Absolute Return Letter: In the Long Run We Are All in Trouble

“The long run is a misleading guide to current affairs. In the long run we are all dead.”

John Maynard Keynes

I often find myself caught between what is appropriate for the short-term vis-à-vis the long-term. Should I allow myself to become captivated by the long-term challenges that we are facing or should I do what the majority of investors seem perfectly happy to do – ignore the long term and focus on the present? Moral deliberations, career risk considerations, greed - you name it – all seem to be factors.

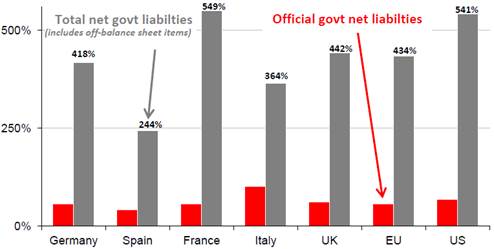

I vividly recall the misfortunes of Tony Dye. Tony was one of Britain’s best known fund managers in the 1990s. As equity markets became more and more expensive towards the end of the decade, he became increasingly adamant that markets were overvalued and began to reduce his equity exposure. In 1999 his firm was 66th out of 67 in the UK equity league tables and in February 2000 he was sacked for poor performance. Within a few weeks of his dismissal, the FTSE peaked and one of the largest bear markets of all times began, all of which taught me a very important lesson – poor timing can ruin even the best investment decisions. All this came back to me after I published a chart in last month’s Absolute Return Letter produced by Albert Edwards and his colleagues at Société Générale (chart 1).

Chart 1: Total Government Liabilities

Source: Societe Generale Cross Asset Research.

Many of you came back to me, asking if this something we have to worry about. More on that later but I would like to start elsewhere. I want to address the question that seems to preoccupy investors more than anything at the moment. Will monetary policy lead to runaway inflation or will it not? There is so much scare mongering going on that it is time to take a deep breath and look at the facts.

Why inflation will remain subdued

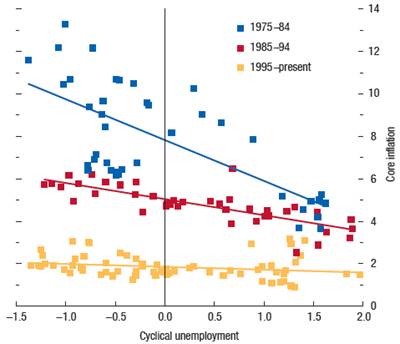

There are at least a couple of reasons why investors in most countries1 shouldn’t worry unduly about inflation in the short to medium term (what will happen in the long term I honestly don’t know). As so aptly demonstrated in a recent IMF paper, the interaction between inflation and the economic cycle is very different today when compared to the 1975-1994 period. Whereas inflation back then was pro-cyclical, it is largely non-cyclical today with inflation well anchored around 2% regardless of the underlying economic conditions (chart 2). The obvious implication of this is that inflation should behave relatively well even as (if) economic fundamentals improve.

Chart 2: Inflation vs. cyclical unemployment

Source: http://www.imf.org/external/pubs/ft/survey/so/2013/res040913b.htm

The other reason has to do with how monetary policy is interpreted - or rather misinterpreted. I have written extensively about this in the past so please refer to some of the older letters for detail. Suffice to say that many investors do not appear to grasp the difference between the monetary base and the money supply and that is indeed a mistake.

Using August 2008 - the approximate time of the Lehman bankruptcy which kick-started the new, more expansive era of central bank policy - as the base (i.e. index = 100), the U.S. monetary base has grown to 347, but the money supply (M2) has only grown to 135. The UK monetary base now stands at 433 with its money supply stuck at 110. In the eurozone, the monetary base is at 157 while the money supply stands at 107. Finally, in Japan, the monetary base is at 150 (and about to go much higher) but the money supply is only at 113 (see here).

At the end of the day, it is the money supply, not the monetary base, which sets the tone for inflation. Another way to illustrate this is by having a glance at QE’s effect on bank lending (chart 3). There has been no growth in bank lending at all despite all the so-called money printing. Investors are quite right in keeping their eye on the ball but, through my lenses, it looks as if they are focusing on the wrong ball.

Chart 3: QE’s effect on bank lending

Source: Nomura Research Institute

The ostrich rules in European banking

As an interlude - because that is not what this month’s letter is principally about - in the short to medium term, I worry primarily about the total state of denial in the European banking sector. Many of our banks are effectively bankrupt but the ostrich principle applies - with the apparent blessing of the authorities. Bury your head in the sand and hope for the problem to go away before anyone notices.

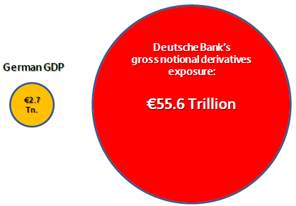

Over the past several months there has been a rather heated debate across Europe as to how far Germany is prepared to go, and should go, to keep the eurozone afloat. I would suggest very far. Here is the reason: Only a few days ago it was revealed that Deutsche Bank’s gross notional deriatives exposure now stands at a whopping €55.6 trillion (not a misprint) – more than 20 times the size of German GDP (chart 4).

Chart 4: German GDP vs. Deutsche Bank’s gross derivatives exposure

Source: Zero Hedge

Many will argue that Deutsche’s net exposure – which is only a tiny fraction of its gross exposure - is what matters, and that is theoretically correct. However, as Zero Hedge points out, the netting out works fine only to the extent the chain is not broken. The moment there is discontinuity in the collateral chain, all bets are off (see here). As many of Deutsche Bank’s counterparties are other European banks, it – and the rest of Germany – simply cannot afford for the European banking industry to come clean.

Despite all of this, I believe the short to medium term outlook is relatively constructive. The scare mongers and the gold bugs – who are more often than not one and the same – want you to believe that the world is coming to an end, which it is not. The U.S. Treasury Department is even planning on making the first down payment on federal debt since 2007. Who saw that one coming?

Here in Europe, the anti-austerity movement has suddenly got some long overdue wind in its sails, following the revelation that Reinhart and Rogoff made some pretty basic mistakes when preaching to the world that national debt in excess of 90% of GDP spells economic mediocrity. Apart from those elementary mistakes, which may or may not be material, Reinhart and Rogoff never distinguished between currency issuers (e.g. the U.S., U.K. and Japan) who can never be forced to default on debt issued in their own currency, and currency users (e.g. the eurozone members), a fact which always made me suspicious of their conclusions, but that is a story for another day.

The long term outlook for equities is bleak

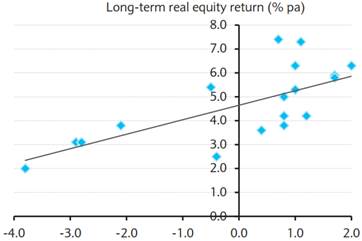

What worries me more is the long-term outlook for equities which I think is mediocre at best, and I base that on two observations. Firstly, it is becoming increasingly obvious to me that we should expect interest rates to stay low for an extended period of time, both on an absolute and a relative basis. I actually expect real rates (measured as inflation-adjusted 10-year bond yields) to remain flat to negative in most G10 countries for several more years to come. Now, what can we deduct from that? Negative real rates are highly unusual and imply that capital is not priced correctly. It is an important indicator of financial repression.

What’s more, real rates are a proxy for trend growth. Negative real rates in a growing number of countries around the world suggest falling trend growth or, at the very least, a drop in expected trend growth. In the past, real rates have also been correlated with equity returns and negative real rates have usually led to low equity returns (chart 5).

Chart 5: The link between real interest rates and equity returns

Source: Barclays Equity Gilt Study 2013

Secondly, I worry a great deal about demographics and the effect they will have on financial markets. The link between demographics and equity valuation is well documented. Barclays researched it in the 2010 edition of the Equity Gilt Study (see here) and the FT picked up on it more recently (see here). The logic is fairly straightforward. In our younger years we save mostly for our children’s education and equities play a lesser role in our portfolios. As the children get older, and we begin to focus on our own retirement, our savings patterns change with equities now dominating our portfolios. Hence the demographic mix is likely to impact equity valuations, and that is precisely what has happened (chart 6).

Now, due to the ageing of society, the big equity buyers (the 40-49 year old) are being outnumbered by the big bond buyers (the 60-69 year old), pushing bond valuations up and equity valuations down. Importantly, that trend is likely to continue for at least another 6-8 years. This observation brings another question about – how much of the recent strength in the bond markets should actually be attributed to various QE programmes and how much is due to demographic factors? Nobody really knows the answer to this question, but I suspect that the significance of central bank policy is overestimated.

Chart 6: The link between savings and equity valuation

Source: “The population conundrum”, Financial Times.

Now back to chart 1. Equity markets have treated us well in the last couple of years but you don’t have to be über-bearish to see that we have to negotiate some pretty strong headwinds in the years to come. Jagadeesh Gokhale produced a noteworthy paper back in 2009 named Measuring the Unfunded Obligations of European Countries (which you can find here). The findings in that study feed straight into chart 1.

The growing age-related liabilities imply that we either need to reform our welfare programmes or the tax rate will have to increase to an average 60% across the EU to meet future obligations. Put slightly differently, the average EU country would need to put aside an amount equivalent to almost 10% of the annual GDP to fully fund future liabilities. Is that going to happen? I suspect not.

Across the Atlantic, the situation is as bad, if not worse. The U.S. payroll tax would have to double from current levels to fully fund future liabilities and each year that the U.S. government takes no action to reduce the projected shortfall, the funding gap grows by more than $1.5 trillion after adjusting for inflation.

The real zombie of Europe

Based on these calculations it is difficult to remain optimistic about the long term. Undoubtedly a solution will be found. It may be that we all have to work until we reach the tender age of 80. Or it may be that state sponsored benefits will be phased out completely and we will all have to rely exclusively on private pension arrangements. I don’t know precisely what the preferred path will be, but I do know that it will be a very bumpy road indeed. Europe has a history of dealing with social change in a very immature way, and the road to the new equilibrium is likely to be littered with social unrest.

France is a prime example of Europe’s self-inflicted hardship. Here are some revealing stats borrowed with gratitude from Gurusblog:

In 1999 France represented 7% of world exports. Today the number is 3%, and the figure continues to fall.

In 2005 France ran a trade surplus amounting to +0.5% of GDP. Today the surplus has turned into a deficit equivalent to 2.7% of GDP.

The total value of French car and machinery equipment sales to China is one-seventh the value of German sales of those same products to China.

In France 42% of wage costs of a company are social charges or taxes. In Germany it is 34% and in the UK 26%.

Since 2005, the total cost of producing a car in France has risen 17%, while in Germany the cost has increased 10%, in Spain 5.8%, and in Ireland 2%.

In France a worker earns on average €35.30 per hour, while in Italy the average is €25.80 and €22.00 in the UK and Spain.

The profits of French companies have fallen to 6.5% of GDP, a level that puts them at 60% of the European average. Lower margins mean less money to invest in new plants or technology leading to a 50% drop in the R&D of French companies over the last four years.

In my book, France is an accident waiting to happen. Unlike countries like Portugal or Spain where there is at least some political appetite for addressing the shortcomings, in France such appetite is virtually non-existing. It is therefore not unreasonable to suggest that the real test for Europe will come when the financial markets finally come around to the inevitable conclusion that France is the real zombie of Europe.

Concluding remarks

Now, you may well deduct from all of this that I am as bearish as I have ever been, but nothing could be further from the truth. The issues I have discussed in this month’s letter are clouds on the horizon which are likely to take years to play out and, in the meantime, investors will continue to be preoccupied with far more mundane issues. All I know is that financial markets cannot stay disconnected from economic fundamentals forever so, ultimately, the Tony Dyes of the world will be proven right. Unless they lost their jobs beforehand, that is.

Niels C. Jensen

8 May 2013

© Absolute Return Partners LLP 2013. Registered in England No. OC303480. Authorised and Regulated by the Financial Conduct Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP ( ARP). ARP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

Absolute Return Partners

Absolute Return Partners LLP is a London based client-driven, alternative investment boutique. We provide independent asset management and investment advisory services globally to institutional investors.

We are a company with a simple mission – delivering superior risk-adjusted returns to our clients. We believe that we can achieve this through a disciplined risk management approach and an investment process based on our open architecture platform.

Our focus is strictly on absolute returns. We use a diversified range of both traditional and alternative asset classes when creating portfolios for our clients.

We have eliminated all conflicts of interest with our transparent business model and we offer flexible solutions, tailored to match specific needs.

We are authorised and regulated by the Financial Conduct Authority in the UK.

Visit www.arpinvestments.com to learn more about us.

Absolute Return Letter contributors:

|

Niels C. Jensen |

Tel +44 20 8939 2901 |

|

|

Nick Rees |

Tel +44 20 8939 2903 |

|

|

Tricia Ward |

Tel +44 20 8939 2906 |

1Some countries are more inflation prone than others, so the following should be read with that in mind. The UK is one such example.

© Absolute Return Partners