F.I.R.S.T.: Bond Market Outlook

Bond Market Outlook

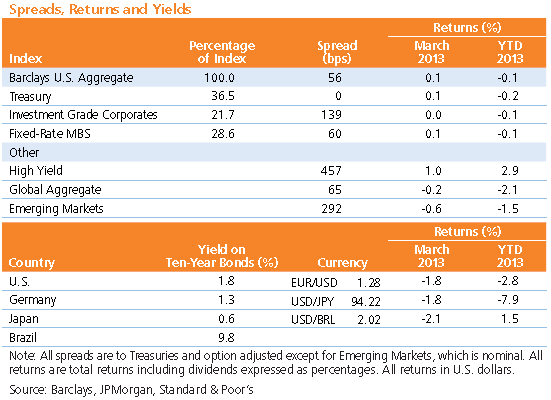

Global Interest Rates: Though yields appear rich, most central banks should remain accommodative through at least 2013.

Global Currencies: We are bullish on high-quality EMs like Mexico and Brazil but remain broadly bearish on developed currencies.

Corporates: As idiosyncratic risk increases, so too does the need for vigilance in security selection.

High Yield: Returns have been strong all year, and spreads still offer attractive compensation for longer-term default risk.

Mortgages: First quarter was challenging, but the recovering housing market and QE3 will be powerful catalysts.

Emerging Markets: We favor sovereigns over corporates, and continue to prefer high yield over investment grade credit and local over hard currency.

Macro Overview

- Amid heightened political uncertainty in Europe and subdued global growth expectations, global investors owe Hiroki Kuroda a big domo arigato for his pledge to inject about $1.4 trillion into the moribund Japanese economy by the end of 2014. The newly appointed BOJ governor’s unprecedented plan to buy Japanese government bonds, ETFs and other financial assets represents the boldest step yet in the central bank’s fight against the forces of deflation; as a percentage of GDP, the program makes even Ben Bernanke look like a tightwad. While Kuroda’s actions treat the traditional sound-money wisdom of his predecessors with the same respect that Godzilla treats downtown Tokyo, financial markets have thus far responded positively to the BOJ’s stimulus and to the resulting weaker yen.

- There tends to be a positive correlation between central bank balance sheet expansion and financial market performance, as the flood of liquidity incites investors to search for more attractive currency-hedged yields. The impact of the BOJ’s announcement was no different from that of the liquidity jolts previously provided by the Fed and ECB, spurring the outperformance of longer-duration U.S. Treasuries, U.S. agency mortgage-backed securities, higher-yielding emerging market currencies (like the Brazilian real) and sovereign debt for certain European countries (such as France).

- The Bank of England, meanwhile, likely is on the verge of another QE announcement, and the ECB has felt increasing pressure to provide further accommodation thanks to big trouble in little Cyprus and the lack of a functioning government in Italy. Recent Fed rhetoric suggests QE in the U.S. will continue at least through year end in the absence of a large upside surprise from labor markets, which disappointed profoundly in their latest release.

- Thankfully, there are also signs of organic life out there. Robust private-sector demand and improvements in the U.S. housing and manufacturing sectors continue to be supportive, and emerging market fundamentals remain attractive. We are constructive on global credit risk and higher-yielding EM currencies that can withstand a stronger U.S. dollar. While global interest rates will likely move higher as investors pursue higher-yielding alternatives, rates will stay relatively contained thanks to monetary stimulus here and abroad.

Sector Overviews

Global Interest Rates

- Japan’s quantitative easing program is the big story in global rates. The U.S. yield curve flattened in response, and the effects have spread into other yield curves globally. Markets will be tracking the movements of Japanese investors as the BOJ squeezes local investors out of the domestic space.

- Global growth appears stable despite fiscal and political headwinds. Yields appear rich to fair value; given heavy quantitative easing and near-zero inflationary pressure, however, we expect most central banks will keep monetary policy easy through 2013 and in some cases into 2014. We are bullish on most higher-yielding emerging markets while remaining neutral to bearish on most developed nations.

Global Currencies

- In global currencies, we continue to be biased toward those emerging markets in which fundamentals and foreign exchange yields look attractive relative to their developed counterparts —particularly in Latin America and certain parts of Asia ex-Japan, such as the Chilean and Colombian pesos and the Malaysian ringgit.

- We do not believe the U.S. dollar strength in early 2013 is sustainable until the Fed begins to taper its purchase programs, which is unlikely this year. Nonetheless, we are bullish on high-quality emerging markets that will benefit from a stronger U.S. dollar and U.S growth, like Mexico and Brazil, but we remain broadly bearish on developed market currencies like the euro, pound sterling and Japanese yen. We are also bearish on currencies likely to trade in sympathy with a weakening yen, like the Aussie dollar and Korean won.

Investment Grade

- We remain negative on credit fundamentals. We still expect year-over-year sales and earnings growth rates to decelerate before stabilizing and potentially inflecting later this year. But as top-line weakness and the upward drift in leverage continues, we maintain our negative fundamental view.

- Technicals continue to be supportive; inflows have been relatively stable, and spreads have been remarkably firm despite the turmoil in Cyprus. We expect demand to stay healthy even as new-issue supply exceeds expectations. Idiosyncratic risk — in the form of shareholder-friendly activities and instances of voluntary leveraging — has increased, highlighting the need for vigilance in security selection. The financial and utility sectors continue to offer investors a relative safe-haven versus industrials.

High Yield

- The high yield market has largely ignored the latest headlines out of Europe. As has been the case in recent months, lower-quality credits outperformed higher-quality credits, as high dollar prices have left little room for appreciation. However, high yield returns have been strong all year, and spreads still offer attractive compensation for default risk in the longer term.

- While U.S. flows have been mixed, flows to non-U.S. funds remain strong and most of this money finds its way into the U.S. market, helping to absorb a heavy new-issue calendar. An escalation of the European crisis could lead to outflows of non-U.S. funds, which could indirectly pressure U.S. prices.

Mortgages

- Agency MBS performance will continue to be dictated by interest rate volatility. The FOMC’s focus on job growth and economic momentum may be a silver lining, as QE3 ($40 billion agency/GNMA purchases per month) is a powerful driver for MBS performance. Non-agency RMBS has remained well-bid throughout the quarter, supported by strong momentum in the U.S. housing market. Supply, both secondary and primary, has remained manageable and well-supported by banks, insurers and money managers seeking yield.

- With almost $20 billion in new-issue supply year to date, CMBS spreads came under pressure in February; though spreads firmed with lighter new issuance in March, we expect elevated supply in April. Fundamentals have remained supportive in the U.S. commercial real estate market, as delinquencies have continued their steady decline and transaction velocity remains elevated.

Emerging Markets

- Emerging markets were negatively impacted by the March spike in European sovereign risk, though the magnitude was limited by stronger U.S. growth and the Fed’s commitment to monetary accommodation. Flows continue to favor local-currency over hard-currency sovereigns. Overall, we are constructive on emerging sovereigns and expect some spread compression in coming months, though local markets should outperform for the year.

- While all segments of the emerging corporate market widened in March, high yield names have continued to outperform and technicals have improved with some slowing in new issuance. Corporate leverage has moved higher and valuations have grown challenging. However, the outlook for EM corporates continues to be cautiously optimistic, as the search for yield is expected to drive interest in the asset class.

ING U.S. Investment Management’s fixed income strategies cover a broad range of maturities, sectors and instruments, giving investors wide latitude to create a new portfolio structure or complement an existing one. We offer investment strategies across the yield curve and credit spectrum, as well as in specialized disciplines that focus on individual market sectors. We build portfolios one bond at a time, with a critical review of each security by experienced fixed income managers. As of December 31, 2012, ING U.S. Investment Management managed $127 billion in fixed income strategies in the United States.

This commentary has been prepared by ING U.S. Investment Management for informational purposes. Nothing contained herein should be construed as (i) an offer to sell or solicitation of an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. Any opinions expressed herein reflect our judgment and are subject to change. Certain of the statements contained herein are statements of future expectations and other forward-looking statements that are based on management’s current views and assumptions and involve known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed or implied in such statements. Actual results, performance or events may differ materially from those in such statements due to, without limitation, (1) general economic conditions, (2) performance of financial markets, (3) interest rate levels, (4) increasing levels of loan defaults, (5) changes in laws and regulations and (6) changes in the policies of governments and/or regulatory authorities.

Past performance is no guarantee of future results.

© 2013 ING Investments Distributor, LLC • 230 Park Avenue, New York, NY 10169

CID 6219