Financial markets got the news they wanted last week as Europe cut interest rates, while here at home the Federal Reserve hinted they might do even more when it comes to money printing. To top it off, Friday’s employment report showed improvement from March although the details caused most to discount the excitement.

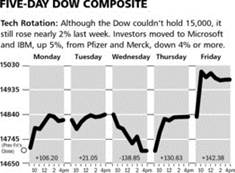

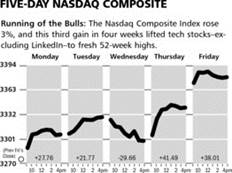

As the charts above illustrate, The Dow Jones Industrial Average gained 1.8%, with many of its component firms increasing their dividendssubstantially. The Nasdaq Composite moved higher by over 3% led by a resurgent Apple share price.

The Markets & Economy

All you really need to know is that if the globe’s central banks continue to think that the economy is struggling then you should not be persuaded by the happy talk emanating from CNBC or elsewhere. Interest rates were reduced in Europe because things are bad. Japan has embarked on its money-printing expedition because of their fear of deflation. Here at home, we remain in the best situation around, but our GDP growth will be lucky to come in at 2% once again this year. The Fed understands this and has vowed to keep interest rates at virtually zero for as far as the eye can see. The Fed has this flexibility since the USA retains the world’s reserve currency and hence a safe haven. Thus there is no credible threat in the near-term to challenge the Fed’s ability to control bond and stock prices.

This continues the paradox of financial markets doing well

while the news headlines remain disappointing or in some cases frightening.

Last week’s unemployment rate showed a nice bounce in the non-farm payroll job creation number. However once again this gain was led by part-time workers which have now reached nearly 8 million people. Explanations are many for this, but the exemption from Obamacare of those working below 30 hours per week is gaining increasing traction.

This trend is also reflected in the decline of the average workweek which, of course, directly feeds into wages earned. Thus the notion of a vibrant employment sector is one that exists only in the minds of CNBC talking heads at this point (and the administration).

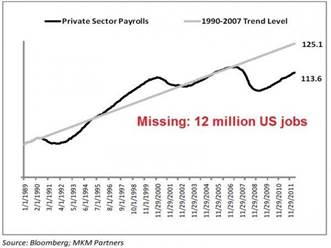

Finally, the chart below shows the long-term trend of private employment in this Country. The USA still has two million fewer private sector jobs than it had in 2008. In addition as the chart shows, given population growth trends, the real job shortfall isnearly 12 million jobs. That explains the reason that nearly 90 million people in this Country are simply no longer counted as unemployed. If they were, the rate would be politically unacceptable.

What to Expect This Week

Unlike last week, the economic data is minimal and earnings season is winding down for the March quarter. Congress comes back into session, but is focusing on immigration reform in the Senate and Benghazi hearings (which may be explosive) in the House.

Accordingly, I expect a quiet week absent international events which also have increased over the past few weeks.

The weekly update from the Economic Cycle Research Institute (see chart next page) showed no change. They think we are already in recession. I think we are muddling along and for many it feels like a recession. The good news though is that gasoline prices are lower heading into the summer season. The bad news is that many states have chosen this time to raise gasoline taxes and thus the consumer may never see the benefits.

![]()

SYMBOL: SWN

Southwestern Energy reported better than expected first quarter earnings results as the price of natural gas continues to head higher. The Company earned $0.42 per share, which was 4 cents better than consensus estimates. Revenues were down 23 percent from a year ago, yet higher natural gas prices will lead to higher revenues going forward. Management was positive on the conference call, and we expect operations to improve over the course of this year.

The Company experienced its highest first quarter cash flow in its history, and we expect that should accelerate in the second half of this year. Southwestern was able to grow its production by 11 percent from the prior year. Management noted that operations improved in both March and April. We believe the Company is undervalued, and the positive trends will lead to a $50 price for shareholders within the next 12 months.

![]() Three-Month Chart

Three-Month Chart

![]()

SYMBOL: DUK

Duke Energy reported solid first-quarter earnings results helped by the cold weather this winter and higher retail electric rates. The Company earned $1.02 per share, which was in line with consensus estimates. The colder temperatures throughout the Company’s region led to a sharp increase in the demand for electricity compared to last year.

The Company is petitioning for higher rates in their region, which should lead to higher margins during the second half of this year. The management team also reiterated what we have been hearing from other companies - that business should improve over the course of the year. Even though the shares have had nice run over the past six months, they still yield over 4 percent. As investors continue to seek high-yielding stocks, we believe the shares will rise to $85 within the next 12 months.

![]() Three-Month Chart

Three-Month Chart

![]()

SYMBOL: SE

Spectra Energy reported better than expected first-quarter earnings results as demand for natural gas increased due to the cold weather. The Company earned $0.51 per share, which was 3 cents better than consensus estimates. Revenues grew by 3 percent from the prior year, although the Distribution Division experienced 12% EBIT growth due to increased demand.

The conference call with investors was the most positive call we have listened to from the Company in several years. Management is currently investing more than $6 billion in expansion projects, and expects to spend more than $25 billion within the next decade. The shares are undervalued at these levels, and are currently yielding nearly 4 percent. We believe this is a very attractive investment at these levels and expect shares to reach $40 within 12 months.

![]() Three-Month Chart

Three-Month Chart

© McIntyre, Freedman & Flynn