As a graduate trainee in a London accepting house in the fall of 1981, I was given the tour and history of my new, 130 year old bank. It was one of the banks that set the daily gold price and had large bullion deposits somewhere under its location at 114 Old Broad Street. But the tour stopped at the vault door. No one went further (probably someone did but it was beyond my pay grade) and further discussion discouraged. Such was the mystery of gold.

Gold always struck us as a very weird investment. Sure it has this allure (it’s finite, durable, inflation hedge, the more ominous the world, the better for gold and so on) which can attract aficionados. Part of its reputation as a hard money tool is bunk. The Gold Standard that became the stuff of legend, from around 1870 to 1914, proved to be a very painful way to correct current account imbalances and led to several prolonged depressions and panics in any number of countries.

The recent obsession with gold had three phases: i) the 1970s rush when a production shortage (think Apartheid sanctions) led to a speculative bubble which took 20 years to clear and paved the way for ii) a Yale study in how, from 1959 to 2004, the risk premium for commodities was essentially the same as stocks but they were negatively correlated so you should jump in with new exciting vehicles in the form of iii) ETFs which quickly accumulated 84m oz of gold or about twice the entire circulation of Krugerrands. They also have a very weird third-hand claim on the gold if you care to read the prospectus. Short version: you don’t own gold when you own an ETF.

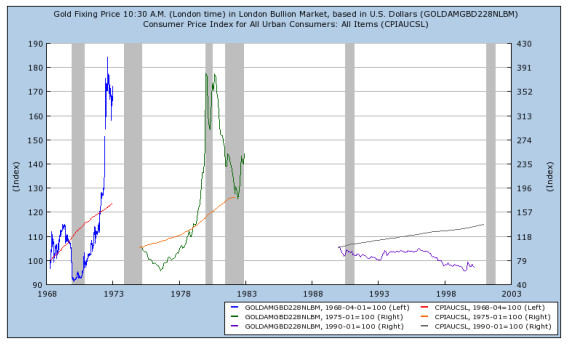

And that set the stage for a speculative blow out. Gold’s utility as an inflation hedge is useless. Here's one chart where the best you can say is that gold beats inflation sometimes but in a highly volatile way:

Source: Federal Reserve Bank of St. Louis, Economic Research

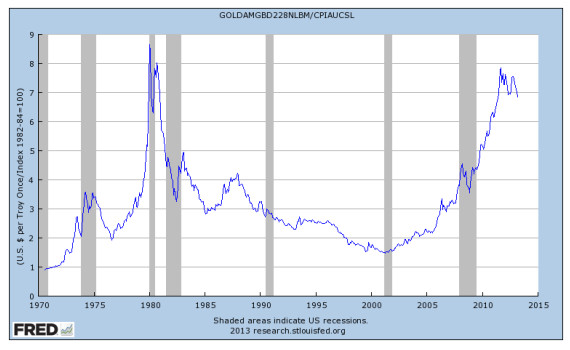

Or here where we divide gold by theCPIto get…well call it what you want but a hedge would be a straight line and this one ain’t. And it’s the same chart whether you price in Swiss francs, yen or pounds.

Source: Federal Reserve Bank of St. Louis, Economic Research

We think two things happened. One is that the low or negative correlation of commodities disappeared once the same buyers appeared. In other words, low correlations can happen if commodity buyers exhibit inherently differing behaviors to investors, (for example, they buy for industrial needs, inventory and fabrication) but these correlations narrow considerably once buyers are pursuing the same end. Put another way, correlations are as much buyer dependant as they are intrinsically dependant. With gold, the correlation with stocks used to be negative but for the last five years and one year have been 0.22 and 0.66. Two. Gold and its derivative markets have de minimis hedge loads, i.e. it no longer serves any utility as a hedge and so becomes just another financial asset. Risk on or risk off. Take your choice.

So what now? People will make money from gold but it will be increasingly speculators and timers. Not investors. We probably wouldn’t touch it.

BigHTto my colleague Jason Doiron on this…

1Yale? Yes, well look at the recent debate on the data veracity of the Reinhart-Rogoff study to see how easily beguiled investors can be by oh so serious papers.

Sources: Bloomberg; Capital Economics; Credit Suisse; “Facts and Fantasies about Commodity Futures,” Gary Gorton and K. Geert Rouwenhorst (National Bureau of Economic Research); Federal Reserve Bank of St. Louis; Sentinel Asset Management, Inc.

© Sentinel Investments

http://www.sentinelinvestments.com