Executive Summary

- Surging equity markets absent an accompanying rate rally is a red flag, as Treasury yields remain well below “normal”.

- While investors’ renewed enthusiasm for equities is warranted, they must be careful to avoid the “folly of gaming diversification”.

- Corporate earnings have impressed, though revenue has struggled due in part to a moribund Europe.

- Divergent markets mean investors should stay broadly diversified in equities and real bonds — not near-cash — and ever alert to the fundamentals.

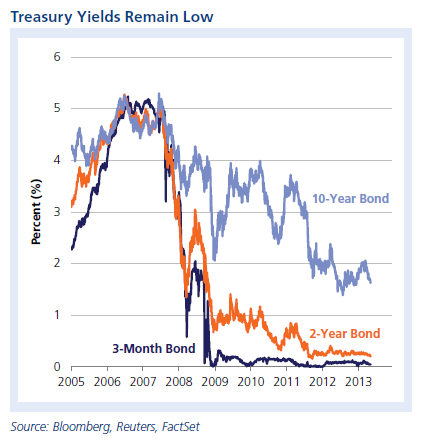

In addition to strengthening fundamentals, a healthy market would at this point include equity prices that were rising in anticipation of economic growth as well as bond yields that were rising in anticipation of reflation that would push rates back to normal. In April, however, we clearly saw rising equity prices but not rising bond yields. This bifurcation represents a tale of two markets — a red flag that should not be taken lightly.

The Death of Bond Prices Appears to Have Been Greatly Exaggerated

Interest rates have been well below normal since the credit crisis. “Normal” can be disputed, but the ten-year Treasury yield historically has been about 4%, so let’s be conservative and say 3.5% is normal. Yields moving back toward 3.5% would be reflation, indicating economic growth without inflation (i.e., the “back-to-normal” trade). All was going well in the first quarter, as ten-year Treasury yields rose above 2%; a bad unemployment report released in early April reversed the trajectory, however, and the ten-year finished the month at 1.67% — ominous indeed.

With this reversal in bond yields, the death of bond prices appears to have been greatly exaggerated. The overwhelming consensus forecast for bonds has been flat wrong, and once again investors have been gamed into dumping their best risk-control asset class in favor of a newfound enthusiasm for stocks. Equities have been on a tear, and investors have been amply rewarded; but as Maverick learned the hard way in “Top Gun”, you never, ever leave your wingman, or disaster may hit when it is least expected.

Bonds are the investor’s wingman, putting up near double-digit returns for the past three years and showing no sign of faltering in 2013, much to the chagrin of the bond bears. Accepting the negative real returns on cash and short-duration instruments has been referred to as “the willingness to get poor slowly”. Gold, while perceived as a great inflation hedge, dropped like a rock, losing its luster as a deflation hedge. If you are wondering how the focus of our fears so quickly switched from inflation to deflation, just look at recent CPI readings, which have fallen well below the Fed’s inflation forecast over the past year, clocking in at an anemic 1.5% year over year.

Investors Have Turned Their Attention to Equities

Investors finally have rediscovered equities; fund flows are positive for the first time in five years. Welcome home and congratulations! Investors are correct to embrace equities as their primary means for building wealth. For those who have delayed getting into equities, now is a good time to move to a normal allocation; despite the markets’ extraordinary run this year and last, equity valuations are still reasonable and near the historical average.

Investors could certainly improve their equity returns by being more broadly diversified. There remains a pronounced lack of diversification within equity portfolios, exemplified by the common error of failing to consider less well-known but better performing categories like U.S. mid cap and global REITs, to name two. It is not only what you own, but also what you don’t own that thwarts wealth creation, especially when those asset classes you don’t own have delivered outstanding returns. These peripheral categories tend to have better track records over longer time periods, with the added advantage of lower correlations to the S&P 500. We have been transparent in pointing out that investors can choose to be invested at their full normal allocations or they can be invested defensively. But to be completely or habitually out of the market is the “folly of gaming diversification”.

The ideal approach to making better investment choices is represented by our Global Perspectives philosophy: “Fundamentals Drive Markets”. So let’s take a look at the current state of the fundamentals.

Market Fundamentals Continue to Be Supportive

U.S. market fundamentals have some natural catalysts that, though perhaps not clearly evident in the mixed statistics we’ve seen of late, have grown increasingly visible. We call these catalysts “Tectonic Shifts”, but before we dive into two of them — new emerging and frontier economies and global trade — let’s look at our ABCDs of underlying fundamentals.

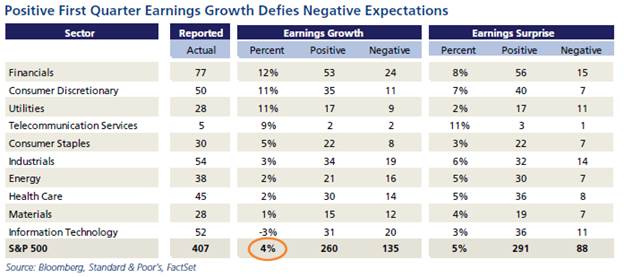

Advancing earnings growth. The tale of two markets is reflected in corporate financials. Corporate earnings growth has surprised on the upside; with 81% of S&P 500 companies having reported first quarter results, the year-over-year earnings growth rate is 4.3%. Revenue growth for those same companies, however, is -0.57%. U.S. corporations are masters of cost cutting, but top-line revenue growth is required for increased growth and profitability over the long-term.

Broadening manufacturing. Manufacturing continues to expand, though its pace unfortunately slowed last month. The ISM manufacturing index posted a 50.7 reading, perilously close to contraction territory. The details of the survey had some brighter spots, though, with current production and new orders both higher. But the employment sub-index fell, basically indicating that little if any employment growth occurred in the sector during April.

Consumer as the game changer. Consumer spending as indicated by retail sales stepped back slightly in March. Perhaps it was a delayed reaction to the expiration of the payroll tax cut, or maybe the impact of sequestration took its toll. On the positive side, gas prices have declined significantly, in effect delivering a substantial tax cut to consumers. And the housing market rebound rages on, providing the economic and psychological boost consumers need to continue spending. Housing prices posted a 9.3% year-over-year increase in February as registered by the S&P Case-Shiller index — the strongest growth rate since 2006.

Developing markets. The PIVOT countries (Peru, Indonesia, Vietnam, Oman and Turkey) represent just a few of the future catalysts for growth that may potentially complement the BRIC (Brazil, Russia, India and China) economies, which have been “emerging” for over 20 years. Trade expansion will continue to fuel growth in these markets, where throngs of younger populations are eagerly awaiting emerging-middle-class consumer status. A trend of “south/south” trade (i.e., trade among developing countries) has emerged, further propelling their growth prospects.

Peru has been hard hit by declining commodity prices this year, as it is the third largest producer of copper and the top producer of silver, but the country is wisely looking to diversify its economy. It was recently reported that Peru is seeking a niche for its handicrafts with trading partner Taiwan, hoping to capitalize on the growing popularity of ethnic-inspired style and fashion overseas by tapping into Taiwan’s gift market.

Global Risks Center on Europe

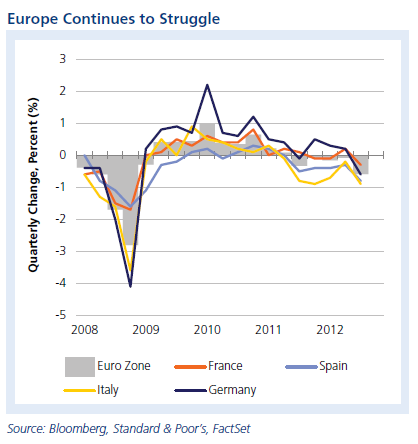

As the year began, our biggest concern was Europe, and our conviction that the euro zone is going from bad to worse has only increased with the release of each economic statistic. No other country exemplifies Europe’s problems better than France. A G-7 country that should stand as a best-practices example for troubled Europe, France has instead become part of the problem.

Witness:

- France has stated plainly that it won’t make its deficit target of 3% of 2013 GDP; its current forecast is 3.7%.

- France is barely skirting recession, contracting 0.3% in fourth quarter 2012 and growing a miniscule 0.1% in first quarter 2013.

- France is intent on raising taxes, punishing its private economy. The government plans around €6 billion ($7.87 billion) of additional taxes in 2014, mostly from increased value-added taxes and corporate income tax increases.

- Unemployment in France last month hit 10.6%, the highest level since the dawn of the crisis and close to record-high levels of 1945.

- The latest trade statistics showed French exports contracted by 2.4% in February, the same ominous pace as in January.

- Increasing political uncertainty — including a Swiss bank account scandal involving France’s budget minister and presidential disapproval readings of 74% — is further darkening the economic vista.

Something positive could be salvaged if other economies in Europe were offsetting the euro zone’s pain, but no such luck. For example, recent reports show the United Kingdom only narrowly avoided slipping into a triple-dip recession during the first quarter, growing a meager 0.15%.

Why does this matter? Because it is showing up in global growth, particularly in U.S. corporate earnings. Europe contributes more than 10% to U.S. sales; given that first quarter revenue growth is currently running negative, it’s easy to see how Europe’s recession matters to the U.S.

The Remedy for the Tale of Two

Markets

We have seen the market climb a wall of worry before, and investors should take note that being on the sidelines when equities relentlessly march forward is folly. Especially when double-digit stock returns persist amid interest rates that are meager and are likely to stay meager for the foreseeable future.

The remedy is to accept both sides of the tale at face value: Remain globally diversified in both equity and fixed income — in real bonds, not near-cash — while remaining ever alert to changes in market fundamentals.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

The opinions, views and information expressed in this commentary regarding holdings are subject to change without notice. The information provided regarding holdings is not a recommendation to buy or sell any security. Fund holdings are fluid and are subject to daily change based on market conditions and other factors.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 6404