The 5% Problem: Double Jeopardy for Traditional Bond Investors

A conversation with Nathan Rowader,Forward Director of Investments & Senior Market Strategist

Exactly what is the 5% problem? And why should investors be concerned about it?

The 5% reference is to the historical average annual yield for traditional bonds— that is, U.S. government bonds, including Treasury notes and bonds—from the beginning of 1926 to the end of 2012.1 The problem is that investors have grown accustomed to earning those kinds of yields, or better, from bond investments that carry little or no risk of default, such as U.S. Treasurys. But over the last couple of years, yields have been in the zero-to-2% range and the risks of bond investing have risen sharply.

So you could say it’s a time of double jeopardy for bond investors. First, they need to worry about finding the kinds of income streams they need to keep their financial plans and retirement on track. But they also need to be aware that their portfolios may be exposed to a level of risk that is far out of proportion to the income that traditional bonds are generating. Many investors still think of traditional bonds as “safe” when that may not be the case at all.

What has changed? Why do you believe the bond market climate has become so much riskier?

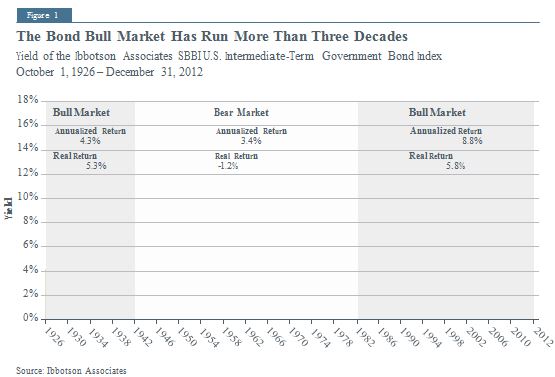

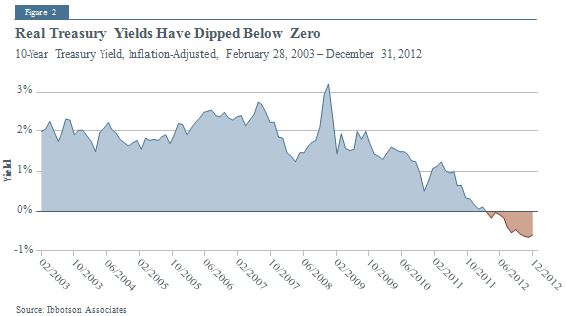

We’re now more than three decades into the bull market for bonds. That means bond prices have been rising while yields have been steadily dropping—those two factors always move in an inverse relationship, as most investors know. When the bull market started, back in 1981, the annual yield from a traditional bond index was in the neighborhood of 14.8% (Figure 1). If you look at 10-year Treasurys now, they’re yielding less than 2% in annual income, and if you adjust that yield for inflation, it has actually dipped below zero (Figure 2).

Because bond prices have been rising, total returns have been good, averaging 8.8% annually over about the last three decades, and 5.8% over the past 10 years. That performance has lulled investors into feeling they are on solid ground with traditional bond investments.

It is critical to recognize, however, that traditional bonds’ ability to deliver positive real returns over the past 30 years has been due in part to the steady rise in bond values during the bull market. Based on the Ibbotson Associates SBBI U.S. Intermediate-Term Government Bond Index, appreciation accounts for 40% of total traditional bond returns between October 1981 and December 2012—nearly twice as high as the historical average since 1926 of 15%.2

If the climate shifts to a bear market for bonds, bond prices will drop—and that could mean major losses in portfolio value for investors with existing bond holdings. The impact could certainly be enough to derail investors’ financial and retirement plans.

How we measured bond performance

Throughout this paper we rely primarily on two metrics for historical U.S. bond performance:

The10-yearU.S. Treasury note (referred to as “Treasurys”) is the benchmark we use when discussing relatively recent government bond performance (that is, over the past 20 or 25 years).

TheIbbotson Associates SBBI U.S. Intermediate-Term Government Bond Index, a broad-based index of 5-year U.S. bonds, provides a longer time series of bond returns. Thus, we used this measure when discussing longer-term historical trends.

We use the term “traditional bonds” to refer to U.S. government bonds, including Treasurys, that carry little or no risk of default, in contrast to higher-yielding corporate or municipal bonds.

Are you saying that the bull market for bonds is over?

I believe so, and I am by no means alone in that belief. Some analysts say we shifted to a bear market for bonds back in July 2012, when 10-year Treasury yields hit a long-term low of 1.4%. Whether you agree with that or not, it’s clear

that interest rates must eventually rise—they really have almost nowhere else to go.

Of course, no one can say what the Federal Reserve will do, or when. But if the economy improves and job creation picks up, I believe we’re likely to see somewhat higher rates of inflation, which could spur the Fed to begin raising interest rates sooner rather than later.

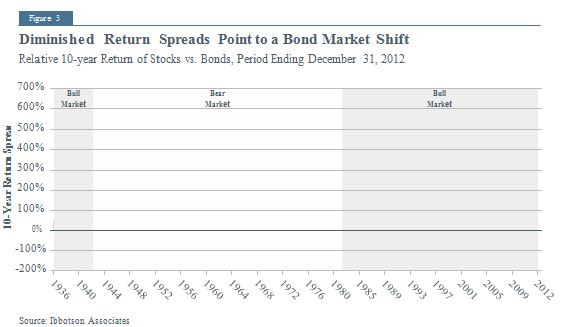

My view has also been influenced by the changing relationship between 10-year traditional bond index and stock market returns (Figure 3). The spread between the two has more or less disappeared in recent months. That is significant because under most conditions, stocks outperform bonds over a 10-year period—and when that’s not the case, the trend usually corrects itself fairly quickly, as we saw in the 1940s, ‘70s, and ‘80s. In fact, the current pattern is almost identical to the one we saw back at the start of the last bear bond market in 1941.

When you talk about risks, is it mainly those connected with rising interest rates?

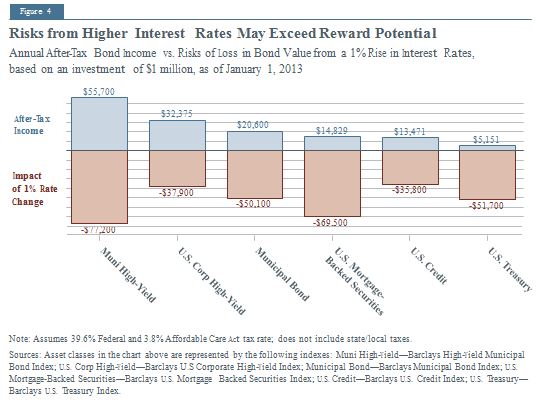

That is certainly the biggest and most immediate cause for concern. Our analysis shows that the risk of losses in bond value resulting from a rise in interest rates could potentially exceed the annual after-tax income from those investments (Figure 4). Think about what that means: if you bought a Treasury bond today and interest rates then rose just 10 basis points, the resulting loss of bond value would wipe out an entire year’s worth of returns.

But let’s not forget about inflation. That’s a more insidious risk, because rather than suddenly erasing a chunk of portfolio value, it chips away at it by degrees. Then, years down the road, you realize that you’ve lost a lot of the purchasing power you thought you had. This risk hasn’t been very prominent in investors’ minds because we’ve been in a low-inflation environment for the last

30 years. Since 1981, the Consumer Price Index has risen just about 3% a year, on average3— which is as you would expect in a bull bond market, since low yields and low inflation tend to go hand in hand.

The thing is, Treasury yields are already lagging inflation now. If consumer prices start ratcheting up, we could see an even greater negative real return on Treasurys.

When you boil it all down, what does the shifting bond market mean to investors? What is your overall message?

Whether you have existing bond holdings or are looking for new income streams, the same message applies: I believe investors need to broaden their search for income beyond traditional bonds. Those with existing bond portfolios also need to be aware of the risks associated with those holdings, and think about alternative income solutions that might help them make greater progress toward their financial goals. Today’s investors have access to a greater variety of income-generating alternatives than investors did 20 or 30 years ago.

Do you think most investors are fully aware of the bond market risks they are facing?

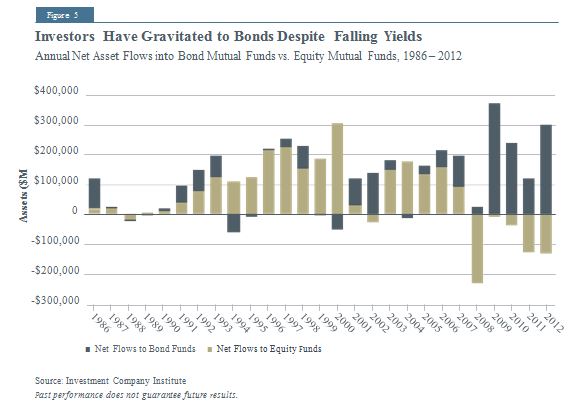

I suspect that many do not, based on the recent trends in asset flows. Since the financial crisis, investors have funneled billions into bonds, even as yields have continued to drop and risks have increased (Figure 5). In fact, the net flows into bond mutual funds from 2009 through 2012 added up to two-thirds of all net flows going back to 1926.4

Because equity funds saw a tide of outflows during this period, we can guess that the move into bonds was driven in part by investors’ fears of another stock market meltdown in this climate of economic and political uncertainty. If so, it’s

highly ironic—because in their flight to perceived safety, traditional bond investors have put themselves at high risk of investment losses. Those who fled the stock market also missed a strong market rally.

If you think about it, anyone who didn’t start investing before 1981 has had no experience other than rising bond prices and declining yields. So a whole generation of investors has had no personal exposure to a bearish bond climate and what it could do to portfolios.

Of course, it’s human nature to believe that “things are different this time.” But when you look at the historical patterns, it feels like maybe we’ve been here before. In terms of yields, inflation, and public debt levels, which historically have moved in a tight inverse correlation with yields, I believe the present climate bears some striking similarities to 1941, when we last shifted into a bear bond market.

Are you suggesting that it would be prudent for investors to move out of bonds altogether?

No, not at all. There are good reasons why an investor might want to have an allocation to Treasurys or some other relatively safe, short- term bonds in any market climate, especially if capital preservation and income stability are top priorities.

My point is that, in my opinion, investors would be wise to diversify a portfolio that’s heavy on traditional bond holdings. One way to do that is shift some assets from Treasurys to a flexible tactical bond strategy that invests across market sectors, such as tax-free municipal bonds, corporates, and high-yield bonds, and incorporates active risk management, including the ability to sell short. Those kinds of multi- sector strategies are designed to respond quickly to changing bond market conditions, including rising interest rates.

What are some of the other directions that income-focused investors might explore?

Dividend stocks, for one, which historically have been an important source of yield. Investors may not realize that stock dividends accounted for more than 40% of the S&P 500’s total return between 1926 and 2012. As of the end of 2012, the earnings yield of the S&P 500 was 5.3% higher than the 10-year Treasury yield, and 0.6% higher when adjusted for inflation.5

Investors might also want to look at more global investment options, including both dividend stocks and bonds. After all, the world’s fastest growing economies are now outside the U.S. Emerging markets have doubled their share of global Gross Domestic Product (GDP) in the last 20 years; they now account for about 38% of the world’s economy.6 If you want to diversify your income-generating investments, why not consider harnessing that kind of growth?

Real estate is another potential income source. Owning shares of Real Estate Investment Trusts (REITs) lets individuals invest in major commercial properties like high-rise office buildings. By law, REITs must distribute 90% of their operating income to investors each year if they want to avoid paying corporate income taxes, and over the past 30 years they have provided fairly stable yields averaging about 8% annually.7

When you talk about rotating into stocks, it raises some concerns. If investors were afraid of the stock market before, won’t they be even more so now that the market has had

an extended rally?

Investors are right to be cautious. History tells us that periods of strong stock market rallies are usually punctuated by market corrections or pullbacks, and over the long term, the market has had one down year out of every four years, on average. On the other hand, the stock market has outperformed bonds for several decades, albeit with greater volatility.8

Based on the economic data we’ve been seeing lately, I’m also of the opinion that economic growth may be picking up somewhat, both in the U.S.and abroad, which would bode well for stocks. For example, median home prices in the U.S. have been slowly rising over the past year or so, giving household balance sheets a boost.9 The employment picture appears to be improving, if slowly; as of the end of 2012, total unemployment claims are down by more than 50% from their June 2009 peak.10

As for corporate and individual debt, those levels have declined since they peaked around October of 2009.11 That is significant, since high debt levels across the board were one of the primary triggers of the 2008 financial crisis.

These factors won’t eliminate the risk of stock market downdrafts, but they do speak to the market’s balance of risk and reward over the longer term.

What about our stratospheric government debt levels? Isn’t that a cause for concern?

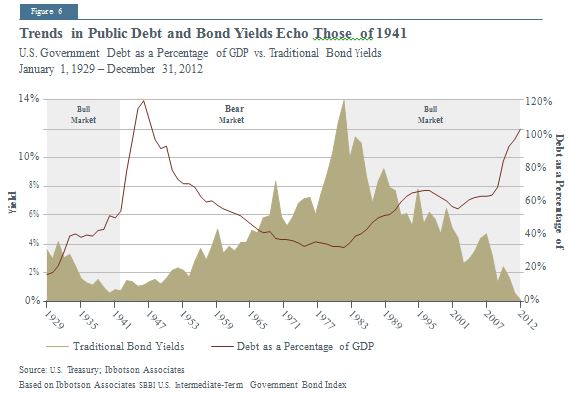

It’s true that U.S. debt levels are high, but they’ve been higher in the past. U.S. government debt is projected to rise to 108% of GDP by 2014; in 1944, the ratio was 120%.12 Remember that 1941 was the start of the bear market for bonds and rising relative values for stocks. Back in the early ‘40s, the relationships between traditional bond yields and public debt were very similar to those today (Figure 6).

This doesn’t guarantee that the same pattern will be repeated going forward, of course, but the historical view is consistent with the trends we’re seeing now. To my mind, that suggests that the economy should be able to continue growing despite our level of public debt. We’re also seeing moves to rein in government debt around the globe, and that is encouraging.

You’vemade a strong case that bond investors need to rethink their positioning. So what should income-focused investors think about doing now?

No one knows the future with certainty, but we can make an educated guess about what might happen by analyzing how a mix of income- generating investments would have performed during historical conditions resembling the ones we seem to be heading into now.

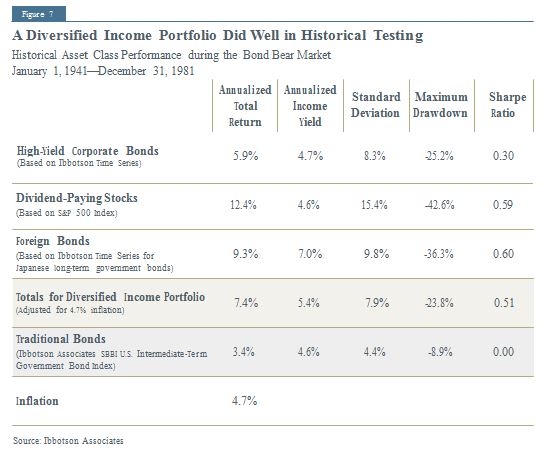

Based on my belief that we’re shifting into a bear market for bonds, our first analysis looked at how a diversified income portfolio would have performed during the 1941-81 bear market.

We found that over that period, a hypothetical equally weighted portfolio of high-yield bonds, dividend stocks, and foreign bonds would have delivered a total return 4% higher than traditional U.S. government bonds, including 0.8% more annualized income. Most important, the hypothetical diversified portfolio produced a positive return after adjusting for inflation, which the traditional bonds did not (Figure 7).

But don’t these alternative income sources have higher risks than Treasurys?

That’s absolutely true, and a very important point. The hypothetical diversified portfolio does display higher overall volatility than the traditional bonds, as reflected in its higher standard deviation measure. It also shows a higher maximum drawdown, meaning the largest single peak-to-valley drop in value during the period.

But investment professionals also look at an additional metric, namely, risk-adjusted return, which is usually measured by a portfolio’s Sharpe ratio. If you believe that investors should be compensated with higher returns for the risks they are assuming, the Sharpe ratio is worth considering. The higher the Sharpe ratio, the better the risk-adjusted return. On that basis, our analysis shows that the hypothetical portfolio would have delivered rewards more than commensurate with the risks.

Did you do any other portfolio testing? What can investors draw from your findings?

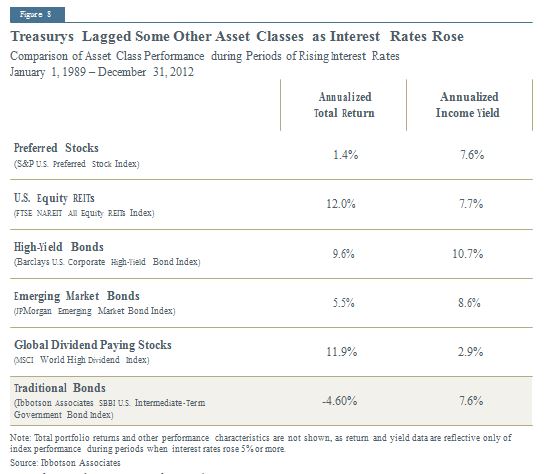

Yes, we did. Given the risks associated with potential interest rate hikes, I wanted to see how a diversified portfolio would have performed during the periods of rising interest rates starting in the late 1970s, by which time there was better asset class performance data.

Just to be clear, the time span covered by the exhibit included periods of declining interest rates and others in which rates were rising. The performance shown is only for those periods when interest rates were rising. You might notice that I tested somewhat different asset classes than I did in the 1941 to 1981 analysis. By the ‘70s, investors were able to take advantage of emerging asset classes that hadn’t existed before.

Once again, several income-producing asset classes matched or exceeded the yield from a broad-based index of U.S. bonds, and all the income alternatives generated higher total return (Figure 8). They also experienced higher volatility. But if interest rates rise, in all likelihood investors would be earning more yield to help offset that risk—though investors should always take to heart the disclaimer that past performance doesn’t guarantee future results.

Thiswhole discussion has put the notion of “safe and solid” bonds in a whole new light. What do you recommend that investors do now?

In my view, anyone who is concerned about the risks we’ve been discussing would be well advised to talk with his or her financial advisor. I’d want to know exactly how my portfolio is positioned from the standpoint of bond market risks and future income-generating potential. Then you’ve got a good basis for discussing whether you want to shift your portfolio allocations and what alternative income sources you might want to consider.

Any final thoughts?

Just another cautionary note—which is to say that only time will tell if the bull market in bonds is truly over. But to my mind, it’s precisely because the world is so unpredictable that a diversified approach to investment income makes sense in any market climate. I can’t think of any possible future market trend that should discourage investors from casting a wider net for investment income.

1. Ibbotson Associates, 12/31/12

2. Ibid.

3. Ibid.

4. Investment Company Institute, 12/31/12

5. Bloomberg, 12/31/12

6. IHS Global Insight, 12/31/12

7. Ibbotson Associates, 12/31/12

8. Ibid.

9. Bloomberg, 12/31/12

10. Bureau of Labor Statistics, 12/31/12

11. IHS Global Insight, 12/31/12

12. The White House Budget Update, 10/31/12

© 2013 Forward Management, LLC. All rights reserved.

All other registered trademarks or copyrights are the property of their respective organizations.

FWD004554

033114