to $4.1 billion. The management team maintained its guidance for the remainder of the year.

Even though earnings came in light, oil production volumes rose sharply from last year. The Company reported production of 471,000 oil-equivalent barrels per day, which was a 15.2 percent increase from last year. The operations in the US were much more efficient, helping to offset the problems they have experienced in Libya. We are encouraged by these production numbers and believe they are driving the share price higher.

Shares of Marathon are trading near 52-week highs, and have a conservative valuation. This is one of our top picks in the energy sector, and the shares still yield more than 2 percent. We expect the price of the stock to reach $40 by the end of the year.

![]() Three-Month Chart

Three-Month Chart

SYMBOL: BIIB

Shares of Biogen Idec continue to surge as the Company announced today that the FDA has accepted the Company’s Biologics License Application for marketing approval of ELOCTATE for the treatment of Hemophilia A. This product would reduce the treatment burden on patients, while giving them long-lasting protection. This is a further sign of how strong Biogen’s backlog of potential drugs is currently, which has sent the shares up more than 3-fold in the last several years. We expect growth investors will continue to buy up shares, leading to a $250 price by the end of this year.

Three-Month Chart

© McIntyre, Freedman & Flynn