Disconnect: Why Stocks and Economy Often Move in Opposite Directions

Key Points

- Many investors are flummoxed by the apparent disconnect between the performance of the economy and the stock market.

- In reality, not only do stocks typically lead the economy; the two can often diverge in the short term.

- Investors need to understand all of the drivers of stock-market performance.

The connection between the stock market and the economy seems obvious. If the latter is performing well, the former should follow. In reality, not only is the opposite typically true—stocks lead the economy—but the two can often appear to be completely disconnected.

Instead of the market and economy being glued at the hip, as many investors assume, it's more like they're tethered at the hip by a fairly long rope. Ultimately they can't get too far apart, but the two can move in different directions—and at different paces—in the shorter term. The trick for investors is to understand the relationship and know how to avoid some common mistakes.

Strong market, weak economy

We recently entered the fifth year of the bull market that began in March 2009, in conjunction with all-time highs reached for both the Dow Jones Industrial Average and the S&P 500® Index. But investors are generally flummoxed, and one of the most common questions I get when I'm on the road talking to clients is, "Why are the stock market and the economy/fundamentals so disconnected?"

I've written and spoken a lot over the years about the relationship between the economy and stocks, but it's worth a refresher. US real gross domestic product (GDP) growth has averaged a relatively paltry 2.1% since the recovery began in mid-2009, yet the stock market is up more than 150% since its low the same year.

Yes, the economy suffered consecutive mid-year slowdowns in 2010, 2011 and 2012, and the stock market behaved poorly during those stretches as well. We're likely in a milder version of a slowdown this year—for the fourth consecutive year. But the stock market has barely blinked, so far.

Before I get to the connection (or perceived disconnect) between stocks and the economy, let me first alert readers to our view that a correction is possible in the near term, although we believe it would be less severe than those of the past three years. And, like then, any correction should ultimately serve as a buying opportunity.

First-quarter GDP—its first estimate reported last week—was weaker at 2.5% than the consensus expectations. Although that's up from a much slower rate of growth during last year's fourth quarter, many find it hard to square with stocks hitting all-time highs during the first quarter. The punch line to the perceived joke is that there's little evidence that GDP in any year reliably correlates with the performance of stocks.

Stocks as leading indicator

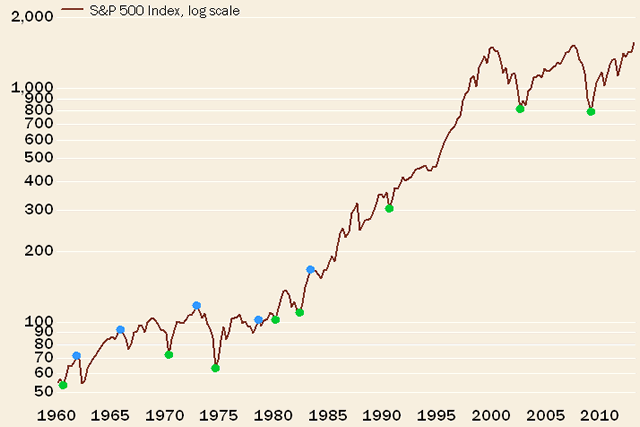

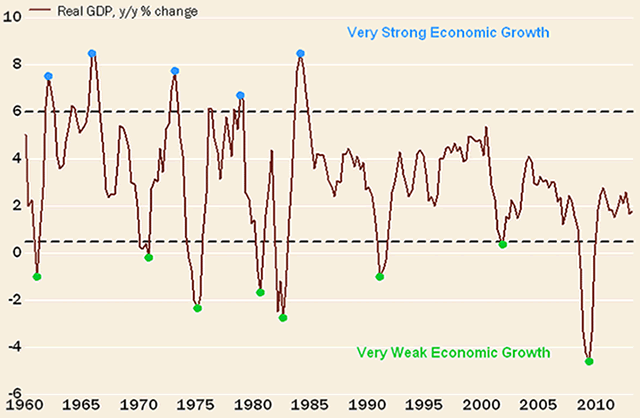

Remember, the stock market (as measured by the S&P 500) is one of 10 sub-indexes in the Conference Board's Index of Leading Indicators. Many investors assume it's the opposite—that economic growth is a leading indicator of the stock market. For a compelling visual of the relationship, see the following pair of charts, which I'll explain below.

Stock Market at Economic Inflection Points

Source: FactSet, as of March 31, 2013. Y-axis of upper chart in logarithmic scale. Y-axis of lower chart represents year-over-year percentage change in US GDP.

The lower chart simply shows the year-over-year rate of change for US GDP. At each trough I put a green dot, and at each peak when growth exceeded 6%, I put a blue dot. (Do note that we haven't had any blue dots since the early 1980s, which I believe is a consequence of the ever-rising burden of debt.)

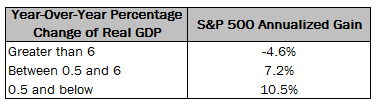

On the S&P 500 chart above, I put the corresponding green and blue dots. What you can see clearly is that the biggest market rallies occur when the economy is weakest, while the biggest sell-offs occur when the economy is booming. A highlight of the details is in the table below.

Source: Ned Davis Research, Inc. Further distribution prohibited without prior permission. Copyright 2013 © Ned Davis Research, Inc. All rights reserved. March 31, 1960-March 31, 2013.

The bottom line is that the stock market, as a leading indicator, tends to launch into rallies and/or corrections around economic inflection points. By definition, a rally-inducing inflection point occurs when economic growth stops falling and begins to rise (green dots), which means GDP growth is at its worst. This is part of why new bull markets can breed rampant skepticism.

A great example of this relationship, and the power of possible inflection points, was the performance of Greece's stock market last year. The country's economy is in a near-depression amid its debt crisis, yet the Athens Stock Exchange was the best-performing stock market within the European Union in 2012—up more than 33%!

Other factors come into play for stocks

Not only is there a timing issue to consider; it's also the case that factors other than economic growth have a significant impact on stock-market returns. Earnings growth and valuation are two of those factors, but even here the connection can appear disconnected at times.

As my friend Larry Kudlow has often said, "Earnings are the mother's milk of stock prices." But is it always true in the short-term? I ask the rhetorical question because many investors are wondering why stocks have continued to perform well in the face of slowing earnings growth.

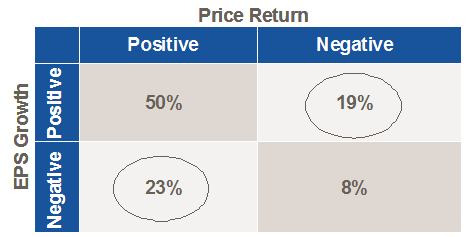

As the grid below (courtesy of our friends at Strategas) shows, 42% of the time over the past 62 years, stock prices and earnings have moved in opposite direction in any given year. While prices generally track earnings closely over the long term, year-to-year divergences can be significant.

Source: Strategas Research Partners LLC, as of December 31, 2012.

So, what are the factors that can drive stock prices other than economic or earnings growth?

- Valuation is a major determinant of stock-market returns. An economy with high GDP growth is likely only a good investment opportunity if stock valuations are low. And even an economy with low GDP growth can provide good stock returns if the market is reasonably priced. The current trailing P/E on the S&P 500 is about 16, slightly below the long-term median of 18. In addition, valuations tend to be greater than long-term norms when inflation is less than 4% (it's presently less than 2%). This suggests valuation could expand further without heavy lifting by earnings.

- History shows that it's often economic surprises—good or bad—that matter more than the absolute level of growth. An economy that's performing better than low expectations, even if that growth is relatively weak, can often be accompanied by a rising stock market. As John Kenneth Galbraith once said, "The only function of economic forecasting is to make astrology look respectable."

- As coined by my first boss and mentor for 13 years—the late, great Marty Zweig—"Don't fight the Fed." The Federal Reserve has pushed interest rates so low that many savers are being pushed from cash vehicles and US Treasuries into stocks in search of both income and capital gains. In fact, relatively tepid growth has been good for the stock market in the past—and will likely remain so, as it will keep the Fed's foot on the accelerator while keeping inflation at bay.

I'll conclude with one final force that the stock market can have going for it. Bull markets can be self-perpetuating: as prices go up, more people want to buy. This has clearly been a force during this bull market, and it isn't likely to change, notwithstanding our view that a pullback is increasingly likely.

Important Disclosures

The information provided here is for general informational purposes only and should not be considered an individualized recommendation or personalized investment advice. The investment strategies mentioned here may not be suitable for everyone. Each investor needs to review an investment strategy for his or her own particular situation before making any investment decision.

All expressions of opinion are subject to change without notice in reaction to shifting market conditions. Data contained herein from third party providers is obtained from what are considered reliable sources. However, its accuracy, completeness or reliability cannot be guaranteed.

Examples provided are for illustrative purposes only and not intended to be reflective of results you can expect to achieve.

© Charles Schwab

![]()

![]()

![]()

![]()