The Return of the Asian Tigers: Guinness Atkinson Asset Management Asia Brief

Often overlooked by international investors, South East Asia encompasses some of the world’s best performing equity markets in recent years, putting the more established emerging markets in the shade. This performance is backed by good economic results and the favourable demographics of some of these countries, with youthful populations ready to improve productivity and increase consumption. One catalyst for future growth is the Association of Southeast Asian Nations (ASEAN) free trade area, which will bring down trade barriers between the South East Asian nations. ASEAN captures the essence of Asian growth and it has the potential to be one of the investment success stories of the coming decade.

|

|

- Return of the Asian Tigers

- Market Review

- China Economic Monitor

The Return of the Asian Tigers

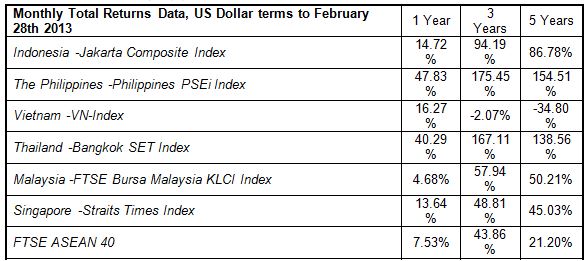

The South East Asian markets (Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand and Vietnam) have been the stealth success of the post-financial crisis world, and the good returns from equities there (see table 1) reflect the essence of the Asian investment story. At a time when investors are worried about financial repression in China and institutional incompetence in India, the South East Asian nations are a credible emerging markets growth option. In 2012 Indonesia, the Philippines and Thailand all grew their GDP more than 6% in real terms, while Malaysia managed a creditable 5.6% growth.

|

|

Sources: Bloomberg, Guinness Atkinson Asset Management

Today’s South East Asian story should be familiar to all emerging markets investors – a compelling combination of young populations, rising urbanization and growing industrialization. Add to the recipe a growing middle-class population with the ability and desire to consume more, decent sovereign balance sheets and stable politics, and the dish becomes very appealing.

What is perhaps not fully appreciated by investors is the scale of the opportunity in South East Asia. ASEAN accounts for less than a quarter of the MSCI Far East ex Japan, so investors looking at the leading Asian benchmarks will likely struggle to get good exposure to this theme. Growth in North Asia has slowed in recent years, and a slowdown there could be ASEAN’s opportunity. Rising wages in China has also encouraged firms to invest in Vietnam, the Philippines and Indonesia.

The case for the Tigers

If China is approaching the end of its hyper-growth period, ASEAN could be just entering its. ASEAN numbers ten member states, which mostly remain well behind the EU and NAFTA in terms of economic development and output, but with a favorable mix of relatively low indebtedness and economic growth momentum. Similar demographics to those which helped to make China an attractive investment ten years ago are now coming into play in some countries in South East Asia. In Indonesia and the Philippines the age structure of the populations means that the working populations are likely to grow relative to their dependent populations for some years to come. These are not trivial changes with under-14s accounting for 27% of Indonesia’s population of 231 million people and 35% of the Philippines population of 92 million people.

The framework for future growth is the AEC – the ASEAN Economic Community, which is a single market which should come to fruition by 2015. The aims of the project are modelled on the European Union’s single market:

- Free movement of goods, services, investment, skilled labor and a freer flow of capital

- Zero tariffs and integrated customs procedures

- A single market and production base

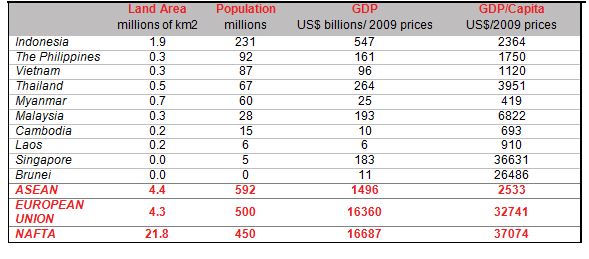

ASEAN stands comparison with the EU and NAFTA (North American Free Trade Area) on land mass and population (see table 2), and it has a good natural resources endowment with oil, natural gas, coal and palm oil readily available. Most of these nations have lower wages than China and are happy to attract the activities which other Asian nations are actively trying to shed as they move up the value chain. Electronics assembly and textiles stand out as two industries in which Thailand, Malaysia and Vietnam have gained ground over North Asia in recent years. There is a developing middle class consumer base, especially in Thailand, Malaysia and Indonesia, and this is being reflected in rising sales of property, particularly smaller ‘starter’ homes and cars.

|

|

Sources: CIA World factbook, Eurostat, ASEAN, IMF, OECD, Population Reference Bureau, Bloomberg

So far, the ASEAN nations’ exports have principally gone outside of the trade block, but with tariffs and restrictions coming down it is natural for the nations to trade more with each other. This is a huge opportunity and one for which individual companies are already preparing, particularly in sectors such as autos where parts can be easily shipped for assembly elsewhere. This also makes the ASEAN nations more dependent on each other’s organic growth and less on the vagaries of growth in the developed world. The political situation in these countries is also better than it has been for many years, with even the ‘closed’ nations, such as Myanmar, starting to open for business.

Two projects illustrate the huge growth potential in ASEAN:

Iskandar Development Region, Malaysia

Iskandar is Malaysia’s attempt to create an economic hinterland for Singapore to mirror the symbiotic success of Shenzhen and Hong Kong. The region covers an area three times the size of Singapore and the Malaysian government is offering grants, tax breaks and favourable planning rules to attract investment. Iskandar offers lower cost housing, a well-educated workforce, a modern airport and a cargo port to benefit from overspill economic activity from Singapore.

Bangkok’s infrastructure boom

As the AEC develops, the leading cities in South East Asia are lobbying to become the ‘capital’ of ASEAN. Bangkok is investing heavily in infrastructure to achieve this status, and the centerpiece is a huge extension to its metro system. The city’s development has been hampered by its congested road network, and the city of 14 million people plans to add 12 new lines to take its 79km of track to 508km by 2029. 10 of the 12 lines are scheduled to be completed by 2017.

Setting aside the niceties of the economic outlook, we believe ASEAN shapes up nicely as an investment today. For portfolio construction the divergences between the ASEAN markets offer a portfolio balance between the more developed markets such as Singapore, Malaysia and Thailand and the potentially higher growth ‘frontier markets’ such as Vietnam and Myanmar. The improved liquidity of their equity markets also makes them investable for institutions in a way they were not even a few years ago.

The improving sovereign debt ratings also support a lower cost of capital in these economies and create the conditions where firms can borrow and invest at a reasonable cost in local currencies, rather than having to look overseas for liquidity. There is also a good degree of currency diversification between the nations, and monetary policy can be tailored to each country, avoiding the monetary ‘balloon squeeze’ which has afflicted China.

ASEAN captures the essence of Asian growth and it has the potential to be one of the investment success stories of the coming decade.

Market Review

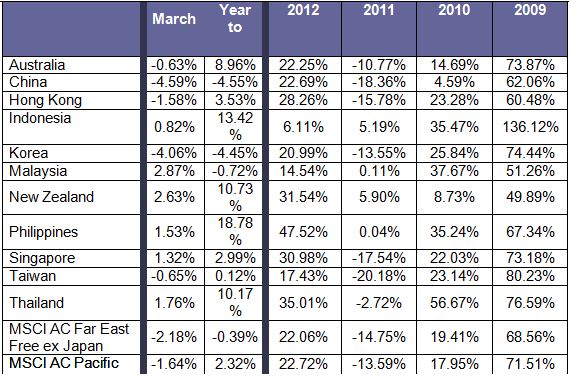

Market Performance Ending March 30th, 2013

*MSCI AC Pacific includes Australia & New Zealand (MSCI Indices were used for regional & individual market performance)

March was a choppy month for Asian equities with very weak performances from China and South Korea, while a number of South Asian markets finished the month in positive territory. Due to the high weightings of China and South Korea in the benchmark indices, the overall indices were down for the month.

China was the weakest market in March, and is now down for the year to date, following a reasonable start to the year. Since Chinese New Year there have been renewed worries about the pace of economic growth in China, and it seems that the recovery is not on as firm a footing as had been hoped. In addition, there are early signs that inflation is beginning to pick up again, and renewed controls have been proposed to curb price rises in the property market. Beijing has implemented a rule to prevent single-person households from owning more than one property, and plans to enforce a 20% capital gains tax on property. Equity investors have been concerned that other cities will follow suit but so far no other curbs have been announced.

South Korea was also weak this month as a result of renewed political concerns about North Korea, which have provoked the US administration to move a missile defence system to the region to protect its interests in Guam. Japan’s renewed desire to carry out aggressive quantitative easing has also hung heavy over the export-led South Korean equity market, as such a policy could lead to further weakening of the Japanese Yen, and make South Korean products relatively less competitive.

The top performing market in March was Malaysia, which has recovered despite concerns about government policies following the forthcoming general election. Parliament was dissolved by the Prime Minister Najib Razak on April 3rd and the election must be held before June 27th.

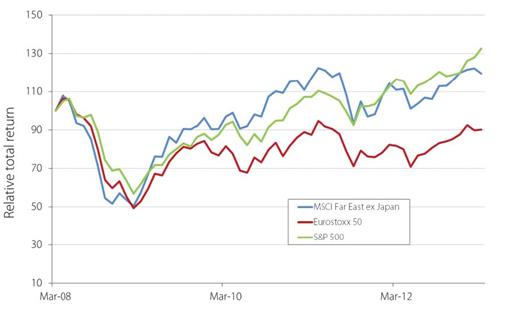

The S&P 500 equity index remains ahead of the MSCI Far East ex Japan over the previous five years, although European equities are still well behind over the period.

![]()

|

|

Source: Guinness Atkinson, Bloomberg

China Economic Monitor

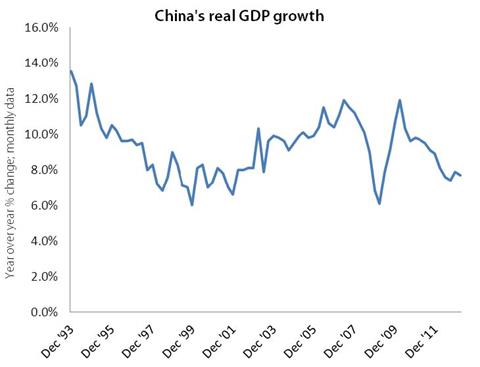

China’s real GDP growth decelerated slightly in the first quarter of 2013, rising 7.7%, compared to growth of 7.9% in the fourth quarter of 2012. While this is a good result in terms of the speed of growth relative to the size of the economy, it is a slight disappointment to the equity market. It was hoped that the improving growth momentum could be maintained from the second half of 2012, but this has not been the case so far this year.

The underlying data yield a mixed picture of growth in the Chinese economy, but few of the metrics we track indicate a sharp recovery in growth. Fixed asset investment (FAI) has held up well in the first quarter of the year, with urban fixed asset investment growing 20.9% in March 2013 compared to the same month of 2012. This is in line with 2012’s results for monthly growth in FAI, which were typically between 20% and 21%. Electricity production partially recovered, growing 2.1% in March 2013 compared to the same month of 2012. This is slower than the mid-single digit growth of electricity production during 2012, but it improved on a sharp contraction in February of 2013. Construction activity was buoyant, with floor space under construction growing 14.7% year over year in March 2013, the best monthly result since June 2012.

On the negative side, freight activity continues to be sluggish, with million ton kilometers of freight growing only 5% year over year in February 2013, compared to typical growth in the teens over the last two years. The weakness is also reflected in slow growth in passenger kilometers, with no sign of recovery back to the growth rates achieved in 2010 or 2011.

|

|

Source: National Bureau of Statistics, Bloomberg

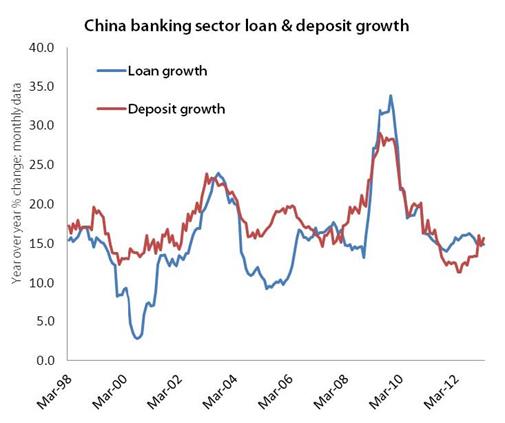

The growth rate in deposits in the Chinese banking system has continued to improve, reaching 15.6% year over year in March 2013. This is significant as it suggests that the banks are being successful at attracting back deposits which might otherwise have gone towards wealth management products or to shadow lending. This is a particular surprise given there has been little change in headline interest rate policy in recent months, suggesting that consumer behavior is starting to change, perhaps in line with increased warnings about the risks of shadow banking. Loan growth has slowed marginally, down to 14.9% year over year in March. This should still be a comfortable level of lending growth relative to real GDP growth of 7.7%.

The macro numbers suggests that liquidity is available to borrowers, and this is confirmed by the new lending figure in March of CNY 1060 billion, which is good relative to the first quarter loan growth in the last two years. It also suggests that the banks’ composite loan to deposit ratio has fallen slightly over the last quarter, which should be good for the overall health of the financial system.

|

|

Source: National Bureau of Statistics, Bloomberg

Although there has been some pick-up from since the end of 2012, inflation seems to remain under control, perhaps offering some headroom to policy-makers for more pro-growth monetary policies. Year over year growth in the headline consumer price index (CPI) was 2.1% in March, while non-food CPI grew 1.8% and food CPI was up 2.7%. There is some disconnect between the headline figures and the detailed numbers with falls in both fresh vegetable and wholesale pork prices in recent weeks. The producer price index (PPI) remains in contraction territory, with overall producer prices falling 1.9% year over year in March. While this is good for consumers, it suggests that perhaps demand is not as strong as it could be and that some firms may have little pricing power at present.

|

|

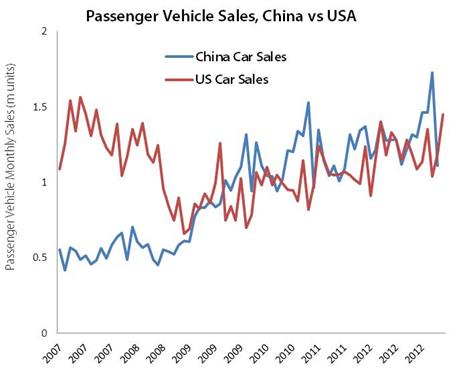

Chinese car sales fell back markedly in February to 1.1 million units, following an exceptionally strong January when 1.7 million units were sold. The pullback was most marked in basic passenger vehicles, which fell to sales of 750k in February compared to an historically strong 1.2m units in January. By contrast, auto sales in the US rebounded well in March 2013, with 1.5 million vehicles sold during the month. The mixed performance of passenger cars sales in China also reflected weaker sales of commercial vehicles in February, with 177k vehicles sold compared to 225k in the previous month.

|

|

Source: China Automotive Information Net, Bloomberg

Performance data quoted represents past performance and does not guarantee future results. Index performance is not illustrative of Guinness Atkinson fund performance and an investment cannot be made in an index. For Guinness Atkinson Fund performance, visit gafunds.com.

Mutual fund investing involves risk and loss of principal is possible. Investments in foreign securities involve greater volatility, political, economic and currency risks and differences in accounting methods. Non-diversified funds concentrate assets in fewer holdings than diversified funds. Therefore, non-diversified funds are more exposed to individual stock volatility than diversified funds. Investments in smaller companies involve additional risks such as limited liquidity and greater volatility. The Fund may invest in derivatives which involves risks different from, and in certain cases, greater than the risks presented by traditional investments.

The MSCI All Country Far East Free ex-Japan Index (MSCI AC Far East free ex-Japan Index) is a free float-adjusted, capitalization-weighted index that is designed to measure equity market performance in the Asia region excluding Japan. The Index is made up of the stock markets of China, Hong Kong, Indonesia, Korea, Malaysia, Philippines, Singapore, Taiwan and Thailand.

The MSCI All Country Pacific Free ex-Japan Index (MSCI AC Pacific Index) is a free float-adjusted, capitalization-weighted index that is designed to measure equity market performance in the Pacific region. The Index is made up of the stock markets of Australia, China, Hong Kong, Indonesia, Korea, Malaysia, New Zealand, Philippines, Singapore, Taiwan and Thailand.

The S&P 500 Index is a broad based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general.

The STOXX Europe 50 Index (STXE 50), Europe’s leading Blue-chip index, provides a representation of supersector leaders in Europe. The index covers 50 stocks from 18 European countries: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Iceland, Ireland, Italy, Luxembourg, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland and the United Kingdom.

The Hang Seng Index is a market capitalization-weighted index of 40 of the largest companies that trade on the Hong Kong Exchange.

The Jakarta Stock Price Index is a modified capitalization-weighted index of allstocks listed on the regular board of the Indonesia Stock Exchange.

The Philippine Stock Exchange PSEi Index is a capitalization-weighted index composed of stocks representative of the Industrial, Properties, Services,Holding Firms, Financial and Mining & Oil Sectors of the PSE.

The Bangkok SET Index is a capitalization-weighted index of stocks traded on the Stock Exchange of Thailand.

The FTSE Bursa Malaysia KLCI Index comprises of the largest 30 companies by full market capitalisation on Bursa Malaysia’s Main Board.

The Straits Times Index, calculated and disseminated by FTSE, comprises the top 30 SGX Mainboard listed companies on the Singapore Exchange selected by full market capitalization.

CIMB FTSE ASEAN 40 is an open-ended exchange-traded fund registered in Singapore.

The FTSE 100 Index is a capitalization-weighted index of the 100 most highly capitalized companies traded on the London Stock Exchange.

brief

The Vietnam Stock Index or VN-Index is a capitalization-weighted index of all the companies listed on the Ho Chi Minh City Stock Exchange.

Consumer Price Index (CPI) is a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food and medical care.

Producer Price Index (PPI) is a family of indexes that measures the average change in selling prices received by domestic producers of goods and services over time.

One cannot invest directly in an index.

This information is authorized for use when preceded or accompanied by a prospectus for the Guinness Atkinson Funds. The prospectus contains more complete information, including investment objectives, risks, fees and expenses related to an ongoing investment in the Funds. Please read the prospectus carefully before investing.

Opinions expressed are subject to change, are not guaranteed and should not be considered investment advice.

Distributed by Quasar Distributors, LLC.

© Guinness Atkinson Asset Management