Understanding where we are in the an important aspect of investing, as the behavior of asset classes may vary throughout that cycle. Recent data indicate that the U.S. remains in its fourth year of expansion, but payroll and retail numbers have disappointed. Outside the U.S., Europe continues to be mired in recession while China’s growth rebound recently has appeared to sputter. In this edition of Strategic Spotlight, we review what these developments mean for the global business cycle and how to position portfolios accordingly.

Monitoring Business Cycle Phases

Investors generally think of a business cycle as including the following phases: early recovery, mid-cycle expansion, late-stage growth and, finally, contraction/recession. Understanding how different asset classes perform in various stages of the economic cycle is a critical component of tactical asset allocation. Risk assets such as equities, for example, historically perform well in the early to mid-cycle stages; commodities generally perform well closer to the end of a business cycle; and Treasuries tend to outperform during a recession as risk aversion spikes.

The ability to position a portfolio appropriately in view of the economic environment can potentially contribute to excess returns. The catch is that observing the business cycle in real time is easier said than done, as GDP data are usually released infrequently and with a lag. Therefore, investors generally need to rely on a host of more timely indicators, such as business survey results, to paint a better picture of where an economy is headed.

U.S.: Mid-Cycle Growth Is Intact

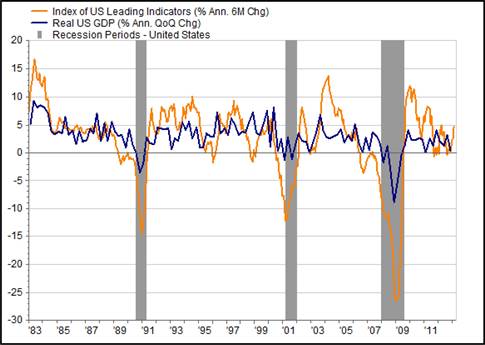

The U.S. economy is currently in a mid-cycle expansion stage. Equity markets have performed solidly this year as signs of economic growth appear to be gaining momentum. Recently, we’ve seen an uptick in the housing market and a boom in domestic energy, while employment continues to grow. The resolution of the fiscal cliff early this year averted a self-inflicted injury to the economy, allowing growth momentum to continue. The index of U.S. Leading Indicators—made up of 10 economic components that historically have had strong predictive power on GDP growth—also appears to confirm that growth remains intact (see display).

LEADING U.S. ECONOMIC INDICATORS POINT TO STABLE GROWTH

Source: FactSet (data through March 2013)

Nevertheless, recent signs are causing concern. The delayed effects of payroll tax changes and fiscal contraction through sequestration have appeared to surprise investors. Business confidence has also waned as uncertainty over the potential impact of reduced government spending on corporate hiring decisions. However, we believe that, as in years past, growth momentum will likely be sufficient to offset weakness in government spending this year and allow the country to stay on course.

Europe: Recession Lasts Longer than Expected

Hopes at the end of last year for a quick rebound in Europe proved brief as most

economies there have remained in recession. Germany and other core eurozone countries are faring better than peripheral nations but continue to be in economic contraction mode. Still, there are signs of gradual improvement. For example, recent data indicate that consumer and business confidence in Germany has turned the corner, making it likely, in our view, that the country will again lead Europe out of the recession. Other large nations in the eurozone, such as France, Spain and Italy, remain in poor shape in the face of ongoing austerity measures.

However, gradual improvement is expected as troubled countries carry out structural changes to make their respective economies more competitive and begin to consider stimulus measures to ignite growth. While monetary policy will remain accommodative as inflation stays benign, policy uncertainty may impact confidence and delay growth. The consensus expectation is for the eurozone to exit the recession by year-end, although the risk remains that sluggish growth may persist.

Asia: Early Recovery Amid Structural Changes

China, which has been a key driver of global growth, has not experienced negative year-over-year GDP growth since quarterly numbers were first published about 20 years ago. In that sense, the slowdown to 7.4% in the third quarter of 2012 appears to be one of the closest things to a recession the country has experienced—and not much over the 6.6% experienced during the 2008–2009 global financial crisis. In the first quarter of 2013, China’s growth reaccelerated to 7.7%, an indication of a rebound but also that the country’s performance remains below expectations. A Chinese recovery is potentially significant given its ability to invigorate many other emerging nations, ranging from export-focused economies (Korea, Taiwan) to commodity producers (Brazil). However, many investors are concerned that, despite entering into a recovery phase, China will struggle to achieve higher growth levels given the structural problems that are plaguing the country.

Japan made headlines in recent months as a more activist government and central bank came into power. The Bank of Japan’s resolution to target inflation of around 2% is expected to inject about $1.4 trillion into the economy over a two-year period. The liquidity injection has already had a palpable effect on the yen and Japanese equity market, and we believe that Japan could exit the recession with low but positive growth. However, to sustain growth over the longer term, monetary intervention would need to be followed by fundamental changes to address the country’s competitive weakness.

Supportive Backdrop for Risk Assets

Global growth appears to be in the trough of a short slowdown and, in our view, will likely rebound gradually throughout 2013. Unlike 2008–2009, the recent deceleration has not been a synchronous one, and the majority of markets are still in expansion mode. Despite the recent spate of poor data, the U.S. appears to be in the mid-cycle growth phase supported by improvements in housing, while Europe remains mired in recession with the prospect of entering early stage recovery later in the year. Asia (particularly China), which has been a major driver of global growth, is in the process of emerging from a particularly slow period, but structural headwinds could prevent it from reaching the heights of the past.

Despite near-term volatility associated with a potential soft patch in the U.S. during the spring and continued political uncertainty in Europe, we believe the global backdrop should remain favorable for investing in risk assets, particularly for regions in early to mid-cycle growth, as corporate earnings growth and multiple expansions could both drive returns.

This material is provided for informational purposes only and nothing herein constitutes investment, legal, accounting or tax advice, or a recommendation to buy, sell or hold a security. The views expressed herein are generally those of Neuberger Berman's Investment Strategy Group (ISG), which analyzes market and economic indicators to develop asset allocation strategies. ISG consists of five investment professionals who consult regularly with portfolio managers and investment officers across the firm. Information is obtained from sources deemed reliable, but there is no representation or warranty as to its accuracy, completeness or reliability. All information is current as of the date of this material and is subject to change without notice. Any views or opinions expressed may not reflect those of the firm as a whole. This material may include estimates, outlooks, projections and other "forward-looking statements." Due to a variety of factors, actual events may differ significantly from those presented. Investing entails risks, including possible loss of principal. Indexes are unmanaged and are not available for direct investment. Past performance is no guarantee of future results.

This material has been issued for use by the following entities; in the U.S. and Canada by Neuberger Berman LLC, a U.S. registered investment advisor and broker-dealer and member FINRA/SIPC; in Europe, Latin America and the Middle East by Neuberger Berman Europe Limited, which is authorised and regulated by the UK Financial Services Authority and is registered in England and Wales, Lansdowne House, 57 Berkeley Square, London, W1J 6ER; in Australia by Neuberger Berman Australia Pty Ltd (ACN 146 033 801, AFS Licence No. 391401), which is licensed and regulated by the Australian Securities and Investments Commission to deal in, and to provide financial product advice for, certain financial products to wholesale clients; in Hong Kong by Neuberger Berman Asia Limited, which is licensed and regulated by the Hong Kong Securities and Futures Commission; in Singapore by Neuberger Berman Singapore Pte. Limited (Company No. 200821844K), which currently operates under an exemption from licensing under the Financial Advisers Act (Chapter 110) of Singapore for marketing of collective investment schemes to institutional investors; in Taiwan by Neuberger Berman Taiwan Limited, which is licensed and regulated by the Financial Services Commission ("FSC") to deal with specific professional investors or financial institutions for internal use only, and which is a separate entity and independently operated business, with SFB operating licence no.:(101) FSC SICE no.008, and address at: 11F, No. 1, Songzhi Road, Taipei, Telephone number: (02) 87292308; and in Japan and Korea by Neuberger Berman East Asia Limited, which is authorized and regulated by the Financial Services Agency of Japan and the Financial Services Commission of Republic of Korea, respectively (please visit https://www.nb.com/Japan/risk.html for additional disclosure items required under the Financial Instruments and Exchange Act of Japan). Except for the foregoing, this material is not intended for use or distribution within or aimed at the residents of any other country or jurisdiction. This document is not an advertisement and is not intended for public use or additional distribution in the following jurisdictions: Brunei, Thailand, Malaysia and China.

The "Neuberger Berman" name and logo are registered service marks of Neuberger Berman Group LLC. Neuberger Berman LLC is a Registered Investment Advisor and Broker-Dealer. Member FINRA/SIPC.

N0121 4/13 © 2013 Neuberger Berman LLC. All rights reserved.