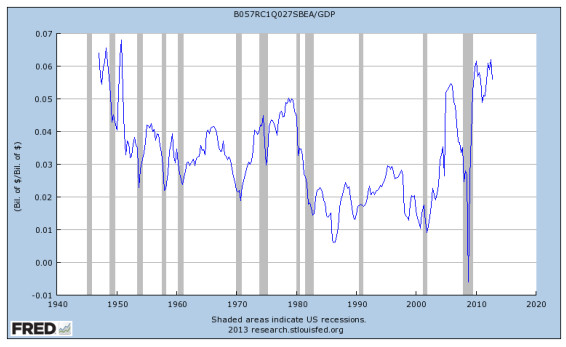

The current earnings season is a very mixed bag. Start with the economic background where nominal growth decelerated in 2012 from around 4.4% to 3.6%. The first quarter may be marginally higher but some of that is from a low base effect. It’s very difficult for companies to raise prices, increase share or volumes when demand is simply deficient. Sure, balance sheets are in much better shape, as evidenced by robust bond issuance, but many companies are in excess savings mode. Here are undistributed corporate profits as a percent of GDP.

Source: Federal Reserve Bank of St. Louis, Economic Research

Companies have three choices when it comes to profit: i) spend it, which is the same as reinvesting in the business ii) distribute it in the form of dividends or share buy backs or iii) save it. They have clearly been in “save” mode and gradually passing into “distribute” mode. But what we’re not seeing is a lot of “spend.”

In this season, sales growth is around -0.4% and earnings growth at 1.6% for half of the S&P[1] companies reporting so far. These compare to 3.6% sales growth and 9.2% earnings growth last quarter. This is why the market has little tolerance for any misses even after expectations were revised down. The price action for an earnings miss last quarter was +/- 0%. Now it’s around +/-2%.

Companies are at least increasing dividends faster than earnings which means the all important dividend yield on the market is holding up well. Say it again, some 40% of long-term stock returns comes from dividends. We got into the craze for share buybacks some years ago and that still permeates the market. But dividends are what counts.

Overall we are encouraged by: consumer spending, some wage growth, housing and a rollover in oil and gas prices. Claims are reasonably strong, although they tell only half the employment story. You still need someone to hire the other side of the claim to arrive at employment growth. So this means QE remains in place. The hawks are i) pressing on asset price inflation ii) extremely uncomfortable with both the unemployment mandate and iii) QE buying. The only people that count are Bernanke, Yellen and Dudley. QE will continue until they see “substantial improvement” in the labor market.

Curious Fact: All last week we saw index futures rally first thing pre-opening. The S&P 500 futures for June settlement rallied 15 to 20 points in the two hours before opening regardless of some major earnings disappointments from the night before. What this suggests to us is that investors are working hard to gain exposure to the biggest, most liquid names as an asset class, not necessarily for the idiosyncratic risk. This might be foreign buying, foreign central banks, some arbitrage between stocks paying over 2.3% on forward estimates, compared to 1.7% on treasuries or just a desire to not miss rallies and upsides. For now, take it that the market remains well bid.

Sources: Bloomberg, Capital Economics, Federal Reserve Bank of St. Louis, High Frequency Economics, Federal Reserve Board, ISI, Pantheon MacroEconomic Advisors, Sentinel Asset Management, Inc.

[1] Standard & Poor's 500 Index is an unmanaged index of 500 widely held US equity securities chosen for market size, liquidity, and industry group representation. An investment cannot be made directly in an index.

© Sentinel Investments

http://www.sentinelinvestments.com