An Idea Around Disclosure and Something to Consider on Pension Reform

A fair amount was written this week regarding the SEC Cease and Desist Order against the City of Harrisburg (“Order”) and, while certainly not privy to all that was said, we want to take a slightly different perspective. Before getting there, a very brief summation of the Legal Discussion from the Order and the SEC’s Report of Investigation (“Report”).

- SEC found that certain public statements made during a two-year period misrepresented and omitted to state material information regarding Harrisburg’s financial condition and credit ratings downgrades.

- Harrisburg did not provide to the public current and accurate information regarding the City’s financial condition, including annual financial information or notices in accordance with its written undertakings pursuant to Rule 15c2-12 of the Exchange Act.

- SEC brought the action and the resulting Order under the antifraud positions of the SEA and Harrisburg was found to have violated Section 10(b) of the Exchange Act and Rule 10b-5.

Most of you are aware of the underlying facts around the City’s failure to file annual financial information and its failure to timely submit a material event filing around its downgrade from Moody’s. For a comprehensive recitation of the facts, check out the Order (Securities Exchange Act of 1934, Release No. 69515/May 6, 2013).

The report then offers guidance: “municipal issuers should establish practices and procedures to identify and timely disclose, in a manner designed to inform the trading market, material information reflecting on the creditworthiness of the issuer.” The Release sets forth a number of practices to support its guidance but preludes the same with “[a]t a minimum, they should consider adopting policies and procedures that are reasonably designed to result in …” (emphasis supplied by the author).

Now to my point. We have a mechanism that requires the filing of annual financial information or, where the issuer fails to do so, a notice of failure to file. What we do not have is a defined timeframe for when the financial information must be filed. As we all know, the equity markets have such a rule and the failure to adhere to it usually results in severe price movements of the company’s stock.

Recognizing the proponents of more or less regulation each can make valid points and the debate will not be resolved any time soon (akin to the “Tastes Great, Less Filling” debate of year’s past), I take a step back and wonder if there is a way to serve the market and the American tax payer at the same time. As the Executive and Legislative branch grapple with the debt situation, debt ceilings and the budget, we all know the issue of tax exemption has been more than on the table and, based on all the rumors we hear, some limitation appears to be inevitable. Given that reality and the reality that we, as a market, suffer from stale financial information, why not offer up something beneficial to all?

- A defined time by which each issuer or obligor must (not should) file annual financial information after the close of their fiscal year. For example, 180 days (roughly the average for all States and the 50 largest cities).

- Failure to file within the required time will cause the outstanding debt or any debt issued for some time in the future to not be tax-exempt.

Some will argue it is a crazy idea or poke holes. Agreed it is far from perfect. That said, a few points before you take your shots:

- Issuers will be highly incented to maintain their tax-exempt status (think of the cost of borrowing if they don’t comply).

- Institutional and individual investors will be better served by being provided more timely information.

- The market may function more efficiently by rewarding those issuers that are forthcoming versus those that are perpetually late.

While this may not solve some of the problems that Harrisburg faced (ratings disclosure and certain statements) or the totality of the long-term deficit, it may help to solve a long-term issue of a $3.7 trillion market comprised of 54,000 issuers, more than 1.4 million bonds. I welcome your comments and ideas and, with your permission, would be happy to share them in the coming weeks with our readers.

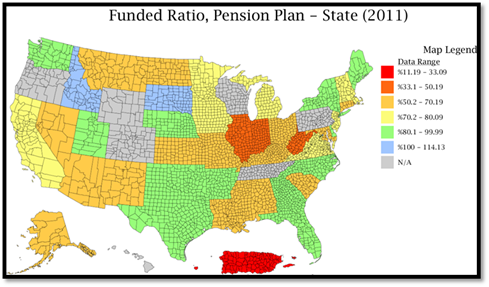

While out on the precipice, I thought I would also jump into the shark-filled pension waters and offer up a few thoughts. In some respects, the issues are similar: timeliness and meaningful disclosure. At least on the pension side we have the implementation of the GASB rules (some argue these rules do not go far enough). However we slice it, the liability is in the trillions and, some argue, absent meaningful change growing to beyond manageable (aren’t some plans already there?). Let’s start with a few reference points.

DIVER Advisor, Map Module; State CAFRs.

You can use your own judgment with regard to what is an “acceptable” funded ratio (blues and greens are north of 80%) and for ARC paid, yellow, green and blue is better than 85% while green and blue are 100% and above.

We have all heard about the bill floating around Congress that seeks to tie the ability to issue tax-exempt municipal debt to the States disclosure of its true cost of their pension plans. Sponsors of the bill said they wanted to send a clear signal that the Federal Government would not bail out municipalities that can’t deliver on their promises. Now putting aside our skepticism on their resolve, one has to applaud their initiative. (We also hope those same legislators take some of their own advice in dealing with the obligations of the Federal Government…)

Here is something to consider. At Lumesis, we track almost 800 pension plans from the States and cities with populations greater than 100,000 (the underlying data is available to our subscribers) and know that many States and cities rely on actuarial figures from the underlying plans that are two or three years old (in some cases older). So, in addition to the funding issue we do have a disclosure issue.

While I am not sure of the answer to resolve the disclosure side of things, I do think a mechanism to require consistent and comparable annual disclosures of funded ratios and critical assumptions would benefit all interested parties – States and cities, bond holders and those promised the benefit down the road. That said, as municipalities consider ways to make changes to plans, where they can or through negotiations with their labor partners, I offer an idea I came across when reading about Sweden. Yes, Sweden (I know, I’m comparing a country to a State or smaller municipality – my point is, let’s get creative to solve problems). Sweden allows its pension obligation/benefit to rise and fall with GDP. Now that may help solve the benefit growth side and just may promote some responsible thinking on the discount rate side as well.

Last Week’s Data :

Weekly Initial and Continued Jobless Claims, State, 4/27/2013

Drought Intensity, County, 5/07/2013

Foreclosures, County and State, April 2013

UPDATED: Muni Index, Pt. in Time/Trend, County, May 2013

On the Road : A light week for us. Mike will be in NYC for part of this week and Gregg will be in Chicago.

Gregg L. Bienstock

CEO & Co-Founder, Lumesis, Inc.

© Lumesis